As the deadline approached on President Trump's promise to bomb Iran "to the Stone Ages," he declared a two-week ceasefire, removing the immediate threat to the Strait of Hormuz. West Texas Intermediate crude futures (CLK26) dropped 16% to $94.55 a barrel, while Brent crude (CBM26) fell 13.8% to $94.13. The move erased the geopolitical premium that had pushed prices above $110 earlier in the week.

Oil stocks followed suit, plunging 5% to 8% or more in premarket trading as traders priced in the return of ample supply. Yet one name stands out as one to buy regardless of whether this truce holds or not: ExxonMobil (XOM).

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

A Fragile Truce That Shook the Market

The ceasefire buys time, nothing more. It hinges on a 10-point proposal delivered by intermediaries in Pakistan and requires Iran to allow temporary safe passage through the Strait of Hormuz, which carries one-fifth of global oil. Key terms—long-term sanctions relief, permanent reopening of the strait, and verification mechanisms—remain unresolved.

Granted, the pause sparked a broader market rally, with the S&P 500 ($SPX) futures jumping more than 2%, but for energy names, the relief translated into selling pressure. Pure-play producers, which rely heavily on high prices, dropped hardest. The truce could collapse as quickly as it formed if negotiations stall. That uncertainty leaves most oil stocks exposed. So, here's why Exxon is the exception.

www.barchart.com

www.barchart.com ExxonMobil Is Resilient No Matter What Happens Next

ExxonMobil stands apart because it was built for exactly this kind of normalization. Unlike upstream-only peers that need $80-plus oil to break even, XOM’s diversified operations—upstream production, refining, chemicals, and LNG—generate cash across price cycles. Its latest full-year results show $28.8 billion in GAAP net income and $52 billion in cash flow from operations for 2025, even as average WTI prices fell 16% year-over-year (YoY) in the fourth quarter.

Production hit 4.7 million oil-equivalent barrels per day, the highest in more than 40 years. Structural cost savings reached $15.1 billion since 2019, lowering its supply costs to levels that stay profitable below $60 a barrel.

That’s a fancy way of saying XOM doesn’t need another oil spike to deliver returns. When crude prices drop, its refining margins often expand because feedstock gets cheaper. The company distributed $37.2 billion to shareholders through dividends and buybacks in 2025 alone. Believe it or not, this cash machine keeps running whether the truce holds or tensions flare again.

The Numbers That Matter and How XOM Stacks Up

Here’s what the data reveal when you compare XOM to the sector:

Forward P/E ratio: 20.09 (versus the energy sector average closer to 18 for higher-risk names, but with far lower volatility). Dividend yield: 2.46% (paid consistently), with a payout ratio of just 59.70%—leaving room for growth even if prices stay soft. Levered free cash flow: $12.23 billion (TTM), funding both the dividend and $15 billion-plus in planned 2026 capital spending without strain. Beta: 0.29 (60-month), meaning XOM moves only about one-third as much as the broader market—ideal for safety-focused investors.Contrast that with pure upstream peers or European majors like Shell (SHEL) and BP (BP), which lack the same downstream cushion. XOM’s low breakeven and 4.9 million barrels-per-day production guidance for 2026 position it to grow earnings $3 billion next year at constant prices. It is clear these figures turn volatility into opportunity.

