Lumen Technologies, Inc. LUMN and AT&T Inc. T operate in the telecommunications and fiber network space.

AT&T is one of the largest wireless service providers in North America and one of the world’s leading communications service carriers.

Lumen, on the other hand, is a turnaround story. The company is repositioning itself as “the trusted network for AI.” Management’s strategy is centered on three pillars: building the AI backbone, cloudifying the network and expanding a connected ecosystem of partners.

So, now the question arises: Which stock makes for a better investment pick at present? Let’s dive into the fundamentals, valuations, growth outlook and risks for each company.

LUMN: AI Pivot & Debt Paydown

Proliferation of AI workloads is driving demand for low-latency, high-bandwidth fiber connectivity between data centers, cloud regions and enterprise clients, resulting in increasing demand for Lumen's Private Connectivity Fabric (“PCF”) and network-as-a-service (NaaS) solutions. Driven by significant AI-fueled connectivity demand, Lumen has secured a total of $13 billion in PCF deals at the end of the fourth quarter of 2025.

The company recently partnered with Amazon Web Services (“AWS”) to deliver network connectivity for AWS Interconnect – last mile using Lumen Cloud Interconnect. Enterprises can now deploy private, high-speed AWS connections in minutes (not weeks) through a fully automated, software-driven setup, added Lumen.

Beyond fiber, Lumen is building the NaaS business, with its customer base now exceeding 2000. Management remains upbeat about Internet on Demand, or IoD Offnet, and expects this solution to boost market reach. Lumen remains upbeat about its connected ecosystem strategy (with more than 16 ecosystem partners like Palantir, Commvault and QTS). The connected ecosystem is producing tangible results with more than 180 potential sales opportunities, as highlighted on the most recent earnings call.

The company exceeded its 2025 cost-reduction target, achieving more than $400 million in run-rate savings. It now targets $700 million exiting 2026 and $1 billion by year-end 2027. This cost optimization, combined with improving revenue mix, underpins guidance for adjusted EBITDA of $3.1-$3.3 billion in 2026, with management expecting EBITDA to inflect growth this year.

Perhaps the most important development has been the company’s dedicated deleveraging efforts, including the recent sale of Mass Markets' fiber-to-the-home business (including Quantum Fiber, across 11 states) to AT&T for $5.75 billion in cash. Total debt now reduced to less than $13 billion, down more than $5 billion since January 2025.

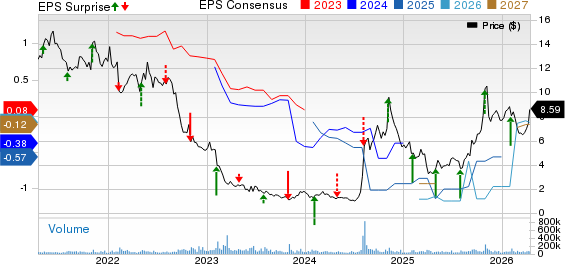

Lumen Technologies, Inc. Price, Consensus and EPS Surprise

Lumen Technologies, Inc. price-consensus-eps-surprise-chart | Lumen Technologies, Inc. Quote

Annual interest expense has been reduced by nearly $500 million, unlocking massive cash flow gains. It also previously eliminated second-lien debt. The sale of the fiber-to-the-home business reduces annual capex by more than $1 billion, allowing Lumen to focus investment on enterprise and AI infrastructure.

While the growth factors appear compelling, risks remain. Lumen must sustain the cost-saving momentum while stabilizing revenues and managing its debt profile. Despite deleveraging, the debt is still hovering at about $13 billion. Legacy headwinds remain a concern, with management expecting Business segment revenues only in 2028, implying at least a couple more years of structural decline.

At its Investor Day, LUMN noted digital capabilities, including NaaS, Edge Solutions, Security and the Connected Ecosystem, to deliver between $500 million and $600 million of incremental revenues exiting 2028 and $800-$900 million by 2030. PCF business will yield $400-$500 million of recurring revenues exiting 2028 and $550-$650 million by 2030.

