The AI PC story is picking up speed, with global semiconductor revenue expected to top $1 trillion for the first time in 2026. This jump is driven mostly by strong AI demand, with the Computing & Data Storage segment alone forecast to grow 41.4% year-over-year (YOY) and pass $500 billion. On top of that, Gartner expects worldwide AI spending to hit $2.59 trillion in 2026, a 47% increase from the prior year.

Intel (INTC) does not want to be left behind in that kind of market. It is pushing major PC makers in the U.S., China, and Taiwan to move to its most advanced 18A-process chips, including the Panther Lake and Wildcat Lake platforms, as demand for top-tier processors starts to run ahead of supply on the best manufacturing nodes.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Wedbush Securities sees this as a smart way for Intel to protect its margins by guiding customers toward higher-value, premium-priced chips.

Will this proactive push into next-generation chips finally deliver the sustainable margin expansion and revenue growth investors are craving, or is it merely a tactical defense in a hyper-competitive market?

Intel’s Messy Earnings Picture

Intel is based in Santa Clara, California, and designs, manufactures, and sells microprocessors, chipsets, and related computing platforms for PCs, data centers, and newer AI-focused devices around the world.

INTC has a year-to-date (YTD) gain of 220.26% and a 52-week return of 471.17%.

www.barchart.com

www.barchart.com The company now has an equity value of $598 billion, and its trailing price-to-earnings multiple of 1,846.67 times and trailing price-to-cash-flow multiple of 59.91 times are far above sector medians of 25.06x and 18.35x.

Their latest quarterly report, for the period ended March 26, showed revenue of $13.58 billion versus analyst estimates of $12.39 billion, which worked out to 7.2% YOY growth and a 9.6% beat. It also delivered adjusted earnings per share of $0.17 compared with an estimate of -$0.10, producing a +270.00% surprise.

INTC posted adjusted operating income of $1.67 billion, versus a $397.4 million analyst estimate, and Intel turned that into a 12.3% adjusted operating margin, suggesting the higher-end product mix is already helping.

It is also clear that the underlying numbers are still messy. The operating margin was -23.1% in March 2026, compared with -2.4% in the same quarter last year. The company reported net income of -$3.728 billion, with net income growth at -530.80%.

Intel generated $1.096 billion in operating cash flow, although that was down 88.70%, and its net cash flow came in at $2.983 billion, down 53.85%. This is why Intel’s push to steer PC makers toward its latest chips matters so much, because a better mix and pricing are some of the few levers it can pull quickly to support those stretched financials.

Intel Leans on New Partnerships and Chips

Intel’s push to get PC makers onto its latest chips builds on the recent launch of its Core Series 3 processors, which are meant to bring AI‑ready performance to small businesses, schools, and budget-conscious users. These chips are designed to power AI‑capable PCs with better everyday performance and efficiency, support up to 40 platform TOPS, and deliver clear gains over older machines, gently steering customers toward newer, higher‑value systems.

That same strategy shows up in its long-term work with Alphabet's (GOOGL) on infrastructure. Under a multi‑year deal, Google continues to use Intel’s Xeon processors while the two companies co‑develop custom infrastructure processing units that fine‑tune networking, storage, and AI workloads at massive scale.

Additionally, Intel has gone from being viewed as a “market reject” to landing a key AI role with Elon Musk’s ventures. Its involvement in Musk’s Terafab project, a huge AI and semiconductor campus meant to support Tesla (TSLA), SpaceX, and xAI with advanced 14A process manufacturing, has helped reposition Intel’s foundry arm as a more credible AI supply‑chain partner.

The brand is getting more visibility in high‑performance settings, too. Intel was recently named the official compute partner of McLaren Racing across Formula 1, IndyCar, and sim racing. Its Xeon and Core Ultra processors will power everything from aerodynamics simulations to race‑day strategy analytics.

These moves all feed into the same story Intel is telling PC manufacturers that the future is on its newest platforms, and that is where the performance, partnerships, and pricing power now live.

Analysts Weigh Intel’s Margin Story

Intel’s next big checkpoint is set for July 23, when it is scheduled to release earnings for the June 2026 quarter. In the upcoming report, the Street is looking for average earnings of $0.10 per share, compared with -$0.26 a year earlier. That works out to an estimated YOY growth rate of 138.46%.

