PepsiCo, Inc. PEP has reported solid first-quarter 2026 results, wherein revenues and earnings per share (EPS) beat the Zacks Consensus Estimate and improved year over year. Results reflected an acceleration in reported and organic revenue growth, supported by improving trends in North America and continued resilience across the international business.

PEP’s first-quarter core EPS of $1.61 beat the Zacks Consensus Estimate of $1.55 and improved 8.8% year over year. The increase reflected operating profit growth and a higher core effective tax rate than the year-ago quarter. The company’s core constant-currency EPS increased 5%, pointing to underlying growth despite currency-related translation effects. Reported earnings were $1.70 per share compared with $1.33 in the year-ago quarter. Foreign currency aided EPS by 4%.

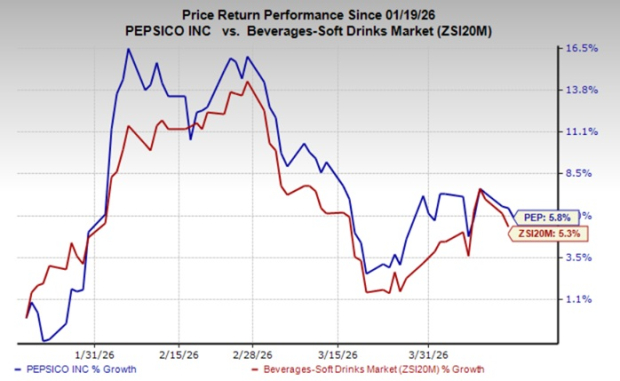

Shares of the Zacks Rank #3 (Hold) company have gained 5.8% in the past three months compared with the industry’s 5.3% growth.

Image Source: Zacks Investment Research

Peek Into PEP’s Q1 Details

The company also delivered net revenues of $19.44 billion, up 8.5% from the year-ago quarter and beating the Zacks Consensus Estimate of $18.95 billion by 2.6%. The increase in net revenues was aided by multiple levers. The unit volume rose 4% for the convenient food business and flat for the beverage business. Foreign exchange translation provided a 3.4-percentage-point benefit, while acquisitions and divestitures added a 2.5-percentage-point net benefit. Organic revenues increased 2.6%, supported by effective net pricing and a slight contribution from organic volume growth.

Our model predicted year-over-year organic revenue growth of 3.6% for the first quarter, with a 3.9% gain from the price/mix and a 0.3% decline in volume.

On a consolidated basis, the reported gross profit rose 7.4% year over year to $10.73 billion. The core gross profit increased 7.3% year over year to $10.72 million. The reported gross margin contracted 60 bps to 55.2%, whereas the core gross margin fell 60 bps year over year to 55.1%.

We anticipated the core gross margin to remain flat year over year at 44.3% in the first quarter. In dollar terms, core gross profit was expected to increase 5.7% year over year.

PepsiCo’s operating profit rose 24% to $3.21 billion in the first quarter of 2026, while core operating profit increased 9% to $3.05 billion. The operating margin expanded significantly to 16.5% from 14.4% in the year-ago quarter on a reported basis. The core operating margin was 15.7%, up 10 bps year over year, as productivity savings and net revenue growth helped offset certain operating cost increases.

Our model predicted core SG&A expenses of $7.57 billion, which indicated year-over-year growth of 5.2%. As a percentage of revenues, core SG&A expenses were anticipated to be 40%, suggesting a 10-bps decline from the prior-year quarter.

We expected a core operating margin of 15.7%, implying a 10-bps increase from the year-ago quarter’s actual.

PepsiCo, Inc. Price, Consensus and EPS Surprise

PepsiCo, Inc. price-consensus-eps-surprise-chart | PepsiCo, Inc. Quote

PEP’s Segment Trends

PEP’s first quarter showed a sequential acceleration in North America, with PepsiCo Foods and PepsiCo Beverages both delivering improved reported net revenue and organic revenue growth. Management noted that affordability initiatives and innovation activity helped drive better performance, including a notable improvement in the convenient foods organic volume.

