nLIGHT LASR and Lumentum Holdings LITE are both well-known players in the fiber laser and photonics industry. nLIGHT is a leading supplier in providing high-power lasers for mission-critical defense systems and advanced manufacturing, while Lumentum is a larger, established leader with a wide portfolio of lasers used in industrial, medical and advanced technology applications.

Both LASR and LITE support modern manufacturing by providing the laser and photonics technologies needed to work with metals, electronics and advanced materials. However, from an investment point of view, one stock offers a more favorable outlook than the other right now. Let’s break down their fundamentals, growth prospects, market challenges and valuation to determine which stock offers a more compelling investment case.

The Case for nLIGHT Stock

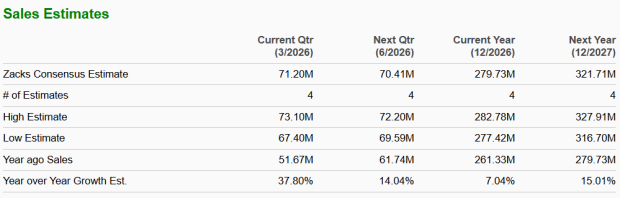

nLIGHT’s directed energy end market is becoming one of the key growth drivers. The directed energy end market was a key reason behind the strong performance of its Aerospace and Defense (A&D) business in 2025. A&D revenues rose 60% year over year to a record $175 million, and management said directed energy was one of the main contributors. The company believes it is well-positioned in this market because it offers products across the full stack, from laser chips and components to high-energy laser systems and full laser weapon modules.

Management also highlighted solid execution on major directed energy programs. nLIGHT continues to make progress on HELSI-2, a $171 million program to develop a 1-megawatt high-energy laser. Here, shipments tied to HELSI-2 were a significant driver of defense product revenues in 2025 and are expected to remain a substantial contributor in 2026. In the fourth quarter, nLIGHT also substantially completed its work on the Army’s DE M-SHORAD program and delivered a 50-kilowatt CBC high-energy laser and beam director to its partner for integration and test.

However, a key risk that weighs on nLIGHT’s prospects is the company’s decision to exit the cutting and welding business, which will create a clear revenue headwind in 2026. Management said this move is expected to reduce full-year revenues by around $25 million to $30 million. The company has already informed customers and is now working through last-time buys and other wind-down actions. Some revenues from this business will continue in the first half of 2026, but management said it should be close to zero by the second half of the year.

This exit is part of a broader effort to improve focus and move resources toward better opportunities such as directed energy, laser sensing and additive manufacturing. Strategically, that makes sense because cutting and welding have been facing weak demand and are no longer as attractive as the company’s core growth areas. However, even if the decision is right from a long-term perspective, it still creates a short-term gap in the company’s revenue base.

The Zacks Consensus Estimate for 2026 and 2027 revenues indicates a year-over-year increase of 7% and 15%, respectively.

Image Source: Zacks Investment Research

The Case for Lumentum Stock

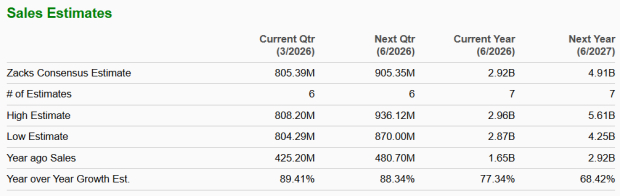

Lumentum reported second-quarter fiscal 2026 revenues of $665.5 million, up 65% year over year. Management stated that the company is now a key supplier to AI networks through both hyperscaler customers and network equipment providers. The company expects further growth, guiding third-quarter revenues to a midpoint of $805 million, which implies a year-over-year increase of more than 85%.

Cloud transceivers were a major contributor in the second quarter. Transceiver revenues increased significantly and are expected to grow again in the next quarter. The company has improved execution in this business, including faster design cycles and better manufacturing performance. Management stated that it is now in the “lead pack” of suppliers as customers move to 1.6T networks, with demand stronger than expected.

