Amid all the distrust between China and the United States concerning artificial intelligence, an endorsement from a Chinese brokerage for an American neocloud company is certainly noteworthy. That is exactly what happened with CoreWeave (CRWV), when Chinese brokerage firm GF Securities initiated coverage on the former's stock with a “Buy.”

Citing long-term demand, close relationships with major hyperscalers, and eventual profitability by 2028, the firm said this in a note to clients: “Backed by first-mover GPU deployment, exclusive AI-only focus, best-in-class efficiency, and LTAs with major AI hyperscalers, CoreWeave is positioned as a long-term winner in the AI infra boom. We are positive on 1) accelerating demand for AI buildouts; 2) RPO that largely underpin our 2026–2027 revenue forecasts; 3) declining debt financing costs; 4) profitability to inflect sharply as large contracts mature; 5) new LTAs benefiting from higher GPU rental pricing.”

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

GF's optimism is certainly not misplaced, as CRWV stock is up 47.8% YTD.

www.barchart.com

www.barchart.com Enviable Customer Base

What started as a cryptocurrency mining company has now become one of the world's largest neocloud players. The story is akin to one of its closest partners and investors, Nvidia (NVDA), which pivoted from a company focused on graphics for gaming to becoming what it is today — the linchpin of the AI industry.

However, while I have recently discussed what makes CoreWeave unique, the company is also converting this uniqueness into customers. And not just any customers, CoreWeave is the neocloud of choice for many of the largest hyperscalers in the world.

Notably, while the company's Nvidia connection is not there to hide from anyone, it is actually another tech titan that first onboarded CoreWeave. It is Microsoft (MSFT).

Before other big tech players began aggressively courting specialized cloud providers, Microsoft recognized the potential in CoreWeave infrastructure to support its massive demand for AI reasoning and model training. By 2024, this relationship had matured significantly, with Microsoft accounting for approximately 62% of the annual revenue of CoreWeave, providing the financial stability and credibility necessary for the firm to scale its data center footprint and procure high-end hardware from partners like Nvidia.

And if there is Microsoft and we are talking about AI, can OpenAI be left far behind? In March 2025, OpenAI signed a five-year agreement with CoreWeave valued at $11.9 billion. This contract was later expanded twice, bringing the total commitment from OpenAI to about $22.4 billion.

Beyond the massive commitment from OpenAI, the partnership with Meta has been equally transformative for the long-term outlook of CoreWeave. In a deal that underscores the race for resilient data center capacity, Meta (META) solidified its existing relationship with an expanded agreement that runs through December 2032. This deal, valued at roughly $21 billion, focuses on scaling infrastructure to support the complex AI operations of Meta. When aggregated with earlier commitments, the total value of the agreements with Meta reaches roughly $35.2 billion. This multi-year visibility is critical for a company like CoreWeave because it allows for disciplined capacity planning and provides a strong foundation for ongoing investment in next-generation architectures such as the Nvidia Vera Rubin platform.

Finally, it's not just hyperscalers; financial institutions are also opting for CoreWeave for their AI workloads. For instance, in April 2026, Jane Street entered into a $6 billion AI cloud agreement, signaling that the demand for this specialized infrastructure extends well beyond traditional consumer tech giants and into the realm of quantitative finance. Overall, the company's financial services backlog stands at $10 billion.

Furthermore, the company has begun integrating its services more deeply with Google Cloud through new interconnect and orchestration services announced in April 2026.

These developments suggest that while the initial hyperscaler deals provided the necessary capital for takeoff, CoreWeave is now shifting toward a more diversified model that integrates its specialized GPU clusters into a broader multi-cloud ecosystem.

CoreWeave Getting Closer to Profits, Yet Still Not There

CoreWeave's financials are a mixed bag, marked by unprofitability but strong growth.

The first quarter of 2026 presented a complex picture for the company, characterized by revenue growth that outpaced expectations even as bottom-line results failed to meet analyst targets. Specifically, the firm generated $2.08 billion in revenue for the quarter, representing an impressive 111.6% increase over the previous year. Despite this top-line success, the company reported a loss of $1.40 per share, which was worse than the projected loss of $1.20 per share. Although this loss was slightly narrower than the $1.49 per share recorded in the same period last year, operating loss margins widened to 7% from 3%, suggesting that the cost of scaling operations is currently rising faster than revenue gains.

However, a distinct positive in the recent financial update is the massive improvement in liquidity.

Net cash from operating activities soared to about $3 billion, compared to just $61 million in the prior year. This jump was bolstered by a significant reduction in accounts receivable of about $1 billion, which reflects a more effective collection of payments from its client base compared to the previous year. Nevertheless, the balance sheet remains a point of scrutiny for some.

The company finished the quarter with a cash position of $2.2 billion, a total that appears constrained when weighed against short-term debt obligations reaching $8.1 billion. Investors will likely be watching closely to see if the company can maintain its rapid revenue trajectory and convert those gains into a more stable financial position while managing its substantial debt load.

