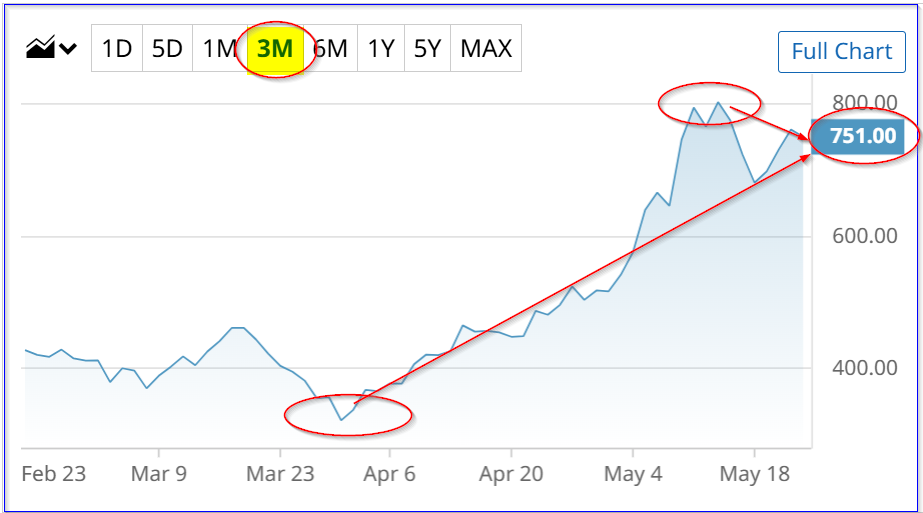

Micron Technology (MU) stock is up 133% from its March 30 low of $321.80, but MU could still be cheap based on its projected free cash flow. Moreover, analysts have raised their price targets. One play is to short out-of-the-money (OTM) put options.

MU closed at $751.00 per share on Friday, May 22, down from a recent peak of $803.63 on May 13. But it could be worth almost 13% more at almost $844, as this article will show.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

