As I’ve noted here recently, this stock market is in desperate need of some heroes. I do not think the AI trade can carry things much longer.

So instead of looking in the usual places, I am starting to look for turnaround situations. And that leads me to the iShares U.S. Medical Devices ETF (IHI). This is the type of ETF that makes me glad there are ETFs. Because I do not always want to pursue growth with single-stock risk.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

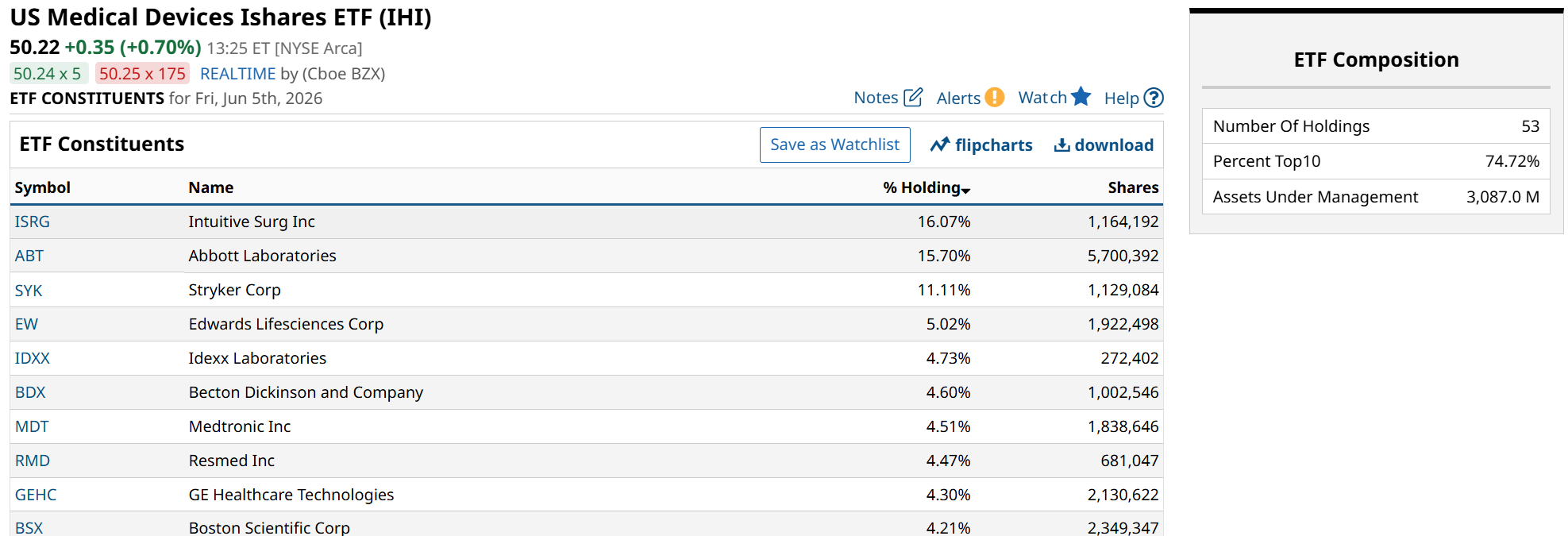

As we see here, IHI is 75% allocated to its 10 largest names out of about 50 stocks in total. Plus, 43% of the entire ETF is invested in only three stocks, as shown here.

www.barchart.com

www.barchart.com For many investors, especially newer ones, they see this as “too concentrated, too risky.” And I say that if you own IHI, it is likely a small enough part of your portfolio that it is best to view it as a way to access one or two handfuls of stocks you want. Or one favorite, with some cushion around it. In this case, Intuitive Surgical (ISRG), Abbott Laboratories (ABT), and Stryker (SYK) would be the prime targets. But if one of them falters, as they often do, the rest can potentially pick up the slack.