www.barchart.com

www.barchart.com What Wall Street Sees

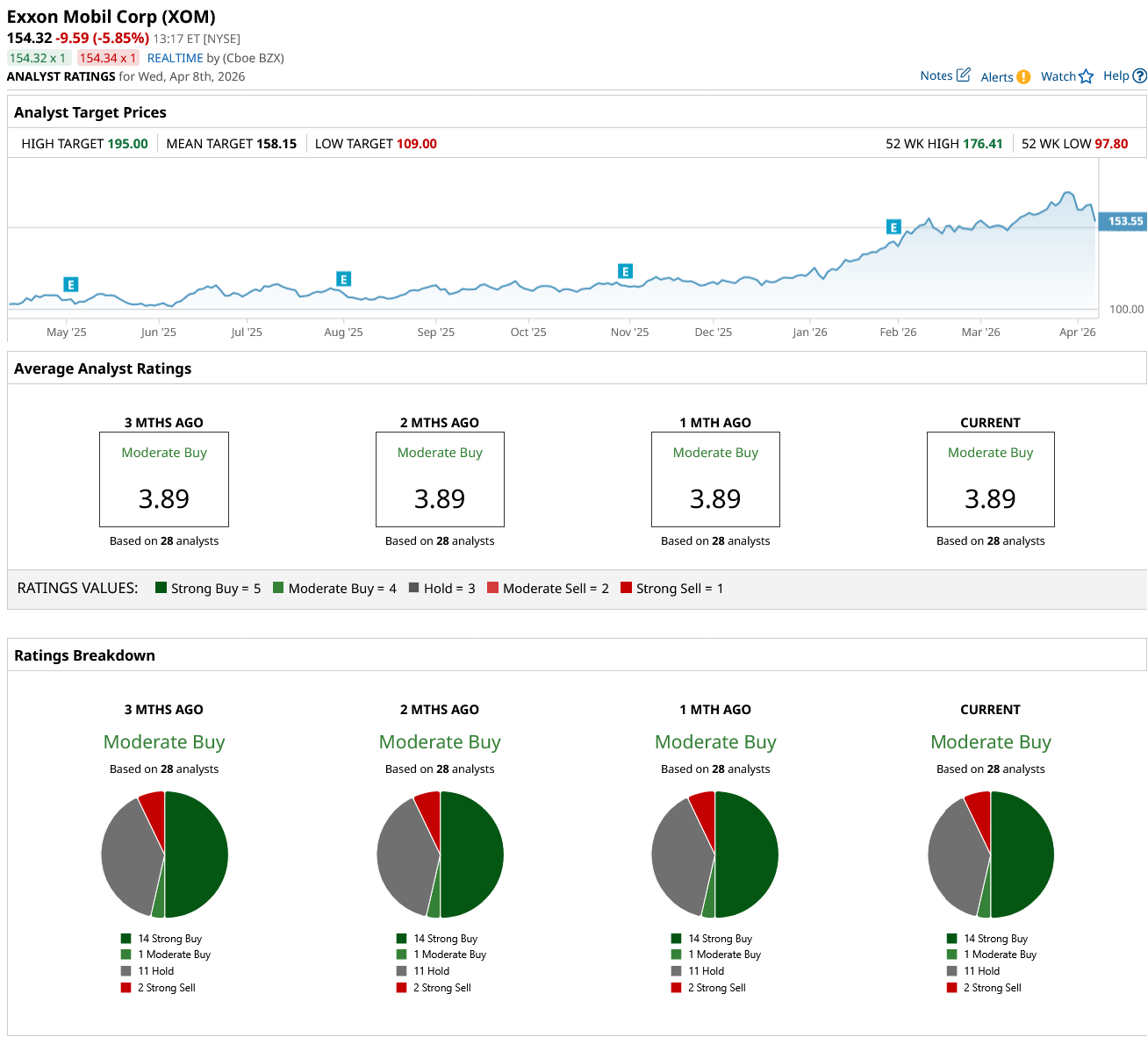

According to Barchart’s analyst ratings page, 28 analysts cover XOM and rate it a "Moderate Buy." There are 14 "Strong Buy" ratings, one "Moderate Buy," 11 "Hold" and two "Strong Sell" ratings.

The mean price target sits at $158.15, with a high of $195 and a low of $109. That suggests modest near-term caution after the rally, but the consensus still points to long-term value for patient holders.

Key Takeaway

All in all, the 16% oil collapse highlights how quickly premiums vanish. Yet ExxonMobil’s integrated model, $52 billion cash flow machine, 2.46% yield, and low-breakeven assets make it the one oil stock worth owning today—truce or no truce.

Passive income investors seeking steady dividends and resilience should view the current dip as a chance to add shares at a reasonable valuation.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Oil Prices Crash 16% on Iran War Ceasefire—Why ExxonMobil Is Still the Only Buy That Makes Sense Bearish Outlook? Try These 2 Bear Call Spread Trades on Thursday Stocks Slip Before the Open as Oil Rebounds Amid Fragile U.S.-Iran Ceasefire, PCE Inflation and GDP Data in Focus Lockheed Martin Stock Is Up 30% in 2026 and Yields 2%. Is It a Top Buy While the Iran War Drags On?