However, near-term challenges persist. The industry continues to face tariff-related uncertainty, cost pressures, inflation and ongoing labor constraints. These factors can delay project timelines and compress margins, while also clouding visibility and keeping investor sentiment cautious, especially amid execution risks tied to large and complex infrastructure projects.

Industry Description

The Zacks Building Products - Heavy Construction industry consists of mechanical and electrical construction, industrial and energy infrastructure, as well as building service providers. This industry comprises heavy civil construction companies that specialize in the building and reconstruction of transportation projects, including highways, roads, bridges, airfields, ports and light rail. The companies serve commercial, industrial, utility and institutional clients. The industry players are engaged in the engineering, construction and maintenance of communications infrastructure, oil and natural gas pipelines, as well as processing facilities for energy and utility industries. These firms are also engaged in mining and dredging services in the United States and internationally.

3 Trends Shaping the Future of the Heavy Construction Industry

Data Centers, Grid, and Industrialized Infrastructure: A central structural driver into 2026 is the AI/data-center buildout. The data center boom is fueling growth for U.S. heavy construction firms by driving demand for large-scale site development, power infrastructure, and specialized mechanical systems. These long-term, high-value projects enhance backlog visibility, regional expansion, and margin performance, particularly for companies with technical expertise and national execution capabilities. Overall, the data center boom, fueled by AI and digital infrastructure needs, is reshaping the U.S. heavy construction landscape, favoring firms with technical expertise, national reach, and the ability to execute high-value, mission-critical infrastructure. On the power side, the companies frame the grid as a multi-year CapEx cycle driven by load growth against aging infrastructure, expecting substantial investment across transmission, substations, distribution and new generation capacity. The U.S. administration’s ambitious infrastructure plan, aimed at creating modern, sustainable infrastructure and a cleaner future, is set to have significant implications for the economy and the construction industry over the next five years. By laying the groundwork for sustainable growth, the plan seeks to mitigate the effects of climate change and enhance public health, ensuring access to clean air and water. This expansive infrastructure agenda could be a major boost for companies involved in construction and related sectors.

Solid Inorganic Moves & Renewable Business Prospects: Acquisitions have been companies’ preferred mode of solidifying product portfolios and leveraging new business opportunities. Again, due to increased renewable project activity and the expansion of services in biomass and other smaller production facilities, the power generation and industrial construction market is poised to see sizable growth. The companies are well-positioned to gain from the renewable energy drive of the pro-environmental Biden administration. The development and deployment of technology solutions across the full spectrum of decarbonization efforts, comprising all facets of infrastructure for providing carbon-free energy solutions, should benefit the companies going forward.

Macroeconomic Challenges: The biggest headwinds for the industry players are centered around macroeconomic challenges and labor availability. In addition to a tight labor market, a rise in raw material costs is a concern. Meanwhile, the businesses of the industry players are susceptible to the cyclical nature of the markets in which clients operate and are dependent on the timing and funding of new awards. Hence, volatility in credits and operating risks associated with economic downturns are pressing concerns. Presently, the macro environment is marked by economic and policy uncertainty, including potential shifts in interest rates, inflation and lingering volatility in equity markets—all of which can raise the companies' borrowing costs. The industry players have been specifically citing concerns around evolving tariff and trade policies that could affect materials pricing and project economics. The companies remain sensitive to changes in customer capital expenditure budgets and regulatory frameworks.

Zacks Industry Rank Indicates Bright Prospects

The Zacks Building Products - Heavy Construction industry is an eight-stock group within the broader Zacks Construction sector. The industry currently carries a Zacks Industry Rank #93, which places it in the top 38% of more than 250 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates bullish near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

The industry’s positioning in the top 50% of the Zacks-ranked industries is a result of a higher earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are gradually gaining confidence in this group’s earnings growth potential. Since February 2026, the industry’s earnings estimates for 2026 have increased to $9.49 per share from $9.06.

Before highlighting a few stocks worth considering for your portfolio, let’s first review the industry’s recent stock market performance and valuation trends.

Industry Outperforms Sector & the S&P 500

The Zacks Building Products - Heavy Construction industry has performed better than the broader Zacks Construction sector and the Zacks S&P 500 Composite over the past year.

Stocks in this industry have collectively gained 135.9% compared with the broader sector’s 31.9% rise. Meanwhile, the S&P 500 has jumped 36.2% in the said period.

One-Year Price Performance

Industry's Current Valuation

On the basis of the forward 12-month price-to-earnings ratio, which is a commonly used multiple for valuing heavy construction stocks, the industry is currently trading at 26.7 versus the S&P 500’s 21.75 and the sector’s 20.96.

Over the past five years, the industry has traded as high as 26.70X, as low as 12.90X and at a median of 17.61X, as the chart below shows.

Industry’s P/E Ratio (Forward 12-Month) Versus S&P 500

Industry’s P/E Ratio (Forward 12-Month) Versus Sector

5 Heavy Construction Stocks to Keep an Eye On

Here, we have discussed five stocks from the industry that have solid growth potential.

