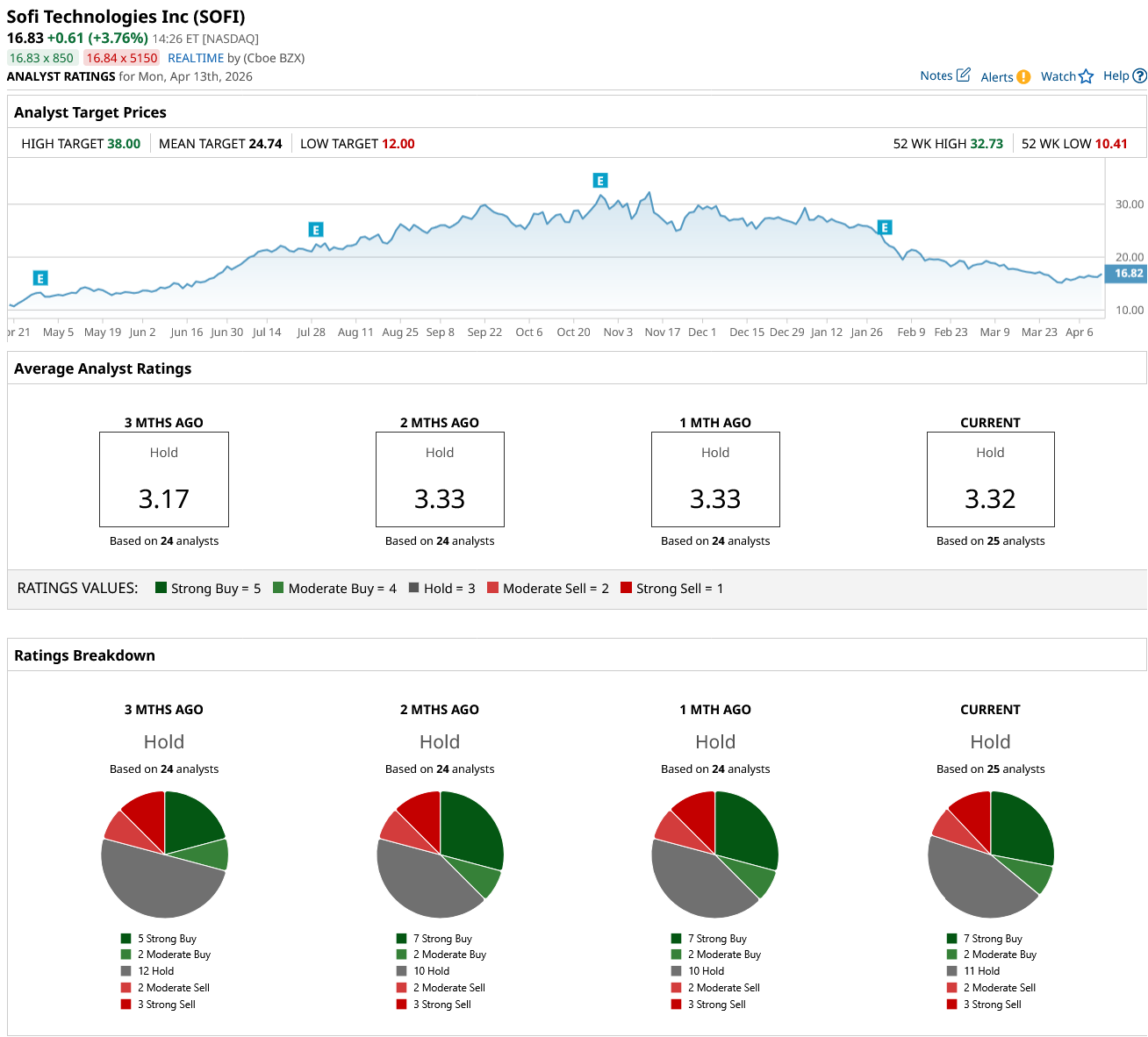

Shares of SoFi Technologies (SOFI) have declined sharply in recent months, falling more than 38% over the past three months and correcting by more than 48% from their 52-week high of $32.73. The steep pullback reflects a combination of company-specific and macroeconomic concerns that have weighed on investor sentiment.

Part of the pressure stems from concerns about potential equity dilution following the company’s recent capital raises. Investors have also reassessed the stock’s valuation after a strong rally, which left shares trading at elevated levels relative to historical benchmarks. At the same time, broader macroeconomic uncertainty, including ongoing geopolitical tensions and the impact of artificial intelligence (AI) technology on jobs, has contributed to a more cautious market environment for financial technology companies.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Sentiment weakened further after short seller Muddy Waters Research disclosed a short position in the company and accused SoFi of using misleading accounting practices. SoFi rejected the claims, describing the report as inaccurate and defending the integrity of its financial disclosures.

These developments have placed SOFI stock under pressure ahead of the company’s first-quarter earnings release on April 29.

www.barchart.com

www.barchart.com SoFi Q1: Here’s What to Expect

Despite the market volatility, SoFi’s business performance has remained strong, with both revenue and profitability continuing to grow at a solid pace.

The financial services company has also diversified its revenue streams. While lending remains a core business, SoFi has expanded into fee-based and capital-light segments that offer more stable, scalable income streams. This revenue mix shift has lowered dependence on interest-sensitive lending revenue and may support more resilient margins over the long term.

Management has addressed investor concerns about share dilution. According to the company, the capital raised through these measures has strengthened its balance sheet. SoFi has used part of the proceeds to retire higher-cost debt, which helps lower interest expenses. At the same time, the company has been able to allocate excess capital toward yield-generating assets, creating an additional stream of interest income.

Looking ahead to the first quarter, SoFi expects adjusted net revenue of about $1.04 billion. That would represent a 35% year-over-year (YoY) increase, slightly higher than the 33% growth recorded in the same quarter last year. A major driver of this expected growth is the continued expansion of the company’s member base. In the fourth quarter of 2025, SoFi added 1 million new members, bringing its total membership to 13.7 million, an increase of 35% compared with the previous year.

Customer engagement with the platform has also remained strong. During the same quarter, SoFi added 1.6 million new products, pushing total product growth to 37% YoY. Cross-buying activity has been encouraging, with around 40% of new products coming from existing members. This suggests that the company is attracting new users and encouraging existing customers to adopt multiple services within its ecosystem.

This momentum is expected to continue into the first quarter. Stronger revenue growth should support further enhancements in profitability. SoFi is projecting adjusted EBITDA of around $300 million, translating to a margin of roughly 29%, compared with 27% in the same period last year.

Earnings are also expected to improve significantly. Adjusted earnings are projected to reach about $0.12 per share, double the $0.06 reported a year earlier. Analysts covering SOFI stock are forecasting a similar figure. Notably, SoFi has surpassed analysts’ EPS estimates in each of the past four quarters, strengthening expectations that it could deliver another solid performance when it reports its upcoming results.

Is SOFI Stock a Buy Ahead of Q1?

SoFi could once again deliver solid growth in Q1, led by member and product expansion and solid momentum in the fee-based revenue. However, broader macroeconomic uncertainty and subdued market sentiment warrant caution.

Wall Street analysts currently maintain a consensus “Hold” rating on SOFI stock ahead of the company’s first-quarter earnings announcement.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

On Semiconductor Pops on Analyst Upgrade. Should You Buy ON Stock Here? A $21 Billion Reason to Buy CoreWeave Stock Now Oracle (ORCL) Stock May Be Priced at a Genuine Discount As Waymo Launches in Nashville, Should You Buy, Sell, or Hold GOOGL Stock?