MU stock - last 3 months - Barchart - May 22, 2026

MU stock - last 3 months - Barchart - May 22, 2026 Why Micron's FCF Could Spike

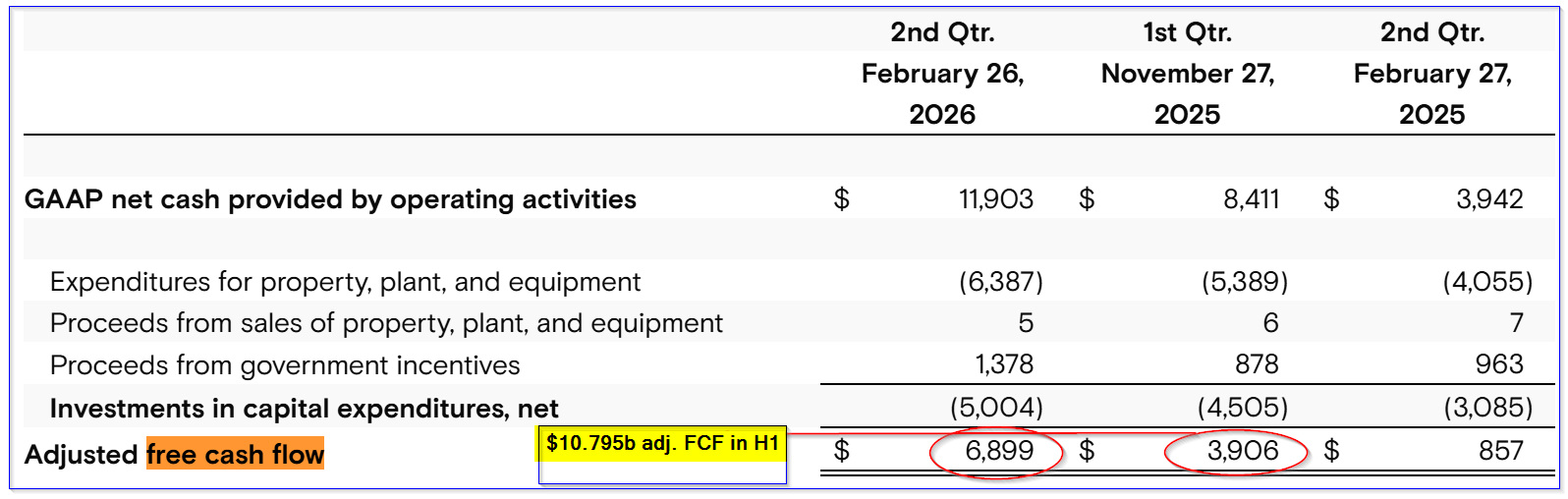

On March 18, Micron posted very strong earnings and free cash flow (FCF) fiscal Q2 margins (ending Feb. 28), as I discussed in my April 14 Barchart article, “Analysts Hike Their Micron Estimates, Pushing MU Stock Price Targets Higher.”

For example, its first-half adjusted FCF margin was 28.83% (i.e., $10.8b/$37.5b revenue), and its Q2 adj. FCF margin was 28.87% (i.e., $6.889b/$23.86b revenue). This can be seen in the table Micron provided:

Micron's First Half (H1) adj. FCF - March 18 fiscal Q1 earnings release

Micron's First Half (H1) adj. FCF - March 18 fiscal Q1 earnings release We can use these to forecast FCF.

For example, analysts now project revenue next year will be $172.76 billion. So, using an average 28.85% FCF margin, its FCF could almost reach $50 billion:

$172.76 billion revenue x 0.2885 = $49.84 billion FCF

Last quarter, Micron was on a run-rate FCF of just $27.6 billion (i.e., $6.6889 billion Q1 adj. FCF x 4). In other words, we can reasonably expect Micron's adj. FCF to rise 82.5% next year.

As a result, we can expect its price target to be substantially higher.

MU Price Targets

For example, assuming the market values this FCF estimate at a 5.0% FCF yield, i.e., 20x FCF. That would give Micron a fair value of almost $1 trillion:

$49.84b adj. FCF 2027 x 20 = $996.8 billion

That is +17.7% higher than Micron's market cap today (i.e., $846.92 billion, according to Yahoo! Finance).

But, just to be conservative, let's assume the market's lower valuation range is a 5.5% FCF yield, i.e., an 18.18x multiple (i.e., 1/0.055 = 18.18x):

$49.84b x 18.18 = $906.1 billion

That's 7% higher than today's price. As a result, MU's price target (PT) range is between 7% to 17.7%, or +12.35% higher, on average:

$751.00 x 1.1235 = $843.75 per share PT

This is higher than other analysts' PTs. For example, Yahoo! Finance's survey of 44 analysts shows an average PT of $613.22. However, that is up from $551.40 on May 5, when I last wrote about MU stock. In other words, Street analysts are playing catch-up.

Nevertheless, there is no guarantee MU will keep rising. As a result, one conservative way to play MU is to short out-of-the-money (OTM) puts.

That way, an investor can set a lower potential buy-in point and get paid while waiting.