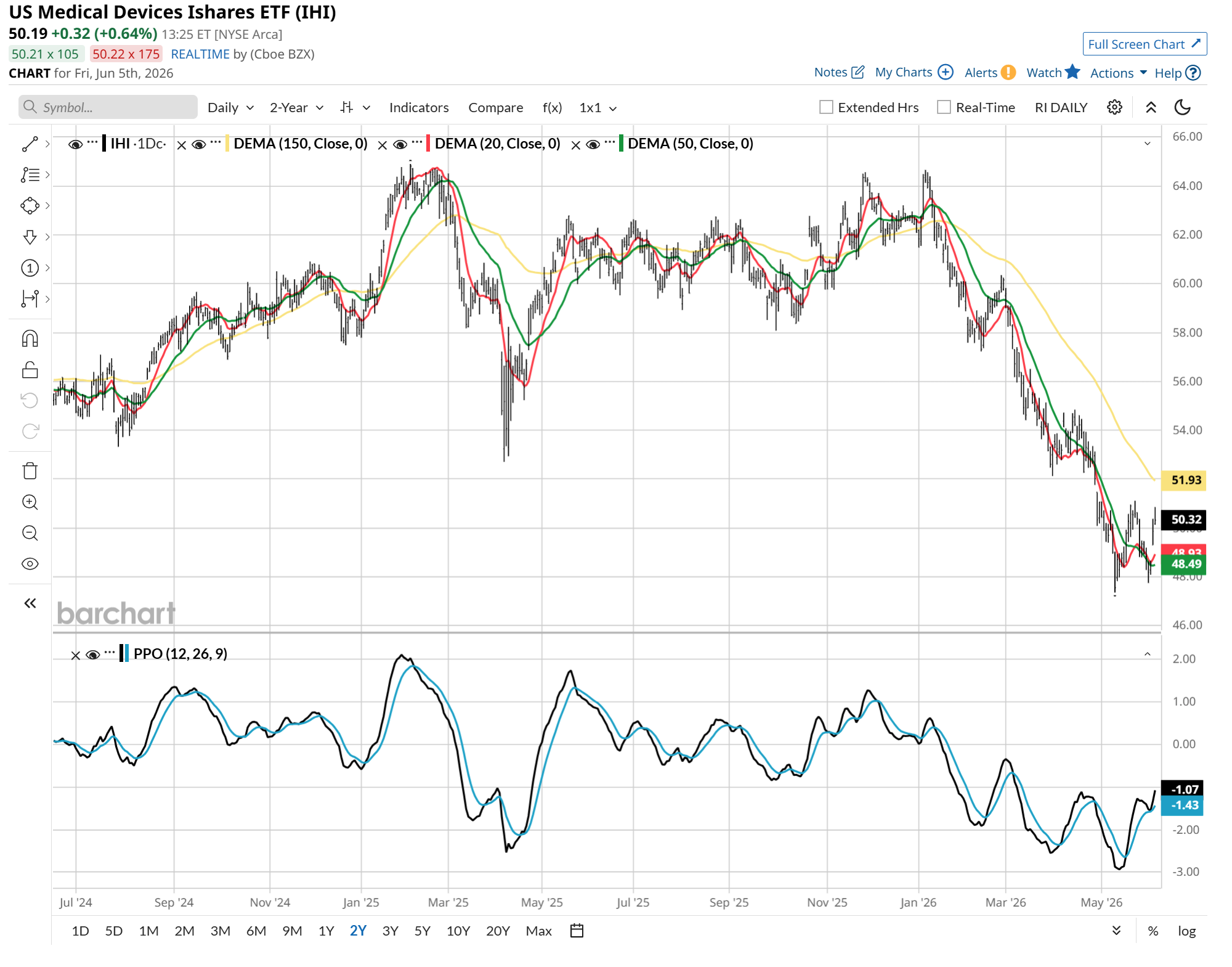

After spending the last few years trapped in a grueling, relative-performance purgatory while the market chased AI chips, medical device stocks are quietly trying to establish a bottom.

