Nebius Group N.V. NBIS is witnessing strong momentum in its business pipeline, reinforcing confidence in its growth outlook for 2026 as demand for AI cloud services continues to accelerate. On the last earnings call, the company reported that its pipeline is expanding significantly, supported by sustained customer interest and increasing adoption across both AI-native companies and enterprise clients. This robust demand environment has led to consistent capacity sellouts, including the latter half of 2025 and into early 2026, highlighting a continued imbalance between supply and demand.

Pipeline expansion is being supported by stronger customer commitments and sustained growth across both new and existing accounts. The company noted a significant increase in contract durations, with new agreements extending by nearly 50% in the fourth quarter of 2025, reflecting a shift toward longer-term engagements. Pricing trends have remained stable across GPU offerings, including older-generation units, supported by consistently high utilization. At the same time, AI-native firms are rapidly scaling their operations, evolving into enterprise-level customers with increasing compute needs, while established enterprises continue to embed AI deeper into their core business processes.

Improving deal dynamics are contributing to the strength of the pipeline. There is also a growing trend of customers securing capacity in advance, including through prepayments, to ensure access amid tight supply conditions. Reflecting this continued momentum, the company indicated that its pipeline creation in early 2026 is on track to surpass $4 billion, supported by steady demand and ongoing sales execution.

Backed by these trends, Nebius reiterated its confidence in its 2026 targets. The company maintained its annualized run-rate revenue (ARR) guidance of $7 billion to $9 billion for the year. The company accelerated its capacity plans, announcing nine new data centers and securing more than 2 gigawatts of contracted power, with expectations to exceed 3 gigawatts. Nebius remains on track to deliver 800 megawatts to 1 gigawatt of available data center capacity by year-end 2026.

With a strong pipeline, expanding capacity and continued demand, Nebius remains well-positioned to deliver on its growth plans. For 2026, the company expects revenue to be between $3 billion and $3.4 billion. The company anticipates the group adjusted EBITDA margin to be approximately 40%.

Taking a Look at NBIS’ Competitors

CoreWeave, Inc. CRWV is positioning itself at the forefront by developing large, purpose-built AI clusters for demanding workloads. Management highlighted four key fundamentals — strong and diversified demand from hyperscalers, AI-native and enterprise customers; new margin-expanding opportunities driven by platform expansion and its NVIDIA (NVDA) partnership; rapid data center expansion supported by strong execution and strategic capacity growth; and a disciplined financial model that invests ahead of revenues to meet contracted demand, backed by a $66.8 billion backlog that provides strong visibility into future cash flows and returns. CoreWeave projects revenues to be between $12 billion and $13 billion for 2026, suggesting 140% year-over-year growth. Management expects every contract tied to new capacity to start generating revenues by the end of 2026.

Microsoft Corporation MSFT capitalizes on AI business momentum and Copilot adoption alongside accelerating Azure cloud infrastructure expansion. Azure’s growth is driven by deep enterprise integration, hybrid cloud strength and rising demand for digital transformation, fueling steady, high-margin recurring revenue. Strong Office 365 Commercial demand has been propelling Productivity and Business Processes revenue growth. ARPU is increasing through E5 and M365 Copilot uptake across key segments. Strategic execution through expanding scale and enterprise customer growth is driving non-AI services. For the third quarter of fiscal 2026, the company expects total company revenues between $80.65 billion and $81.75 billion, suggesting growth of approximately 15% to 17%.

NBIS Price Performance, Valuation and Estimates

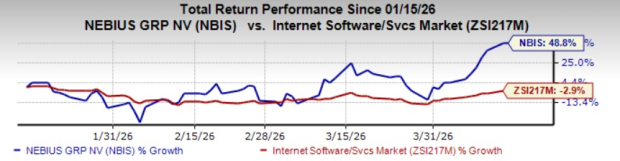

Shares of Nebius have gained 48.8% in the past three months against the Internet – Software and Services industry’s decline of 2.9%.

Image Source: Zacks Investment Research

On a price-to-book basis, NBIS’ shares are trading at 8.44X, above the Internet Software Services industry’s 3.68X.

Image Source: Zacks Investment Research

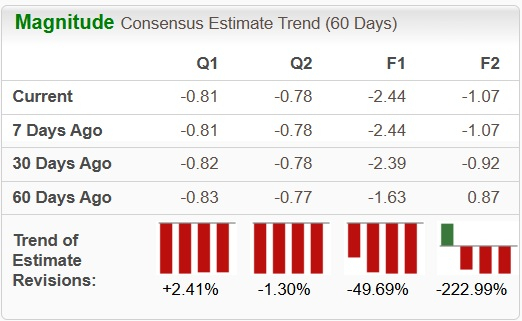

The Zacks Consensus Estimate for NBIS’ earnings for 2026 has been revised downward over the past 60 days.

Image Source: Zacks Investment Research

NBIS currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Nebius Group N.V. (NBIS): Free Stock Analysis Report

CoreWeave Inc. (CRWV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).