The market capitalization of Broadcom Inc. (AVGO) is rapidly approaching the $2 trillion mark. This fact alone places the company in the club of the largest technological giants of the planet. But in my view, the current market valuation appears overheated, and investors, pricing in perpetual growth while assuming margins remain intact, are making a mistake.

The current optimism is understandable. Broadcom positions itself in the market as the main beneficiary and leader in the segment of custom AI-chips (ASIC), forming long-term alliances with key consumers of computing capacities — Alphabet (GOOG) (GOOGL), Meta (META), and recently OpenAI and Anthropic. However, behind beautiful headlines about multi-billion contracts lies a deep contradiction between the expectations of Wall Street and the real business model by which this sector functions.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Economic Essence of Custom Silicon: Engineering vs. Product Model

The main delusion of Broadcom bulls likely lies in a linear comparison of Broadcom with Nvidia (NVDA). But these are principally different economic structures. Nvidia creates a general-purpose commercial product (GPU), fully takes on itself the risks of development and due to its technological moat dictates to the market a high markup, holding the gross margin in data centers on a level higher than 70%.

The model of Broadcom in the segment of custom accelerators (ASIC) is structured differently. Such technological giants, as Google (for its TPU) or Meta, opt to develop custom chips with a main goal — to minimize their infrastructural costs and to walk away from super high markups of third-party suppliers. In this setup, Broadcom acts as a co-developer, architect, and logistician of the supply chain.

The rights to the final chip belong to the customer. Simply put, Google hires Broadcom for the optimization of its spendings. And therefore in my view, a hard margin ceiling is laid into this business-model. A custom chip is created for the sake of the savings of the client, and means, the client never will allow Broadcom to lay into the contract a net margin of "Nvidia" level. There, where a pure-play vendor pockets $10 of profit, a contract architect will receive obviously less. It will earn primarily on the licensing of ready blocks of intellectual property (IP) and possibly a fixed markup for the organization of production on the factories of TSMC.

Financial Indicators and Real Structure of Margin

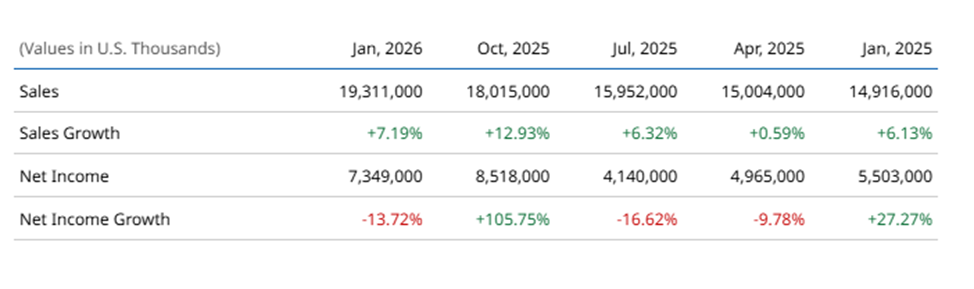

Let us look at the dynamic of revenue and net profit of Broadcom based on Barchart data.

Undoubtedly, the company shows a systematic growth of sales. In the last reporting quarter, the revenue reached $19.3 billion. However, taking a sober look at these numbers, it becomes obvious that on their own, they hardly justify a capitalization in almost $2 trillion. Even at a rough extrapolation, we receive a business with an annual revenue less than $80 billion. Yes, on the given moment the company demonstrates impressive overall margins, but the whole problem lies in its source.

The fact is that the current impressive gross profitability (around 75.6%) — this is the merit of the mature software business (the integration of infrastructural software VMware and other products) and leadership positions in traditional network switches. The flaw in market models is that they extrapolate this historical margin onto future periods. That very “explosive growth,” for the sake of which they value the company so highly, is expected exactly in the segment of custom chips. As the share of this segment grows in the general structure of revenue, the general profitability will inevitably begin to dilute, since the profit margin there is a priori lower. To expect the preservation of the current margin at such a change of the business means to contradict basic logic and the laws of economics.

Multiples, Disconnected from Reality

If we annualize the current quarterly net profit ($7.35 billion), we will receive around $29.4 billion of net income. At a $1.98 trillion market cap this translates to a real P/E multiple on the level of 67x–70x. Even factoring in analysts' forward expectations (forward P/E in the region of 36.7x), the market demands from Broadcom a practically ideal, uninterrupted doubling of profit over the next 24 months.

Conclusions

In conclusion, Broadcom remains a fundamentally strong business under the management of one of the most effective managers of the industry — Hock Tan. However the current price of shares on the level of $400+ fully ignores the structural risks of the lowering of margin. Custom silicon is an instrument of cost optimization for the largest IT corporations of the world, and not a source of super margin for Broadcom. In my view, the current capitalization of the company looks overheated, and in a medium-term perspective investors can expect a painful reality check from actual margin figures.

Disclaimer: The present article reflects exclusively the personal analytical opinion of the author, founded on public financial reports of the company, and does not constitute individual investment advice.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Intel Just Launched Its SuperClaw AI Tool. INTC Stock Is Finally Back from the Dead. GDP, Earnings and Other Key Things to Watch this Week Bloom Energy Stock Could Continue Rising. Here’s Why. The Broadcom Stock Paradox: Why a $2 Trillion Valuation Ignores the Base Economics of Custom Chips