www.barchart.com

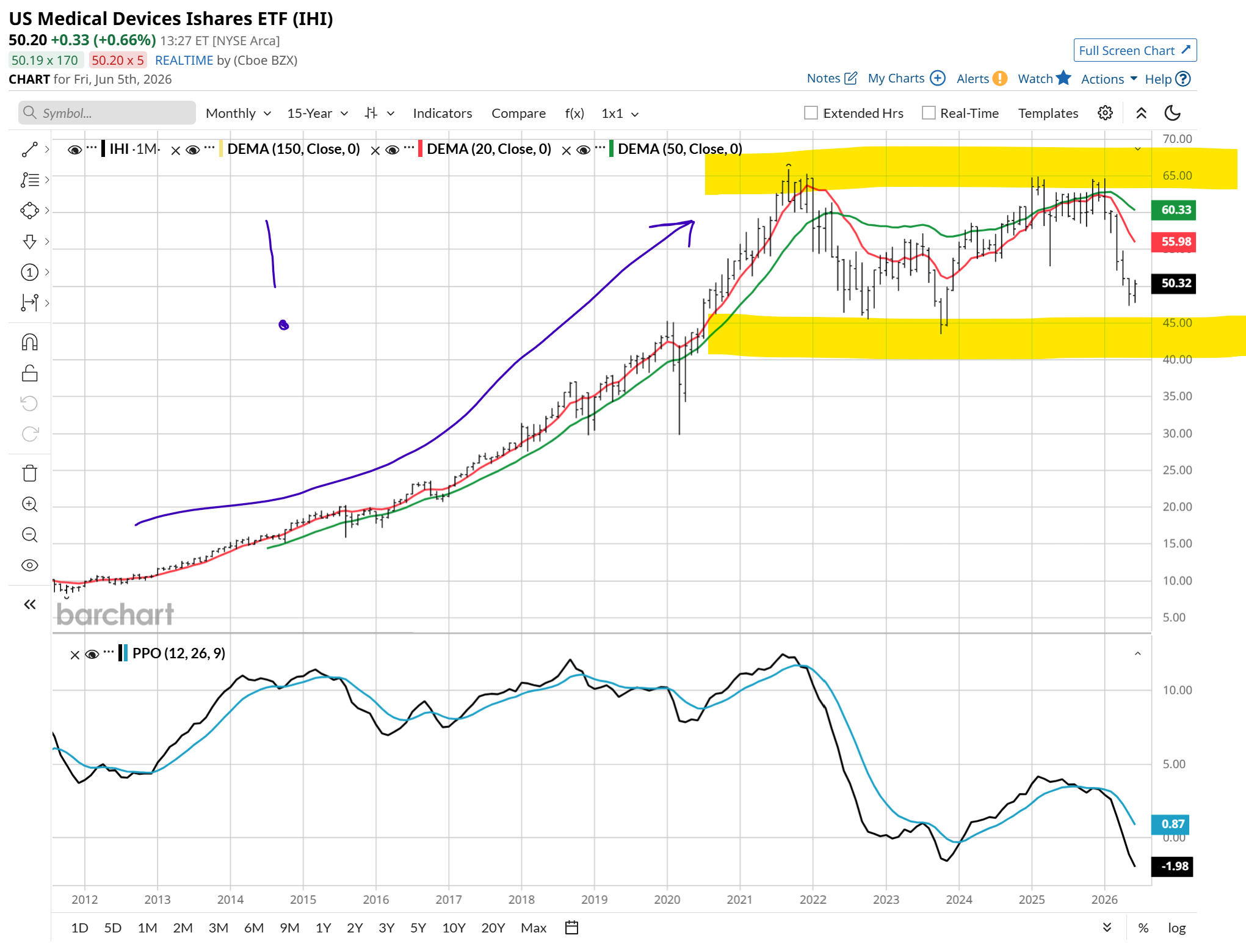

www.barchart.com Let’s add some perspective here. This is a longer view (below), showing the past 15 years for IHI. These stocks were essentially their own med tech revolution for many years, and IHI was the place to be. Up about 550% in a decade through late 2021. See how market segments and themes can rise and fall?

I’ve marked that fantastic run with a single “!” in this chart. Then I drew in the wide trading range that has existed for about five years now. IHI is toward the bottom of that range. So is the percentage price oscillator (PPO) on this monthly chart. So this long-term contrarian view is coming into shape for me.

www.barchart.com

www.barchart.com The question to ask right now is simple: Did the medical device sector just signal a major, multi-year structural bottom?