PepsiCo Foods North America delivered organic revenue growth of 1%, with organic volume up 2%, reflecting a sequential improvement as affordability investments and new product activity reached the marketplace. Management highlighted volume growth across several large snack brands and continued progress in portions of the permissible portfolio.

PepsiCo Beverages North America reported 9% net revenue growth, with organic revenues up 2%. Acquisitions, net of divestitures, contributed meaningfully to reported growth, reflecting distribution and acquisition activity, partially offset by portfolio changes. The organic volume declined 2.5%, including headwinds tied to its case pack water business transition.

International results remained a key support point. The international businesses delivered 5.5% organic revenue growth, marking the 20th consecutive quarter of at least mid-single-digit organic revenue growth, with management citing broad-based momentum and continued share performance in multiple snack and beverage markets. International core operating profit rose 25%, with the core operating margin expanding 145 basis points year over year.

Within the international business, revenues on a reported basis rose 9% in IB Franchise, 18% in EMEA, 16% in LatAm Foods and 11% in Asia Pacific Foods. Organic revenues rose 5% for IB Franchise, 7% each for EMEA and Asia Pacific Foods, and 3% for LatAm Foods.

Financials of PepsiCo Show Stability

PEP ended first-quarter 2026 with improved liquidity, as cash and cash equivalents of $10.48 billion as of March 21, 2026, increased from $9.16 billion at the end of fiscal 2025. Net cash provided by operating activities was $41 billion as of March 21, 2026, compared with net cash used of $973 million in the year-ago period.

PEP’s Outlook for 2026

PepsiCo has reaffirmed its outlook for 2026. The company expects organic revenue growth of 2-4%.

Core constant-currency EPS is anticipated to increase 4-6%, with core EPS growth of 5-7%. Based on the current rates, PEP expects currency translation to provide a tailwind of 1 percentage point on both net revenue and core EPS growth in 2026. Acquisitions completed in 2025, net of divestitures, are expected to add 1 percentage point to reported net revenue growth in 2026. The company expects a core effective tax rate of 22% for 2026.

The company continues to expect capital spending to remain below 5% of net revenues, while targeting a free cash flow conversion ratio of at least 80%.

PEP has been committed to rewarding its shareholders through dividends and share buybacks. It expects to return total cash of $8.9 billion to shareholders in 2026, including $7.9 billion in dividends and $1 billion in share repurchases.

Don’t Miss These Better-Ranked Stocks

Darling Ingredients DAR is a provider of rendering, cooking oil and bakery waste recycling and recovery solutions. The company currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Darling Ingredients’ 2026 sales and earnings implies growth of 6% and 391.2%, respectively, from the previous year’s reported numbers. DAR delivered a trailing four-quarter negative earnings surprise of 41%, on average.

Keurig Dr Pepper Inc. KDP is a prominent integrated brand owner, manufacturer and distributor of beverages across the United States, Canada, Mexico and the Caribbean. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Keurig’s current financial-year sales and earnings indicates growth of 57.1% and 11.2%, respectively, from the prior-year reported levels. KDP delivered a trailing four-quarter earnings surprise of 3.1%, on average.

US Foods Holding Corp. USFD markets, sells and distributes fresh, frozen, and dry food and non-food products to foodservice customers in the United States. It carries a Zacks Rank #2 at present.

The Zacks Consensus Estimate for US Foods’ current fiscal-year sales and earnings implies increases of 5.4% and 20.9%, respectively, from the prior-year reported levels. USFD delivered a trailing four-quarter earnings surprise of 2.2%, on average.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PepsiCo, Inc. (PEP): Free Stock Analysis Report

Darling Ingredients Inc. (DAR): Free Stock Analysis Report

US Foods Holding Corp. (USFD): Free Stock Analysis Report

Keurig Dr Pepper, Inc (KDP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).