Energy stocks are quietly gaining attention in 2026. While broader markets remain cautious amid inflation concerns and geopolitical uncertainty, oilfield services companies, in particular, are performing well. Rising crude prices — driven by Middle East tensions and supply disruptions — have created a supportive backdrop for the sector. Against this backdrop, National Energy Services Reunited Corp. NESR has emerged as a standout performer. The stock has surged sharply, backed by solid operational momentum and strong exposure to the Middle East and North Africa (“MENA”) region. But after such a steep rally, investors may wonder: Is NESR still a buy? Let’s explore.

NESR’s Price Momentum Backed by Sector Strength

NESR’s recent stock performance has been nothing short of impressive. The shares have more than doubled in the past six months, significantly outperforming established players like Weatherford International WFRD and SLB N.V. SLB, which gained 64% and 60%, respectively. This outperformance reflects both company-specific execution and a broader sector uplift driven by rising oil prices.

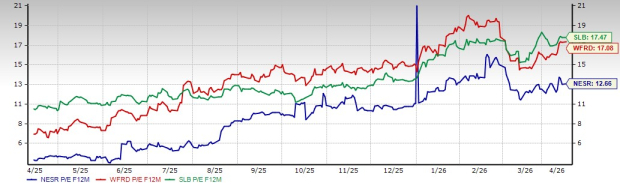

6-Month Price Performance

Higher crude prices tend to act as a direct catalyst for oilfield service providers. As operators ramp up drilling and completion activity, demand for services increases sharply. This dynamic has supported strong performance not just for NESR but also for Weatherford and SLB. However, NESR’s sharper rally suggests that investors are assigning a premium to its MENA-focused growth story and execution consistency.

Earnings Growth and Valuation Offer Upside Potential

Despite its strong price run, NESR’s valuation remains compelling. On a forward price-to-earnings basis, the stock still trades at a discount compared to Weatherford and SLB. This is notable, especially given its superior growth profile.

Valuation Comparison

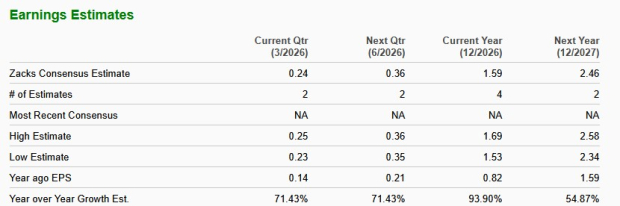

The earnings outlook further strengthens the case. The Zacks Consensus Estimate points to nearly 94% earnings growth in 2026, followed by another 55% increase in 2027. In contrast, both Weatherford and SLB are expected to see earnings decline in 2026. This divergence highlights NESR’s unique positioning and stronger growth visibility.

When a company delivers strong earnings growth but still trades at a relatively low valuation, it often leaves room for further gains. If NESR continues to perform well and meets expectations, its valuation gap with peers could narrow, supporting additional upside in the stock price.

MENA Exposure Driving Structural Growth

NESR’s core strength lies in its deep exposure to MENA, a region witnessing massive upstream investment. With nearly $300 billion in planned spending through 2030, the region offers long-cycle visibility rarely seen in oilfield services.

The company is already benefiting from this trend. Its recent quarterly revenues surged nearly 35% sequentially, driven by project ramp-ups like Jafurah in Saudi Arabia and increased activity across North Africa. Importantly, these are not short-term gains. NESR has a tender pipeline of $2-$3 billion, with multiple awards expected through 2026.

Peers like Weatherford and SLB are also seeing strong momentum in the region. Weatherford continues to benefit from steady activity across Kuwait, Oman, and the UAE, while SLB is witnessing a rebound in drilling and intervention work across key markets. However, NESR’s more concentrated exposure gives it higher leverage to this growth cycle.

As Middle East commodity prices rise due to geopolitical disruptions, national oil companies are accelerating investments. This directly translates into higher service demand, positioning NESR as a key beneficiary of both pricing strength and activity growth.

NESR’s Operational Momentum and Cash Flow Strength

NESR’s growth story is not just about market positioning — it is also about execution. The company delivered strong revenue and earnings growth during the latest quarter, with EPS beating expectations and margins holding steady despite rapid expansion.

Key projects like Jafurah are also evolving into profitability drivers. Margins have already crossed 21% and are expected to improve further as operations stabilize and scale efficiencies kick in. This operational leverage is critical, especially in a competitive pricing environment.

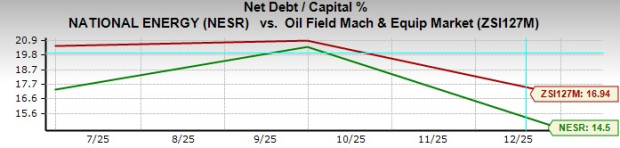

Financially, NESR remains in a strong position. The company generated over $264 million in operating cash flow and maintains low leverage, with net debt well below industry averages. This balance sheet strength provides flexibility to fund growth, pursue new contracts, and potentially return capital to its shareholders.

In comparison, while Weatherford and SLB also maintain solid financial profiles, NESR’s combination of high growth and low leverage stands out. This reinforces its ability to sustain momentum even in a volatile macro environment.

Risks to Watch

That said, the story is not without risks. NESR’s heavy reliance on the MENA region exposes it to geopolitical disruptions. Events like the temporary closure of the Strait of Hormuz have already impacted drilling activity and caused short-term volatility.

Additionally, margin pressures remain a concern. Competitive contract pricing and project mix shifts could limit near-term profitability expansion. While growth remains strong, execution missteps or delays in contract awards could impact earnings visibility.

Finally, the stock’s sharp rally itself introduces risk. After a more than 120% surge, expectations are elevated. Any disappointment — whether operational or macro-driven — could lead to short-term corrections.

Final Take on NESR Stock

Even after its massive rally, NESR’s investment case remains compelling. The company combines strong price momentum with industry-leading earnings growth, discounted valuation, and deep exposure to one of the most active energy regions globally. While risks tied to geopolitics and execution persist, the long-term growth trajectory appears intact. With solid fundamentals and continued tailwinds from Middle East activity, NESR stock still looks attractive. Importantly, it currently holds a Zacks Rank #1 (Strong Buy), reinforcing confidence in its prospects.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

SLB Limited (SLB): Free Stock Analysis Report

National Energy Services Reunited (NESR): Free Stock Analysis Report

Weatherford International PLC (WFRD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).