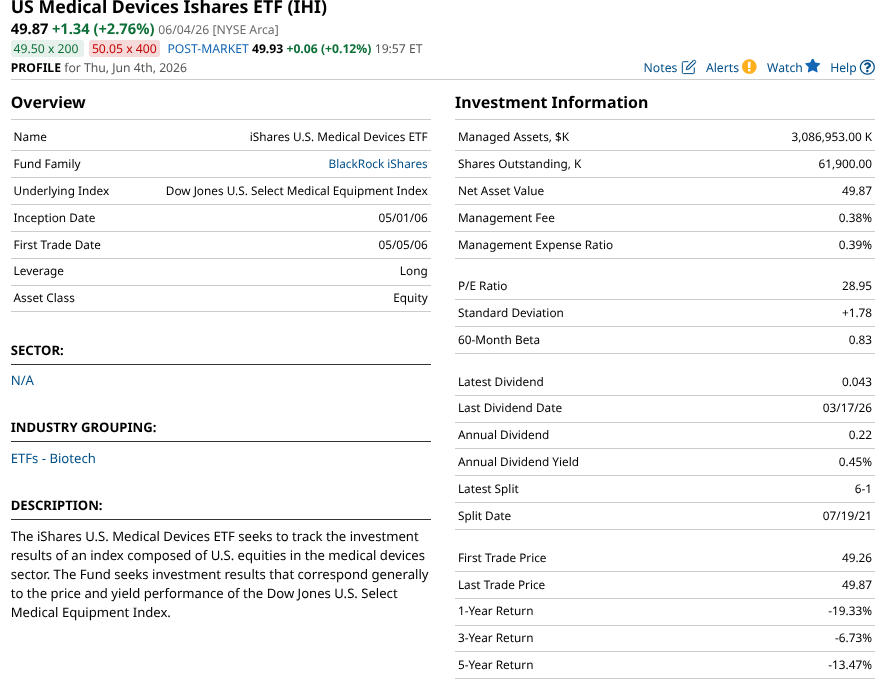

Let’s break down the bull and bear fundamental case for what is really happening inside IHI, now a $3 billion ETF, one which just celebrated its 20th birthday.

www.barchart.com

www.barchart.com The Bull Case: The Post-GLP-1 Capitulation and Demographics

The fundamental bull case for IHI is a classic story of an overextended narrative finally hitting a wall of reality. A couple of years ago, the rise of weight-loss drugs (GLP-1s) triggered a massive panic selloff in medical device stocks. The thesis was that thanks to GLP-1s, no one would ever need bariatric surgery, cardiovascular stents, or orthopedic knee replacements again.

The market is finally realizing that GLP-1s do not magically cure aging joints or erase structural defects. The demand for physical medical devices is roaring back.

The underlying engine for medical devices is completely decoupled from the tech cycle. The massive Baby Boomer generation (which I am part of) is moving deeper into their prime surgical and medical intervention years (tell me about it!).

The structural, baseline demand for pacemakers, artificial hips, and glucose monitors is locked into an upward trajectory for the next decade. Hospitals have finally resolved their post-pandemic staffing shortages and supply chain constraints.

And, high-margin elective surgeries are being booked at record paces, flowing straight through to the top and bottom lines of major device manufacturers. Or to put it another way:

Q: “Hey boomer, what are you going to spend your money on after all those cruise vacations?”

A: “Medical procedures from everything that happened while on excursions and in the lounges!”

The Bear Case: The Capex Crunch and the Hospital Pinch

The fundamental bear case for IHI is about credit/rates inflation and institutional budgeting.

You see, medical device companies don’t just sell single-use scalpels. A major portion of the industry relies on selling multimillion-dollar capital equipment. Like robotic surgical suites and advanced imaging systems.

With interest rates remaining stubbornly high, hospital systems cannot easily finance these massive capital expenditures. They are stretching their existing equipment further and freezing new orders.

In addition, while inflation might be sticky for consumer goods, hospitals are trapped in a brutal margin squeeze. Their labor costs are permanently elevated, but their reimbursement rates from insurance companies and government programs are largely fixed. When hospitals are financially squeezed, they aggressively squeeze their suppliers. The stocks in IHI are among the biggest of those. That in turn forces medical device makers to accept severe price concessions.

Unlike standard value sectors, medical device heavyweights rarely trade at a deep discount. Even after a prolonged period of underperformance, you can see from the graphic above that IHI’s portfolio basket trades at 29x trailing earnings. If the broader economy tilts toward a recession, these premium multiples face a steep re-rating, lower.

