Intel (INTC) stock was once among the laggards in the technology space. However, with growing AI demand and innovation, the company’s turnaround has gained momentum. INTC stock has surged by 225% in the last 52-weeks.

The momentum has been unabated in fiscal 2026, and with Intel scheduled to report first-quarter fiscal 2026 results on April 23, investors have reasons to remain optimistic. For Q1, the company has already provided healthy revenue guidance of $12.2 billion at the midpoint with a gross margin of 34.5%.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Intel is already shipping products built on Intel 18A. At the same time, the development of 14A coupled with customer engagement provides an additional catalyst for the company. It’s also worth adding that the potential increase in pricing for Intel’s servers and client CPUs is a trigger for margin expansion. Considering these factors, Intel will likely remain a strong turnaround story.

About Intel Stock

Headquartered in Santa Clara, California, Intel is a designer and manufacturer of advanced semiconductors. The company has global presence and operates several segments, including its Client Computing Group (CCG) and Data Center and AI (DCAI) segment.

Intel's CCG segment delivers platforms and processors for PCs and edge devices. The segment also caters to industries that include retail, industrial robotics and AI ecosystems. Meanwhile, DCAI delivers workload-optimized solutions based on x86 architecture for data centers. The segment supports workloads in AI, analytics, and more.

Intel has invested more than $46 billion in research and development between fiscal 2023 and fiscal 2025. These investments have focused on next-generation process technologies and are likely to yield results in the coming years.

For fiscal 2025, Intel reported revenue of $49.1 billion with a healthy operating margin of 26%. For the same period, the company’s operating cash flow was $9.7 billion.

With the company focused on capitalizing on the significant AI-driven opportunity, INTC stock has trended higher by 57% in the last six months. The positive momentum is likely to sustain after Intel reports Q1 results.

www.barchart.com

www.barchart.com Pushing for Growth

Intel claims that 18A is the “most advanced process technology” developed in the United States. With the beginning of mass production, the company has reached a manufacturing inflection point.

The company's September 2025 partnership with Nvidia (NVDA) is another potential value creator. Nvidia has invested $5 billion in Intel common stock and the collaboration will jointly develop custom data-center and PC products. The partnership also provides diversification for Nvidia, with the company’s AI chips relying heavily on Taiwan-based fabrication.

In another important development, Intel has joined the Terafab project — which includes SpaceX, xAI, and Tesla (TSLA) — to support “refactor silicon fab technology.” Finally, a recent report indicated that Intel is in talks with Amazon (AMZN) and Alphabet (GOOGL) for advanced packaging services. All of these developments and collaborations point to an innovation-driven turnaround story with ample headroom for value creation.

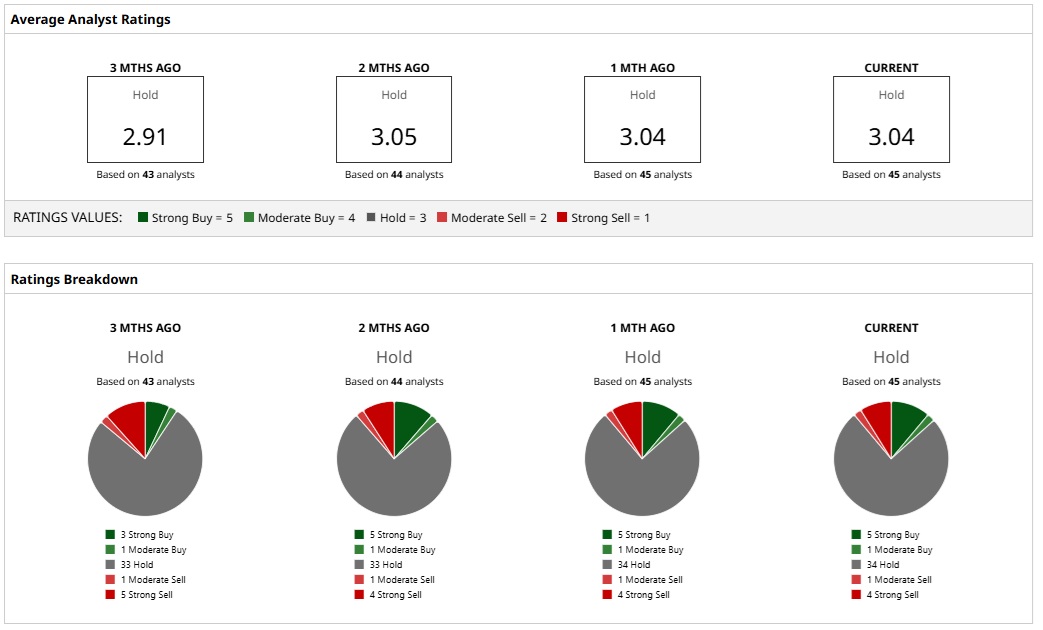

What Do Analysts Say About INTC Stock?

Based on 45 analysts with coverage, INTC stock has a consensus “Hold” rating. Five analysts have a “Strong Buy” rating for INTC stock, one analyst has a “Moderate Buy,” 34 analysts have a “Hold” rating, one analyst has a “Moderate Sell,” and four analysts have a “Strong Sell” rating.

The mean price target of $45.26 represents potential downside of 23% from current levels. However, the most bullish price target of $66 suggests that INTC stock could climb 12% from here.

It’s worth noting that analysts expect earnings growth of 150% and 766% for fisal 2026 and fiscal 2027, respectively. While the stock has surged in the last 52 weeks, earnings momentum is likely to keep sentiment positive.

In terms of recent analyst coverage, KeyBanc reiterated its “Overweight” rating on the stock with a price target of $70. A key factor for the bullish outlook is an increase in pricing for Intel’s server and client CPUs. At the same time, yields on the company’s 18A manufacturing node continue to improve.

www.barchart.com

www.barchart.com On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Intel Stock Fans, Mark Your Calendars for April 23 Tech Stocks Are Experiencing Historic 50-Year Weakness. Should You Buy the Dip in This 1 ETF? Why Wedbush Says You Should Buy Nvidia Stock Now Amid the 2-Week Ceasefire Does New Profitability Guidance Make FuboTV Stock a Buy Now?