AT&T: Subscriber Growth & Strong FCF

AT&T continues to witness 5G and fiber subscriber growth. For 2025, the company added over 1.5 million postpaid phone net adds (fifth consecutive year) and more than 1 million fiber net adds for the eighth successive year. AT&T Internet Air saw 875,000 net adds in 2025, more than doubling its customer base at the beginning of the year. This momentum highlights AT&T’s ability to grow its customer base even in a mature telecom market.

AT&T’s fiber expansion is one of the main themes of its growth strategy. The company plans to scale fiber deployment from 3 million new locations in 2025 to a 4 million run rate by 2026. With assets acquired from Lumen and Gigapower, AT&T targets reaching more than 40 million customer locations with its fiber services compared with 32 million at the end of 2025. AT&T expects to add roughly 5 million fiber locations annually through the end of the decade, after 2026.

Strategy of bundling fiber and wireless plans bodes well. The company’s fiber convergence rate increased 200 basis points year over year to 42% for 2025. Management expects this figure to continue rising toward 50% and potentially higher over time.

AT&T remains focused on business transformation efforts to augment operational efficiency and facilitate optimum utilization of resources to enhance value. The company achieved more than $1 billion of cost savings in 2025 and expects to achieve an additional $4 billion annual cost savings by the end of 2028 via operational efficiency, along with reductions in legacy operations and support expenses.

AT&T Inc. Price, Consensus and EPS Surprise

AT&T Inc. price-consensus-eps-surprise-chart | AT&T Inc. Quote

AT&T’s strong free cash flow and growth in adjusted EBITDA are key strengths. The company expects adjusted EBITDA growth in the 3% to 4% range in 2026, while it expects the rate to improve to more than 5% by 2028. Adjusted EBITDA for 2025 was $46.4 billion, up from $44.8 billion in 2024.

The company generated $16.6 billion in free cash flow in 2025 and expects to generate more than $18 billion in 2026. Free cash flow is projected to grow more than $1 billion in 2027 and roughly $2 billion in 2028. This robust cash generation supports a capital return plan of more than $45 billion between 2026 and 2028 through dividends and share repurchases.

While the acquisitions provide long-term growth, they are expected to weigh on near-term financial performance. The company has guided for approximately 5 cents of EPS dilution in 2026 due to stand-up costs and higher interest expenses associated with the Lumen and EchoStar transactions.

AT&T is facing a steady decline in linear TV subscribers and legacy services. Fierce competition in the U.S. wireless market remains a major concern. As the company tries to woo customers with discounts and cash credits, margin pressures might exacerbate. Device offers created a headwind of approximately 90 basis points to 2025 postpaid phone ARPU growth, and similar pressures are expected to continue in 2026.

Price Performance and Valuation for LUMN & T

Over the past month, LUMN stock has gained 26.1% while AT&T has declined 8.6%.

Image Source: Zacks Investment Research

In terms of forward price/sales, LUMN is trading at 0.82X, lower than AT&T’s 1.38X.

Image Source: Zacks Investment Research

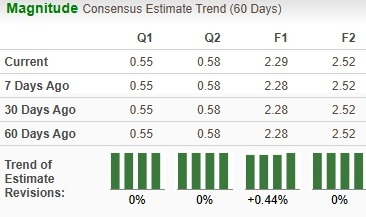

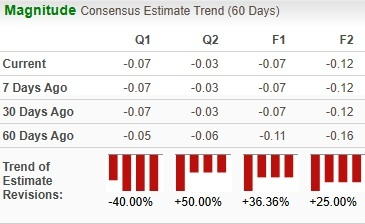

How Do the Zacks Consensus Estimate Compare for LUMN & T?

Analysts have marginally revised their earnings estimates upwards for AT&T for the current year.

Image Source: Zacks Investment Research

Meanwhile, for LUMN, there is a significant improvement in earnings estimates for the current year.

Image Source: Zacks Investment Research

LUMN or AT&T: Which Is a Better Pick?

LUMN currently flaunts a Zacks Rank #1 (Strong Buy) and AT&T carries a Zacks Rank #3 (Hold).

In terms of the Zacks Rank, LUMN appears to be a better pick at the moment.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AT&T Inc. (T): Free Stock Analysis Report

Lumen Technologies, Inc. (LUMN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).