Chart courtesy of Rob Isbitts via PiTrade.com

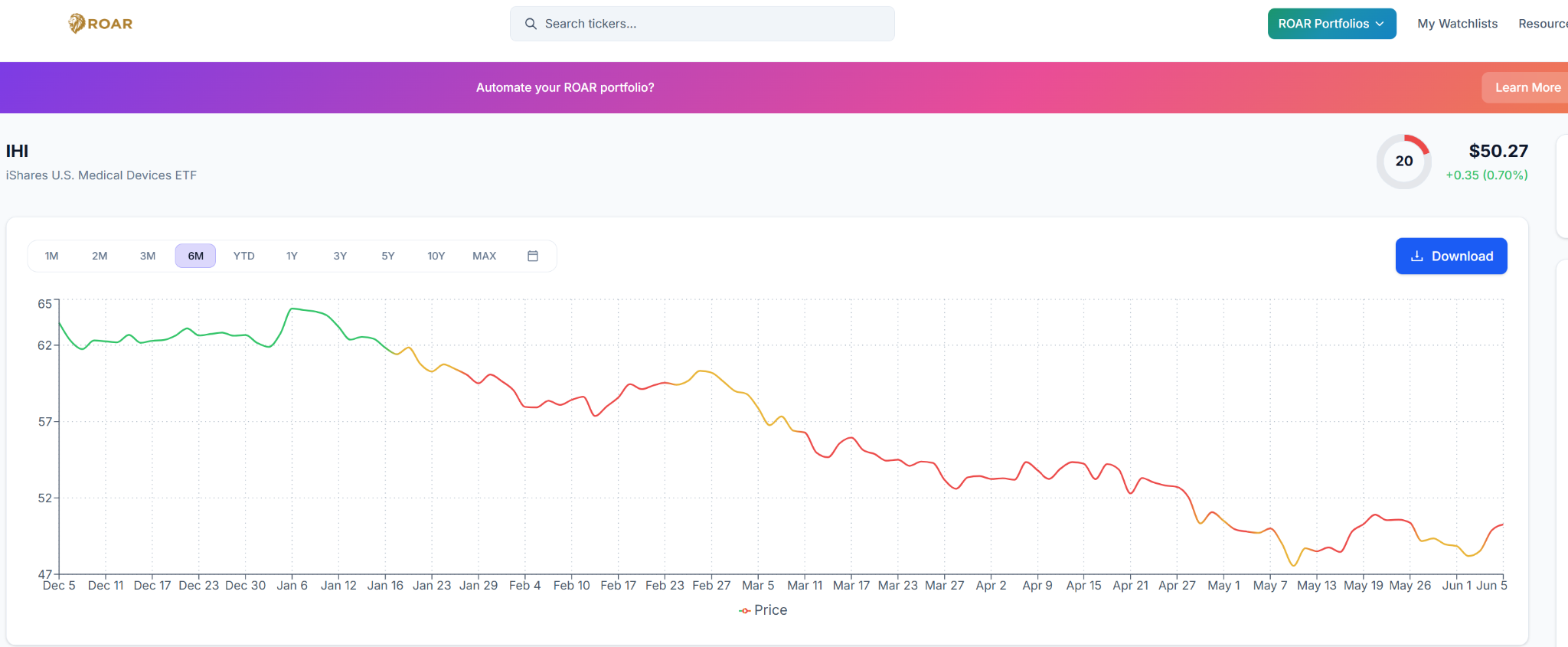

Chart courtesy of Rob Isbitts via PiTrade.com My ROAR Score has been a good guide for IHI over the past year. The score fell from the lower risk (green) zone early this year, around $62 a share. That was the last hope to avoid a decline of significance, which turned out to be a move down to around $47. So ROAR spared a 25% decline over five months. Now down in the higher risk zone for a while, I’ll be looking for a move up into the 30-40 ROAR Score area to take a closer look at this one.

In a market finally showing some degree of vulnerability at the top, nothing is a comfortable, high-percentage trade other than very short-term stuff. But looking beyond that, counting in future quarters and years, I like the return/risk tradeoff down here for IHI.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

When Investors Finally Get Sick of AI Stocks, This Medical Devices ETF Could Be a Long-Term Winner Consumer Staples Stocks Are No Longer a Recession-Proof Haven Amid High Inflation. Just Look at the PBJ ETF. The Dow's Split Personality: Why Some Winners Soar While Others Drag Down the Dow Hunting for the Next Nvidia Is No Easy Feat. Small-Cap Tech Stocks Promise Riches but Really Are Just Rags.