Johnson & Johnson JNJ and AstraZeneca AZN are among the largest global drugmakers, each supported by a diversified healthcare business. Both maintain a significant footprint in oncology. Beyond cancer treatments, J&J markets therapies across immunology, neuroscience, cardiovascular and metabolic disorders, pulmonary hypertension and infectious diseases, while also holding a leading position in medical devices.

At AstraZeneca, oncology contributes roughly 44% of total revenues. The company has also established franchises in immunology, rare diseases, vaccines, and cardiovascular and respiratory care.

Both companies are facing key patent losses that are somewhat hurting sales. So, which stock offers the stronger investment case today? A review of their business fundamentals, growth drivers and risks can help answer that question.

The Case for J&J Stock

J&J’s biggest strength is its diversified business model, as it operates through pharmaceuticals and medical devices divisions. It has more than 275 subsidiaries and boasts 28 platforms or products with more than $1 billion in annual sales, with the aim of adding even more. Its diversification helps it withstand economic cycles more effectively. It also boasts strong cash flows and has increased its dividends for 64 consecutive years. J&J believes that the depth of its portfolio and pipeline is stronger than ever.

J&J’s Innovative Medicine unit is showing a growth trend. The segment’s sales rose 5.6% on an organic basis in the first quarter of 2026 despite the loss of exclusivity (LOE) of the blockbuster drug, Stelara, in 2025. Growth was driven by J&J’s key drugs like Darzalex, Erleada and Tremfya. New drugs like Carvykti, Tecvayli, Talvey, Rybrevant and Spravato also contributed significantly to growth.

The company’s MedTech business has improved in the past four quarters, driven by the acquired cardiovascular businesses, Abiomed and Shockwave, as well as Surgical Vision and wound closure in Surgery. Improvements in J&J’s electrophysiology business also drove growth. MedTech sales rose 4.7% on an organic basis in the first quarter.

J&J also rapidly advanced its pipeline in the past year, attaining significant clinical and regulatory milestones that will help drive growth through the back half of the decade. Key new drugs approved recently are Inlexzoh/TAR-200, a first-of-its-kind drug-releasing system, for treating high-risk non-muscle invasive bladder cancer, Imaavy (nipocalimab) for generalized myasthenia gravis and J&J and partner Protagonist Therapeutics’ PTGX oral targeted peptide inhibitor of the IL-23 receptor, Icotyde (icotrokinra) for treating moderate-to-severe plaque psoriasis (PsO).

In 2025, J&J invested more than $32 billion in R&D and M&A, including the acquisitions of Intra-Cellular Therapies and Halda Therapeutics. Backed by regular pipeline success, J&J expects a more pronounced impact from new products in 2026 than in 2025.

J&J believes 10 of its new products/pipeline candidates in the Innovative Medicine segment have the potential to deliver peak sales of $5 billion, including Talvey, Tecvayli, Imaavy, Caplyta, Inlexzo, Rybrevant, Lazcluze and Icotyde.

J&J expects 2026 to be a year of accelerated growth. The company expects both its Innovative Medicines and MedTech segments to deliver stronger growth this year. The company is confident that it can achieve its target of generating around $100 billion in revenues in 2026. It expects sales to continue to improve in 2027, with a “line of sight” to double-digit growth by the end of the decade. J&J believes that it is already achieving this growth. Though J&J’s total revenues are currently rising in a mid-single-digit range, excluding Stelara, J&J’s top line grew in a double-digit range in the first quarter.

However, J&J faces its share of headwinds like the legal battle surrounding its talc lawsuits, the Stelara patent cliff, the upcoming LOE of key drugs Opsumit and Simponi, and softness in MedTech China.

The Case for AstraZeneca

AstraZeneca now has 16 blockbuster medicines, including Tagrisso, Fasenra, Farxiga, Imfinzi, Lynparza, Soliris and Ultomiris in its portfolio, with sales (product sales and alliance revenues) exceeding $1 billion. These drugs drove AstraZeneca’s 8% top-line growth and 5% core EPS at CER in the first quarter of 2026, backed by increasing demand trends.

Newer drugs like Wainua, Airsupra, Saphnelo, Datroway (partnered with Daiichi Sankyo) and Truqap also contributed to top-line growth, more than offsetting the loss of exclusivity of some mature brands like Brilinta, Pulmicort and Soliris.

