United Rentals, Inc. (URI), headquartered in Stamford, Connecticut, functions as an equipment rental company. Valued at $58.8 billion by market cap, the company offers a wide range of construction and industrial equipment for rent, sale, and servicing, including general and specialized machinery, tools, safety gear, storage solutions, power and climate control systems, and repair and maintenance services.

Shares of this rental giant have outperformed the broader market over the past year. URI has gained 37.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 29.6%. In 2026, URI stock is up 19%, surpassing the SPX’s 9.8% rise on a YTD basis.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Zooming in further, URI’s outperformance is also apparent compared to the State Street Industrial Select Sector SPDR ETF (XLI). The exchange-traded fund has gained about 23.8% over the past year. Moreover, the stock’s gains on a YTD basis outshine the ETF’s 12.4% returns over the same time frame.

www.barchart.com

www.barchart.com URI’s outperformance drove a strong market reaction on robust demand from construction, infrastructure, and specialty rentals. CEO Matthew Flannery cited healthy growth in general and specialty segments, with power, mining, infrastructure, and data centers leading. Additionally, $45 million in “surgical” restructuring from branch consolidation and labor management supported costs. The company kept capital disciplined, boosted fleet utilization, and made about $400 million in small, strategic specialty acquisitions. Moreover, Flannery sees multiyear tailwinds from large projects.

On Apr. 22, URI reported its Q1 results, and its shares skyrocketed 22.9% in the following trading session. Its adjusted EPS of $9.71 surpassed Wall Street expectations of $9.01. The company’s revenue was $4 billion, topping Wall Street forecasts of $3.9 billion. URI expects full-year revenue in the range of $16.9 billion to $17.4 billion.

For the current fiscal year, ending in December, analysts expect URI’s EPS to grow 11.9% to $47.07 on a diluted basis. The company’s earnings surprise history is disappointing. It missed the consensus estimates in three of the last four quarters while beating the forecast on another occasion.

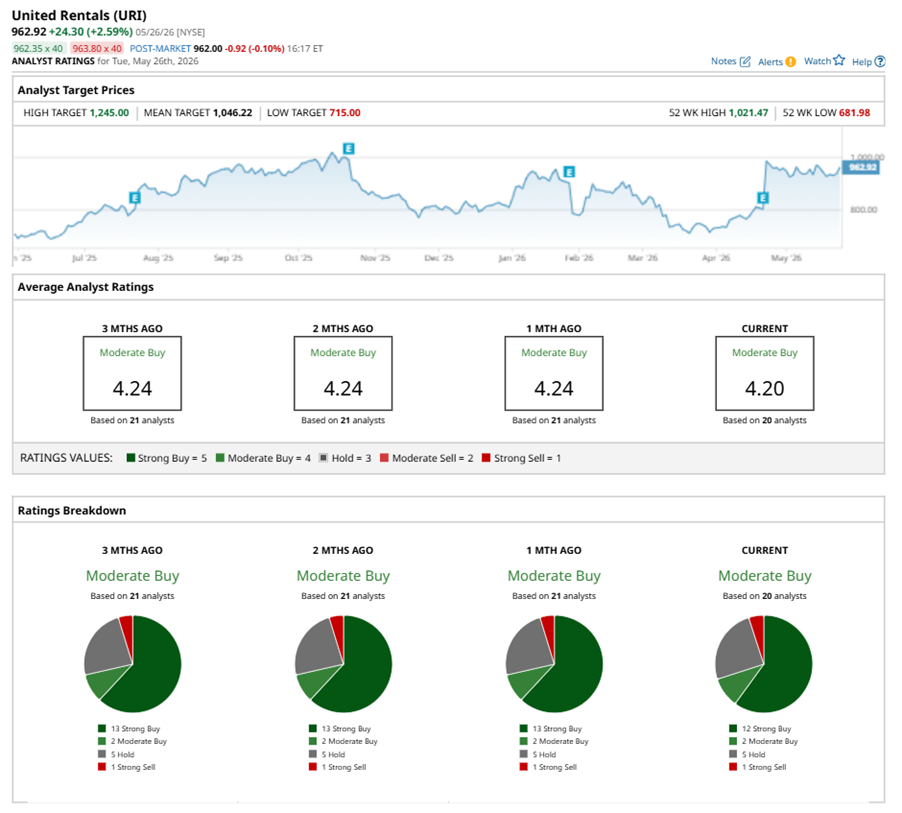

Among the 20 analysts covering URI stock, the consensus is a “Moderate Buy.” That’s based on 12 “Strong Buy” ratings, two “Moderate Buys,” five “Holds,” and one “Strong Sell.”

www.barchart.com

www.barchart.com This configuration is less bullish than a month ago, with 13 analysts suggesting a “Strong Buy.”

On May 13, Wells Fargo & Company (WFC) analyst Jerry Revich reiterated a “Buy” rating on URI and set a price target of $1245, the Street-high price target, implying a potential upside of 29.3% from current levels.

The mean price target of $1,046.22 represents an 8.7% premium to URI’s current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.