Valuation metrics for the stock present a divided outlook for potential investors. On one hand, the forward P/S ratio of 4.36x sits slightly above the sector median of 3.30x, indicating a premium pricing relative to its peers. On the other hand, the forward P/CF ratio of 6.15x is distinctly lower than the sector median of 18.98x, suggesting that the company is more efficient at generating cash flow than its current market valuation might imply. This contrast highlights the ongoing debate surrounding the firm as it attempts to balance aggressive infrastructure spending with the need to demonstrate long-term financial viability in a competitive cloud computing environment.

Analysts' Opinions

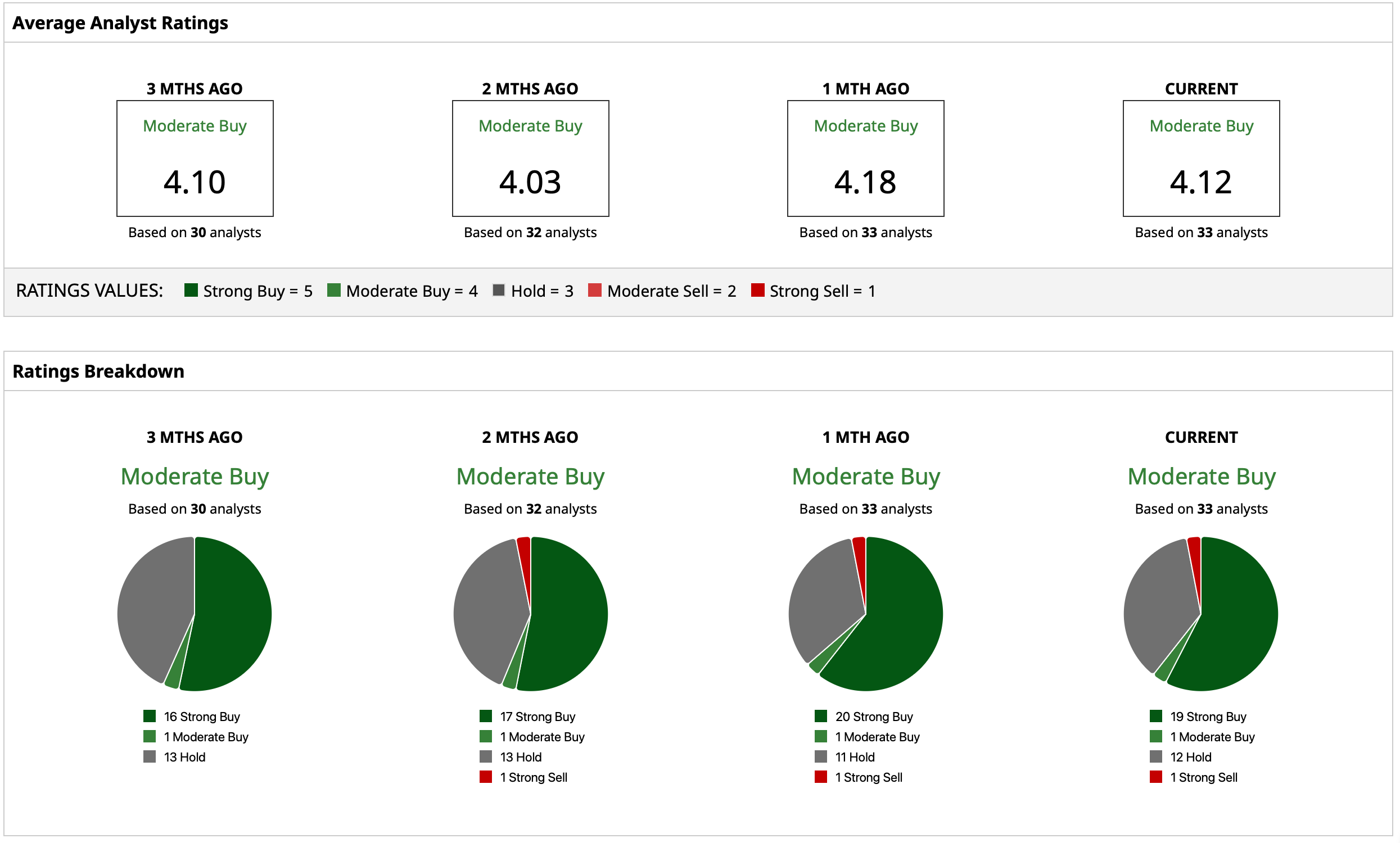

Taking all this into account, analysts have attributed an overall rating of “Moderate Buy” for CRWV stock. The mean target price of $133.26 denotes an upside potential of 23.9% from current levels. Out of 33 analysts covering the stock, 19 have a “Strong Buy” rating, one has a “Moderate Buy," 12 have a “Hold," and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Is Warming Back Up to CoreWeave Stock. Long-Term Demand Is Helping. Palantir’s AI Surge Meets Market Correction. Buy the PLTR Stock Dip Now. 1 Outstanding AI Stock You’ll Regret Ignoring 10 Years From Now A $2.6 Billion Reason to Buy Bloom Energy Stock Now