The Broadcom Ltd. (AVGO) stock sell-off last week, following its June 3 Q2 earnings release showing strong FCF growth and higher FCF margins, is likely well overdone. My price target is now over 97% higher at $782 per share. This is based on analysts' revenue forecasts, its high FCF margins, and management's outlook.

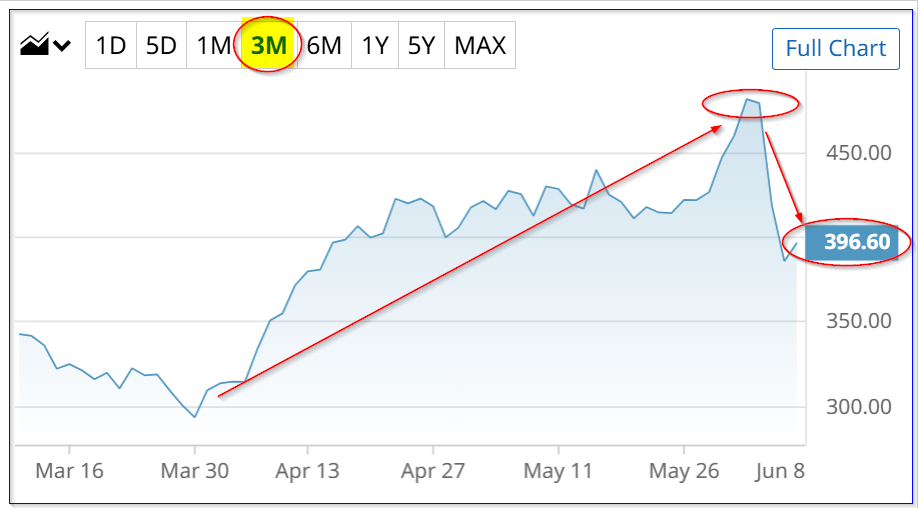

AVGO closed at $396.60 on Monday, June 8, up 2.82%, after tanking last week. The stock hit a closing peak of $481.57 on June 2, right before its earnings release the next day. Then, after the market didn't think it met their expectations, it tanked to $385.73 by Friday, June 5.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

AVGO stock - last 3 months - Barchart - June 8, 2026

AVGO stock - last 3 months - Barchart - June 8, 2026 This $95.84 drop (-19.9%) by last Friday was too much. This article will show why.

Why Broadcom Could Be Worth Much More

First, analysts have maintained their very high revenue forecasts for next year, along with a strong outlook from management, based on AI-related chip demand.

For example, Seeking Alpha now shows that the average analyst revenue forecast for the year ending Oct. 2027 is $170.73 billion.

That is +60.9% higher than their $106.2 billion revenue forecast for this year ending Oct. 31, 2026. Moreover, over the trailing 12 months (TTM) ending this quarter (May 3), Broadcom's revenue was just $75.5 billion, based on data from Stock Analysis.

So, over the next fiscal year, analysts expect almost a $100 billion increase in revenue (i.e., a 126% increase in sales).

That should make investors selling their AVGO shares or shorting them think twice.

Second, Broadcom's free cash flow (FCF) margins have been steadily rising, even after higher revenue and higher capex. For example, over the last quarter, its FCF margin was 46.25% of revenue, higher than last quarter's 41.48% and last year's $42.73% margin.

In addition, over the last year, its TTM FCF margin was 44.34% of revenue, higher than last quarter's 42.34% TTM FCF margin and 39.79% a year ago.

The point is that analysts can depend on Broadcom's ability to maintain a high FCF margin over the next year.

Forecasting FCF

As a result, Broadcom's FCF margin for the year ending Oct. 2027 can be estimated. Here's how:

$170.73 billion revenue x 0.434 FCF margin = $74.1 billion FCF

That is well over twice the $32.762 billion in FCF generated over the past year, according to Stock Analysis.

In other words, one year from now, analysts will be forecasting over $74 billion in FCF for the fiscal year ending Oct. 2027, with two quarters to go. That is undoubtedly likely to push AVGO stock significantly higher.

Here is how AVGO's fair value might work out.

Price Targets for AVGO Stock

Using a FCF yield metric, AVGO's future value might be significantly higher. Here's why.

As of today, Broadcom's market value is $1,878 billion (i.e., $1.878 trillion), according to Yahoo! Finance.

So, if Broadcom were to theoretically out 100% of the $32.762 billion in FCF generated over the past year, its dividend yield would be 1.74%:

$32.762b/ $1,878 billion = 0.01745 = 1.745%

However, just to be conservative, let's use a higher FCF metric to value its future FCF, say 2.0% (just to keep things simple):

$74.1 billion FY 27 FCF / 0.02 = $3,705 billion ($3.7 trillion)

That is 97.3% higher than its present $1.878 trillion market cap. And with some share buybacks, the market cap is likely to be even higher, or double.

As a result, my price target is 97.3% over today's price:

$396.60 x 1.973 = $782.49 price target (PT)

Other analysts have significantly higher price targets than today's price. For example, Yahoo! Finance's survey of 48 analysts is $517.61. That is 30.5% higher than today. Similarly, Barchart's mean survey PT is $507.13 (+27.9% upside). Moreover, AnaChart shows that some recent analysts' write-ups have price targets as high as $582, or 46.7% higher.

The bottom line is that AVGO looks deeply undervalued here, based on its strong FCF margins and analysts' revenue forecasts.

However, there is no guarantee this will happen. One conservative way to play AVGO is to short one-month put options. That way, you can set a lower potential buy-in and get paid while waiting.

Shorting OTM AVGO Puts

For example, the $370 put option, i.e., 6.7% below today's price, expiring July 10, has a midpoint premium of $10.33. That means a short-seller can make a 1-month yield of 2.79% (i.e., $10.33/$370.00).

AVGO puts expiring July 10 - Barchart - As of June 8, 2026

AVGO puts expiring July 10 - Barchart - As of June 8, 2026 Moreover, even if AVGO drops to $370, the investor's breakeven point, given the income already received, is just $359.67:

$370-$10.33 = $359.67, or 9.3% lower

Some enterprising investors will use this income to buy in-the-money (ITM) calls with further out expiry. That way, they can benefit from any upside in AVGO. By repeating this short-put play each month, a good portion of the ITM call premium can be covered.

The bottom line is that using puts and calls selectively like this, an investor can gain a leveraged way to play AVGO.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Following the Post-IPO Quiet Period Expiration, Here’s Why Cerebras Stock Is Moving Higher When Investors Finally Get Sick of AI Stocks, This Medical Devices ETF Could Be a Long-Term Winner Broadcom's Sell-Off Is Overdone - Based on its FCF Margins, AVGO Could Be Worth Double The $115 Million Reason ABAT Stock Is Up Today