Oracle's ORCL decision to deepen its partnership with Bloom Energy is drawing investor attention as the enterprise software giant accelerates its commitment to powering an ambitious AI infrastructure buildout. On April 13, 2026, Oracle announced plans to procure up to 2.8 gigawatts of Bloom Energy's solid oxide fuel cell systems under a master services agreement, with an initial 1.2 gigawatts already contracted and deployment underway through 2027.

The deal followed Oracle's receipt of a $400 million warrant to purchase Bloom Energy stock on April 9, 2026. While the partnership highlights Oracle's differentiated approach to AI infrastructure, investors should weigh both the opportunity and the risks carefully.

Fuel Cells and the Race for AI Power

The Bloom Energy partnership extends beyond a supply agreement, reflecting Oracle's deliberate strategy to bypass the years-long queue for traditional utility grid upgrades. Bloom's solid oxide fuel cell systems provide on-site power generation capable of bringing an entire data center online within 90 days, without requiring grid connectivity. This deployment speed is central to Oracle Cloud Infrastructure (“OCI”), which faces surging demand for AI workloads across its global portfolio. Oracle has committed to bearing energy infrastructure costs independently, funding on-site power generation, dedicated substations and battery storage at its campuses.

The broader buildout is immense. In April 2026, $16 billion in financing was being finalized for an Oracle campus in Michigan, following debt packages of $38 billion for Texas and Wisconsin facilities and $18 billion for a New Mexico site. Oracle also launched a public cloud region in Casablanca, Morocco, in April 2026, extending its global footprint to over 200 planned regions worldwide.

Strong Q3 Metrics, But Execution Risk Looms

Oracle's third-quarter fiscal 2026 results were broadly impressive. Total quarterly revenues rose 22% in dollar terms to $17.2 billion, while cloud revenues surged 44% to $8.9 billion. This marked the first time cloud represented more than 52% of total revenues, surpassing the legacy software segment.

Cloud Infrastructure (IaaS) revenues grew 84% to $4.9 billion, and non-GAAP earnings per share climbed 21% to $1.79, beating guidance. Remaining Performance Obligations ended the quarter at $553 billion, up 325% year over year, providing exceptional revenue visibility. Management noted this was the first quarter in more than 15 years where organic total revenues and non-GAAP earnings per share both grew at 20% or more in dollar terms. Yet legacy software revenues grew only 3%, underscoring that Oracle's growth story is now almost entirely dependent on cloud and AI execution delivering at scale.

Forward Guidance Raises Both Hopes and Stakes

For the fourth quarter of fiscal 2026, Oracle guided for total revenue growth of 19% to 21% in dollar terms and cloud revenue growth of 46% to 50% in dollar terms, representing an acceleration from the fiscal third quarter's already robust cloud performance. Non-GAAP earnings per share guidance for the fiscal fourth quarter stands at $1.96 to $2.

Full-year fiscal 2026 revenue guidance remains unchanged at $67 billion, while Oracle raised its fiscal 2027 revenue forecast to $90 billion — a figure that well exceeded prior Wall Street consensus. Capital expenditure plans for fiscal 2026 total $50 billion, reflecting the unprecedented scale of Oracle's infrastructure ambitions. These forward-looking figures paint a compelling growth narrative, though their realization hinges entirely on Oracle's ability to deploy AI infrastructure at the pace demand requires.

The Zacks Consensus Estimate for ORCL's fiscal 2026 earnings is pegged at $7.45 per share, indicating 23.55% growth year over year.

Oracle Corporation Price and Consensus

Oracle Corporation price-consensus-chart | Oracle Corporation Quote

Share Price Movement and Competitive Landscape

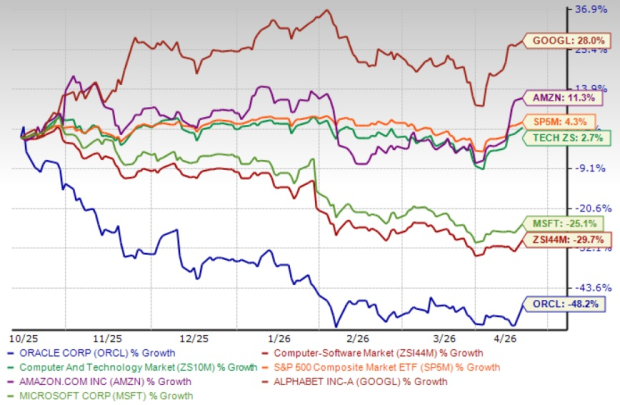

Shares of Oracle have plunged 48.2% over the past six months, underperforming the Zacks Computer and Technology sector and the Zacks Computer - Software industry. In the cloud market, Oracle faces intense competition from Amazon AMZN, Microsoft MSFT and Alphabet GOOGL-owned Google. Amazon's AWS continues to dominate the global infrastructure market share, while Microsoft Azure leverages deep enterprise relationships. Google Cloud pushes AI-native workloads aggressively and is rapidly expanding its own data center footprint. Against Amazon, Microsoft and Google, Oracle differentiates itself through competitively priced GPU compute and strategic multi-cloud database integrations.

ORCL Underperforms Sector, Peers In 6-Months

Image Source: Zacks Investment Research

From a valuation standpoint, ORCL stock is currently trading at a premium with a trailing 12-month price/earnings ratio of 26.24x, which is higher than the industry average of 24.85x. Oracle carries a Value Score of D. This premium valuation reflects investor enthusiasm for the company's cloud transformation and artificial intelligence opportunities, but also introduces meaningful execution risk.

ORCL’s Premium Valuation Builds Concern

Image Source: Zacks Investment Research

A Mixed Picture for Investors

Despite the headline momentum, Oracle's growth story carries meaningful risks. The company has raised more than $100 billion in debt to fund its data center expansion, and $50 billion in capital expenditure commitments in a single fiscal year represent an enormous financial undertaking. The $553 billion RPO does not guarantee timely revenue recognition — converting that backlog requires Oracle to construct gigawatt-scale campuses across multiple U.S. states without significant delays. Supply chain pressures, energy infrastructure dependencies and the complexity of deploying Bloom Energy fuel cells at 2.8 gigawatts introduce real execution uncertainty. Legacy software revenues growing only 3% in the third quarter underscore that Oracle's future is almost entirely tied to cloud and AI delivery. On the positive side, the Bloom Energy partnership enhances Oracle's energy independence and competitive positioning. The company's surging cloud metrics, accelerating IaaS growth and expanding global data center footprint support a credible long-term investment case.

Conclusion

For existing shareholders, these fundamentals justify holding ORCL's shares through near-term volatility; for new investors, elevated execution risk and a heavily leveraged balance sheet suggest waiting for a more favorable entry point in 2026. ORCL stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).