Valued at $191 billion by market cap, California-based Arista Networks, Inc. (ANET) is a leading cloud networking company that provides high-performance networking solutions for data centers, cloud computing, and enterprise environments. Arista is best known for powering the infrastructure behind hyperscale cloud providers and large-scale AI workloads.

The cloud networking giant is expected to announce its fiscal first-quarter earnings on Sunday, May 5, after the market closes. Ahead of the event, analysts expect ANET to report a profit of $0.72 per share on a diluted basis, up 14.3% from $0.63 share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For the current year, analysts expect ANET to report EPS of $3.16, up 16.6% from $2.71 in fiscal 2025. Its EPS is expected to rise 19.9% year over year to $3.79 in fiscal 2026.

www.barchart.com

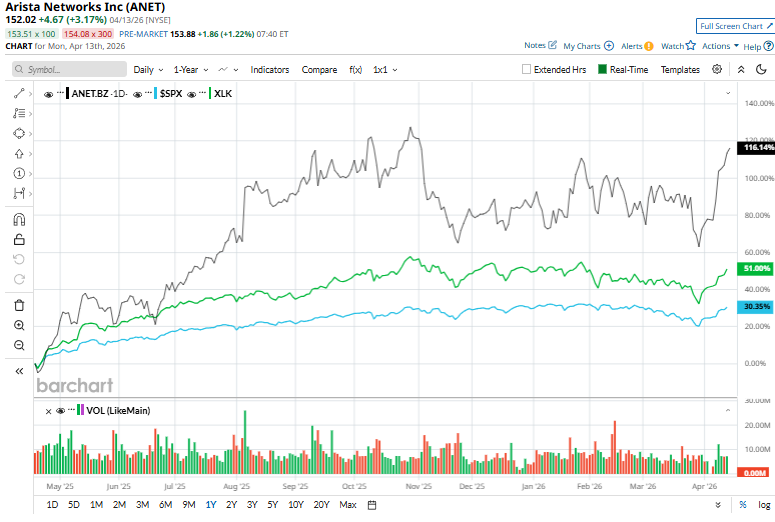

www.barchart.comANET stock has gained 109.2% over the past year, outpacing the S&P 500 Index’s ($SPX) 28.4% gains and the State Street Technology Select Sector SPDR Fund’s (XLK) 46.8% rise over the same time frame.

www.barchart.com

www.barchart.comArista has outperformed the broader market over the past year largely due to surging demand for its high-speed networking solutions, driven by the rapid expansion of AI and cloud data centers. Strong spending from hyperscale customers, combined with consistent revenue growth, high margins, and continued earnings outperformance, has boosted investor confidence.

Analysts’ consensus opinion on ANET stock is bullish, with a “Strong Buy” rating overall. Out of 27 analysts covering the stock, 21 advise a “Strong Buy” rating, two suggest a “Moderate Buy,” and four give a “Hold.” ANET’s average analyst price target is $177.51, indicating a potential upside of 16.8% from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Social Media Stocks Could Be a High-Risk, High-Reward Bet Amid the Iran War Based on This Chart Rubrik Stock Could Be an Iran War Winner, and Analysts Bet It Can Gain 80% from Here Michael Burry Will Be 'Proved Emphatically Wrong' on Palantir, Says Wedbush. Should You Buy PLTR Stock Here? Should You Buy the Dip in Fastenal Stock Today?