Postal Realty Trust PSTL sits in a niche corner of the REIT market, with cash flows tied primarily to U.S. Postal Service-leased properties. Shares were $19.78 as of April 14, 2026, alongside a 6- to 12-month price target of $21.00. The setup points to steady fundamentals, but also clear friction points around per-share growth and a heavier renewal calendar ahead.

PSTL’s Current Setup for a 6- to 12-Month View

The current framework targets modest upside to $21.00 over the next 6 to 12 months, supported by a target multiple of 14.65 times funds from operations (FFO) per share. That stance implies expectations for results that track the broader market, not a call for outsized near-term alpha.

For a new position today, the practical takeaway is that the base case leans toward collecting income and participating in incremental appreciation, rather than betting on a sharp re-rating. The stock’s beta of 0.74 reinforces the lower-volatility profile many investors seek in a defensive REIT allocation.

Postal Realty's Upside Case: Visible Growth Levers

The upside case starts with contractual rent growth and very high occupancy. The portfolio was 99.8% occupied at year-end 2025, and management’s leasing approach emphasizes 10-year terms with 3% annual escalators, which improves revenue visibility over time.

Operationally, the company is guiding same-store cash net operating income growth of 6% to 7% for 2026, a meaningful pace for a net lease-style platform. Management also highlighted that USPS’ last-mile strategy and monetization efforts support demand for the type of facilities PSTL owns, which can help occupancy, pricing power, and lease durations as the 10-year model rolls through the portfolio.

External growth is the other lever. The 2026 acquisition plan calls for $115 million to $125 million of purchases at mid-7% initial cash cap rates. Within management’s return framework, acquiring at roughly a mid-7% initial cash cap rate and layering in around 6% average trailing same-store net operating income growth implies an unlevered internal rate of return in the low double-digit range over time.

PSTL’s Funding Plan and Why It Matters to Returns

Execution depends heavily on funding, and PSTL has been positioning the balance sheet to reduce downside risk while keeping acquisition capacity intact. The 2026 acquisition plan is described as fully funded on a leverage-neutral basis, supported by recent equity and debt activity.

Liquidity expanded meaningfully after $115.0 million of new revolving commitments in February 2026, bringing total liquidity to roughly $270 million to $271 million when including first-quarter capital raised. Management also tightened its leverage target to below 6 times net debt to adjusted EBITDA, with an intent to operate in the low-to-mid 5 times range.

The debt stack is mostly fixed-rate, and the company reported no debt maturities until 2028, which reduces near-term refinancing pressure. In a REIT model where returns can hinge on the spread between acquisition yields and funding costs, these funding conditions matter because they influence how reliably the company can close deals while limiting the risk of a forced slowdown in weaker capital markets.

Postal Realty’s Dilution Reality Check

The key trade-off is that growth has been coming with per-share pressure. 2026 adjusted funds from operations (AFFO) per share guidance of $1.39 to $1.41 explicitly includes approximately 5 cents per share of dilution from outstanding forward equity.

That dilution is not theoretical. In 2025, the company issued 3.15 million shares under its at-the-market program at an average gross sales price of $15.34 per share. After year-end, it entered into forward sales for 1.99 million additional shares that were not yet settled as of Feb. 24, 2026.

The implication is straightforward: even if absolute AFFO and the asset base rise, per-share accretion can lag when equity issuance is a recurring funding tool. The dividend policy also reflects a conservative posture, with a 1% increase in January 2026 to 24.5 cents per share quarterly.

Image Source: Zacks Investment Research

PSTL's 2027 Renewal Wave as the “Big Test”

Lease rollovers are another swing factor. The 2027 renewal cohort totals about 470 leases, including roughly 160 under a master lease that management is working through with USPS. Even with expectations that 2027 renewals will look similar to 2026, the concentration raises the operational intensity required to manage negotiations and documentation at scale.

The risk is not just renewals themselves, but dispersion in outcomes. Timing differences and rent reset variability can widen quarter-to-quarter results when a large cohort is in motion at once.

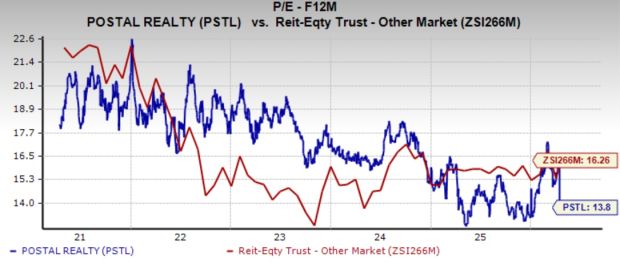

Postal Realty's Valuation vs. Peers and History

On valuation, PSTL trades at 13.80 times forward 12-month FFO per share, below 16.26 times for the Zacks sub-industry and 15.97 times for the Zacks sector. Over the past five years, the stock has traded between 12.82 times and 22.58 times, with a median of 17.56 times, which puts today’s multiple toward the lower end of its own history.

Image Source: Zacks Investment Research

The $21.00 price target is tied directly to maintaining a 14.65 times FFO multiple. That aligns with the broader view that the stock’s risk/reward is balanced at current levels, rather than signaling a clear catalyst for multiple expansion.

Decision Framework Using Zacks Signals

For shorter holding periods, the Zacks Rank is the key signal. PSTL carries a Zacks Rank #3 (Hold), which fits the idea of market-like performance when paired with the company’s steadier, contract-driven cash flows. The Style Scores also suggest PSTL is not screening as a factor standout right now, with a VGM Score of D, Value of C, Growth of D, and Momentum of C. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Investors who want to stay within the broader REIT and Equity Trust - Other group but tilt more toward Zacks Rank strength can also watch names like Gladstone Land LAND and One Liberty Properties OLP, both at Zacks Rank #2 (Buy). Within PSTL specifically, the most balanced approach is to treat the stock as an income-oriented, lower-beta REIT where returns are likely to be shaped by disciplined funding and deal execution, while dilution and the 2027 renewal workload remain the main swing risks.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

One Liberty Properties, Inc. (OLP): Free Stock Analysis Report

Gladstone Land Corporation (LAND): Free Stock Analysis Report

Postal Realty Trust, Inc. (PSTL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).