In 2026, AZN expects continued revenue and earnings growth. It expects total revenues to grow by a mid-to-high single-digit percentage at CER in 2026, while core EPS is expected to increase by a low double-digit percentage at CER.

AstraZeneca has set itself some visible targets for the next few years. It expects to generate $80 billion in total revenues by 2030. By the said time frame, AstraZeneca plans to launch 20 new medicines, with around half of these already launched/approved. It believes that many of these new medicines will have the potential to generate more than $5 billion in peak-year revenues. The company is also on track to achieve a mid-30s percentage core operating margin by 2026.

AstraZeneca’s pipeline is also strong, with pivotal data readouts lined up for 2026.

However, AstraZeneca faces LOE risks for several blockbuster drugs. Generic erosion is already hurting sales of Brilinta and Soliris in some markets. Sales of key drug Farxiga are expected to be pressured in 2026 due to the LOE in some countries like the United States, the United Kingdom, Japan and China. Also, China, though an important market for AstraZeneca, remains a somewhat uncertain market due to pricing pressure from volume-based procurement (VBP) programs and ongoing legal and compliance investigations involving the company’s former China head, Leon Wang.

How Do Estimates Compare for JNJ & AZN?

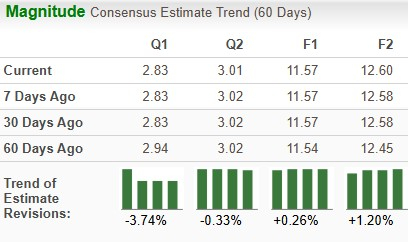

The Zacks Consensus Estimate for J&J’s 2026 sales and EPS implies a year-over-year increase of 7.02% and 7.2%, respectively. The Zacks Consensus Estimate for 2026 earnings has risen from $11.54 per share to $11.57 over the past 60 days.

JNJ Estimate Movement

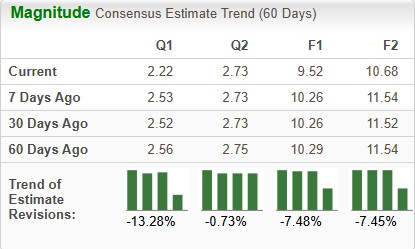

The Zacks Consensus Estimate for AstraZeneca’s 2026 sales and EPS implies a year-over-year increase of 7.02% and 7.2%, respectively. The Zacks Consensus Estimate for 2026 earnings has declined from $10.29 per share to $9.52 per share over the past 60 days.

AZN Estimate Movement

Price Performance and Valuation of J&J & AZN

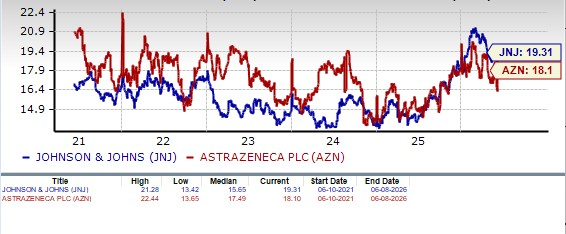

In the past year, J&J’s stock has risen 49.6%, while AstraZeneca’s stock has risen 24.4%, compared with the industry’s increase of 24.7%

J&J looks slightly more expensive than AstraZeneca from a valuation standpoint. Going by the price/earnings ratio, J&J’s shares currently trade at 19.31 forward earnings, higher than 18.10 for AstraZeneca. However, both J&J and AstraZeneca are trading above the industry as well as their 5-year mean.

Johnson & Johnson's dividend yield is 2.3%, while AstraZeneca’s is 2.4%.

AZN or JNJ: Which is a Better Pick?

Both J&J and AstraZeneca have done well in 2025 and look optimistic for continued growth in 2026 despite patent losses for some key drugs. Both stocks have risen in the past year. Both stocks have a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

This makes choosing one stock a difficult task. However, J&J has shown steady revenue and EPS growth for years and expects further growth in 2026. Despite headwinds like the legal battle surrounding its talc lawsuits, the Stelara patent cliff, the upcoming LOE of key drugs Opsumit and Simponi and softness in MedTech China, J&J looks quite confident that it will be able to navigate these challenges. The stability in J&J’s performance makes us choose J&J over AZN.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AstraZeneca PLC (AZN): Free Stock Analysis Report

Johnson & Johnson (JNJ): Free Stock Analysis Report

Protagonist Therapeutics, Inc. (PTGX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).