Laser chips were another key driver. The company reported record shipments of electro-absorption modulated lasers, supported by demand for 100G and 200G technologies. Here, 200G products are ramping earlier than expected and are expected to increase to about 25% of the mix by the end of 2026. These products contribute more to revenues due to higher pricing.

The components segment grew 68% year over year, driven by demand across cloud and data center applications. At the same time, management said demand continues to exceed supply. The company indicated it is under-shipping customer demand despite adding capacity and expects supply to remain tight. The company is expanding capacity to support this demand, where further upside now depends on additional output.

The Zacks Consensus Estimate for fiscal 2026 and 2027 revenues indicates a year-over-year increase of 77.3% and 68.4%, respectively.

Image Source: Zacks Investment Research

LASR vs. LITE: Earnings Estimate Trend

The earnings estimate revision trend for the two companies reflects that analysts are turning more bullish toward Lumentum.

The Zacks Consensus Estimate for LASR’s 2026 and 2027 EPS is pegged at 35 cents and 56 cents, respectively. The estimates for 2026 and 2027 have been revised downward by 3 cents and 6 cents, respectively, over the past 30 days.

Image Source: Zacks Investment Research

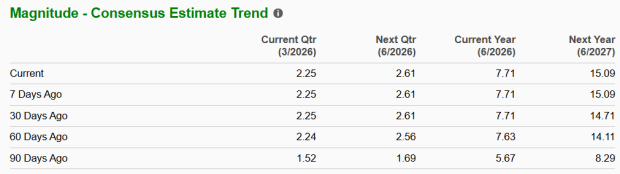

The Zacks Consensus Estimate for Lumentum’s fiscal 2026 and 2027 EPS is pinned at $7.71 and $15.09, respectively. The estimates for fiscal 2026 have been revised up by 8 cents over the past 60 days, while the same for fiscal 2027 have been revised up by 38 cents over the past 30 days.

Image Source: Zacks Investment Research

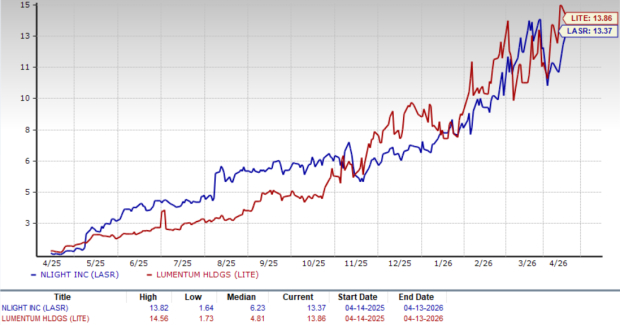

LASR vs. LITE: Price Performance and Valuation

Year to date, shares of nLIGHT and Lumentum have surged 86.1% and 136.9%, respectively.

LASR Vs. LITE: YTD Price Return Performance

Image Source: Zacks Investment Research

Currently, nLIGHT is trading at a forward sales multiple of 13.37X, lower than Lumentum’s forward sales multiple of 13.86X. Lumentum does seem pricey compared with nLIGHT. However, LITE’s robust financial performance, higher growth projections and upward earnings estimate revisions justify its higher valuations.

LASR vs. LITE: Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

Conclusion: Buy LITE, Sell LASR Right Now

Both nLIGHT and Lumentum are important players in the laser and photonics industry. However, LASR is exiting its cutting and welding business, which will create revenue headwind in 2026. In contrast, Lumentum is already seeing strong results from rising AI and cloud spending, demand for its products remains strong, and earnings estimates are moving higher.

Currently, Lumentum carries a Zacks Rank #2 (Buy), making the stock a better pick over nLIGHT, which has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lumentum Holdings Inc. (LITE): Free Stock Analysis Report

nLight (LASR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).