Shorting OTM MU Puts

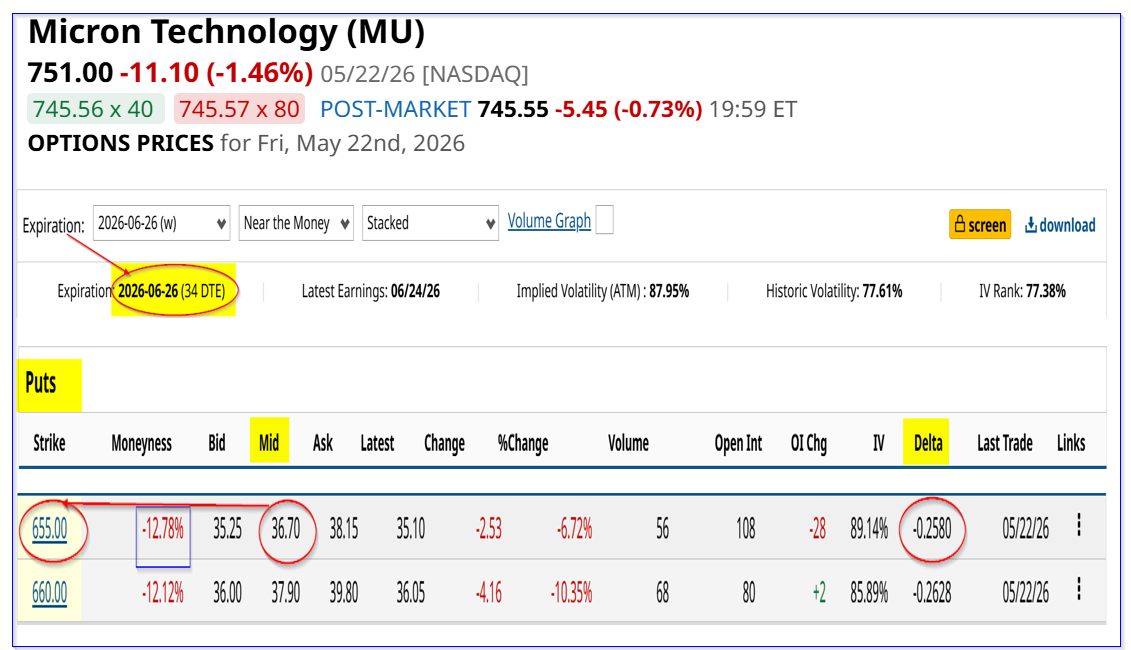

The June 26 expiry period shows that deep out-of-the-money (OTM) MU puts have high premiums. For example, the $655.00 strike price put option, which is 12.78% below Friday's close (i.e., out-of-the-money, since MU would have to fall almost 13% before the put has any value), still has a high midpoint premium: $36.70:

MU puts expiring June 26 - Barchart - as of May 22, 2026

MU puts expiring June 26 - Barchart - as of May 22, 2026 That means an investor can sell this put option short and receive a 1-month yield of 5.60% (i.e., $36.70/$655.00).

That is because the investor only has to secure $65,500 with their brokerage firm as collateral to buy 100 shares should MU fall to $655.00. In return, the buyer of the put pays the short seller $3,670 (i.e., 100 shs per put contract x $ 36.70). So, the income return is:

$3,670 / $65,500 invested at $655.00 for 1 month = 0.056 = 5.60% 1 month yield

Downside Issues

Note that the delta ratio is only 0.2580, implying just over a ¼ chance that MU will drop to $655.00 by June 26. That shows there is good protection on the downside.

However, even if that happens, the investor has a much lower breakeven point:

$655.00 - $36.70 = $618.30 B/E

That is 17.7% below Friday's close of $751.00. In other words, the investor would have a great potential buy-in point.

After all, if MU rises to $844 over the next year, the investor would make a 36.5% total return. In addition, if an investor can repeat this play over 3 months, the net expected return is:

0.056 x 3 = 16.8%

That's equivalent to MU rising to $877 per share, well over my price target.

Nevertheless, if MU drops below the breakeven price, shorting OTM puts can result in an unrealized loss. At that point, the investor could sell short OTM puts or covered calls to mitigate any unrealized loss.

The bottom line is that MU stock could be cheap here. But one conservative play is to sell short put options at deep out-of-the-money strike prices to gain income and potentially buy at a lower price.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Micron Stock is Up over 133% From Its Lows - But Is MU Still Undervalued? Can November Soybeans Challenge Contract Highs? Strong Crush Demand and Seasonal Strength Say It's Possible Unusual Options Activity in CSX Stock Could Signal More Upside Ahead Abbott Laboratories Stock Is Getting Decimated, But the Smart Money Senses Opportunity