Those higher expectations line up with rising interest from big-money investors. During Q1 2026, Chase Coleman’s Tiger Global Management, one of the most closely watched hedge funds on Wall Street, quietly built a fresh position in Intel. The fund bought 1,638,700 shares, a stake worth roughly $180 million based on its most recent 13F filing.

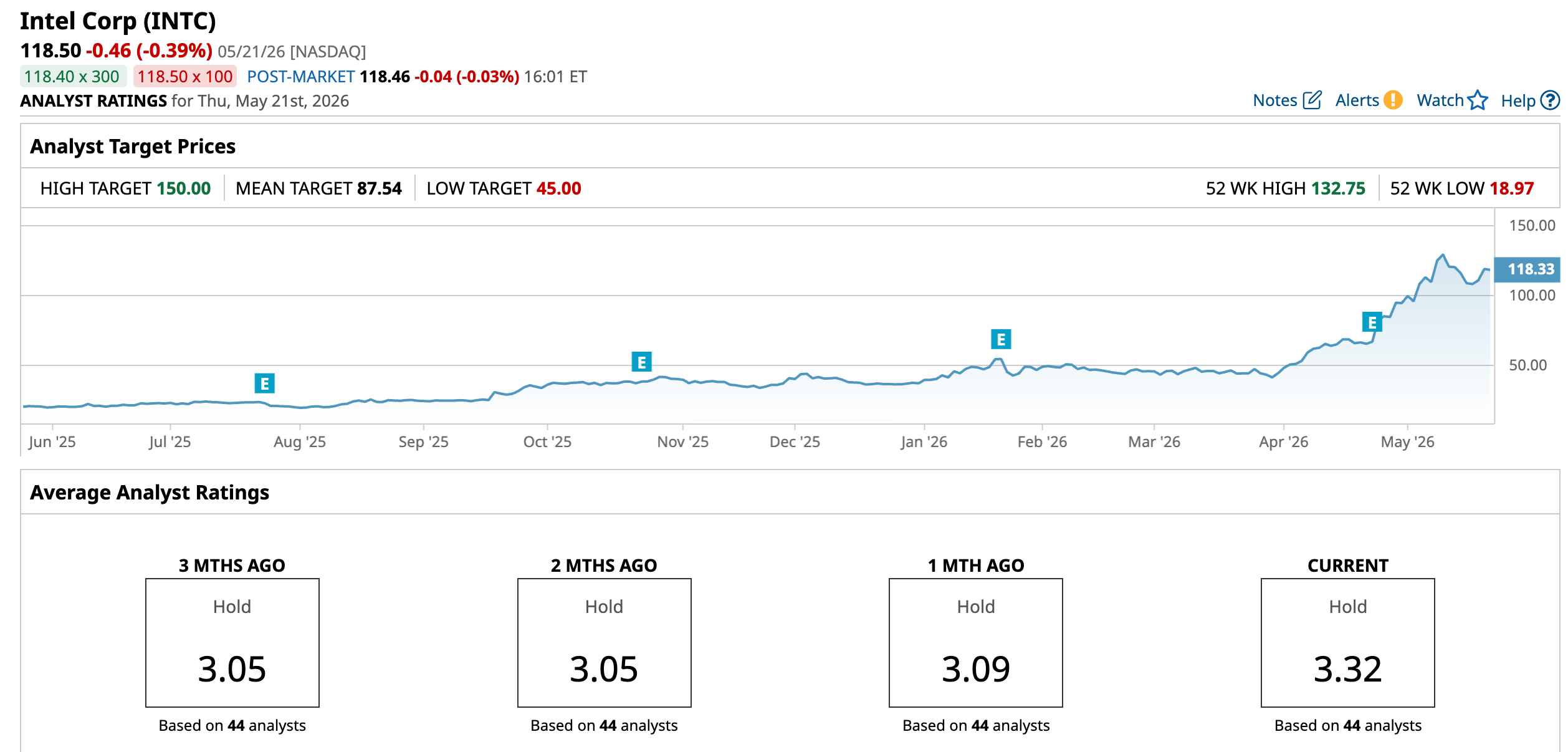

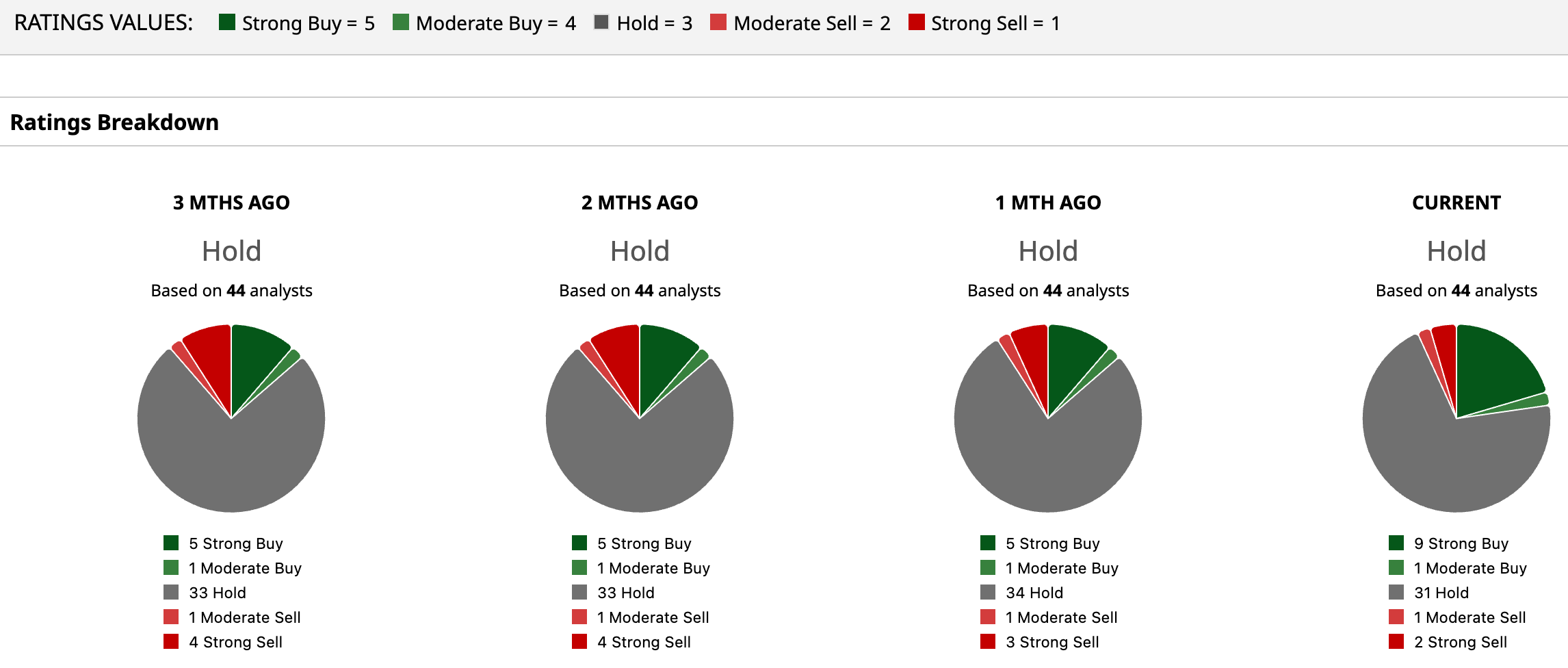

Even with that kind of backing, the broader analyst crowd is still careful. The stock has a consensus “Hold” rating from 44 analysts, which shows the Street is not ready to call Intel’s margin comeback complete. The average price target is $87.54, well below the current share price and implying roughly 26% downside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Intel’s push to get PC makers onto its newest chips looks like a real, if imperfect, way to support margins rather than just a flashy headline move. The fundamentals still need work, but a better product mix, tighter supply, and more AI-related deals all point to earnings and cash flow slowly improving from here. In that kind of setup, the stock seems more likely to cool off or move sideways than crash, with the next few quarters key to proving the margin story in the actual numbers.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Intel Urges PC Makers to Switch to Its Latest Chips Amid AI Demand. This Could Be the Margin Boost INTC Stock Needs. Why Billionaire George Soros Is Betting Big on Talkspace Stock When Growth Stocks Finally Collapse, You’ll Want This 1 Anti-Beta ETF in Your Portfolio Micron Stock is Up over 133% From Its Lows - But Is MU Still Undervalued?