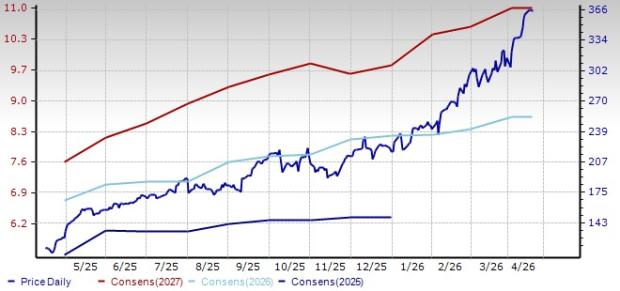

MasTec: Based in Coral Gables, FL, this is a leading infrastructure construction company operating mainly throughout North America. MasTec has strong long-term growth prospects supported by broad-based infrastructure demand across communications, energy and power markets. Accelerating fiber and wireless network investments, driven by broadband expansion, AI-related data center connectivity and middle-mile buildouts, provides sustained tailwinds for its communications business. Power delivery growth is underpinned by rising grid modernization needs, load growth and large-scale transmission, substation and distribution investments. Clean energy demand, including renewable generation and related infrastructure, remains a key multi-year driver. Additionally, improving pipeline infrastructure activity tied to natural gas, LNG exports and gas-fired power generation enhances visibility beyond near-term cycles, reinforcing MasTec’s diversified, multi-year growth runway.

MasTec, currently carrying a Zacks Rank #3 (Hold), has gained 213.7% over the past year. Earnings estimates for 2026 have increased to $8.61 from $8.22 per share over the past 60 days. Earnings for 2026 are expected to grow 31.5% from a year ago. MTZ surpassed earnings estimates in all the trailing four quarters, with the average surprise being 17.4%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Price and Consensus: MTZ

Primoris: A Dallas, TX–based company, Primoris is a provider of infrastructure services operating mainly across the United States and Canada. Primoris has been gaining from robust demand across utilities, energy and renewables, along with a record backlog of nearly $11.9 billion that provides multi-year revenue visibility. The company is benefiting from rising investments in power infrastructure, driven by data center expansion, electrification and grid modernization trends. Growth in renewables, natural gas generation and communications infrastructure, along with increasing Master Service Agreement revenue, enhances stability and predictability. Strategic acquisitions like PayneCrest further expand capabilities in high-growth electrical and data center markets, positioning Primoris for sustained revenue, margin and cash flow growth.

Primoris, currently carrying a Zacks Rank #3, has gained 187.9% over the past year. Earnings estimates for 2026 have increased to $6.02 from $5.78 per share over the past 60 days. Earnings for 2026 are expected to grow 7.1% from a year ago. PRIM surpassed earnings estimates in all the trailing four quarters, with the average surprise being 37.7%. Again, it carries an impressive VGM Score of B.

Price and Consensus: PRIM

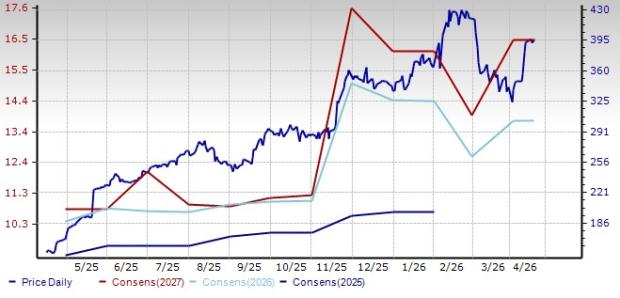

Dycom: Headquartered in Palm Beach Gardens, FL, this is a specialty contracting firm operating in the telecom industry. Dycom has a solid long-term growth outlook, supported by multiple structural demand drivers rather than short-term cycle effects. The company is well-positioned to benefit from accelerating fiber-to-the-home deployments, large-scale data center and AI-driven network builds and rising hyperscaler spending on long-haul and middle-mile connectivity. Federal broadband initiatives, particularly the BEAD program, are expected to unlock multi-year infrastructure spending across rural and underserved regions. Dycom’s expanding service and maintenance portfolio adds recurring, less cyclical revenue visibility. Strategically, the acquisition of Power Solutions broadens its exposure to mission-critical data center electrical work, deepens relationships with hyperscalers and enhances its skilled labor base, strengthening its ability to execute complex, high-value digital infrastructure projects over the next decade.

Dycom, currently carrying a Zacks Rank #3, has gained 155.7% over the past year. Earnings estimates for fiscal 2027 have increased to $13.76 per share from $12.46 per share over the past 60 days. The estimated value for fiscal 2027 is expected to increase 15% from the previous year. DY surpassed earnings estimates in all the trailing four quarters, with the average surprise being 17.1%. Again, it carries an impressive VGM Score of B.

Price and Consensus: DY

EMCOR: Based in Norwalk, CT, EMCOR provides electrical and mechanical construction and related services in the United States and the United Kingdom. EMCOR’s outlook remains strong, supported by robust demand visibility, diversified end markets and consistent execution. The company ended 2025 with record results and a sizable remaining performance obligation of $13.25 billion, providing solid revenue visibility for the next two to three years, particularly in data centers and network communications. Growth is being driven by high-tech manufacturing, healthcare, institutional and water infrastructure projects, along with onshoring trends and energy investments. Continued strength in building services, retrofit demand and aftermarket opportunities adds stability. With a strong balance sheet, active acquisition pipeline and disciplined capital allocation, EMCOR is well-positioned to sustain growth despite macro uncertainties.

EMCOR, currently carrying a Zacks Rank #3, has gained 112.2% over the past year. Earnings estimates for 2026 have increased to $28.23 per share from $27.42 per share over the past 60 days. Earnings for 2026 are expected to grow 9.1% from a year ago. EMCOR surpassed earnings estimates in three of the trailing four quarters and missed on one occasion, with the average surprise being 10.8%. Again, it carries an impressive VGM Score of B.

Price and Consensus: EME

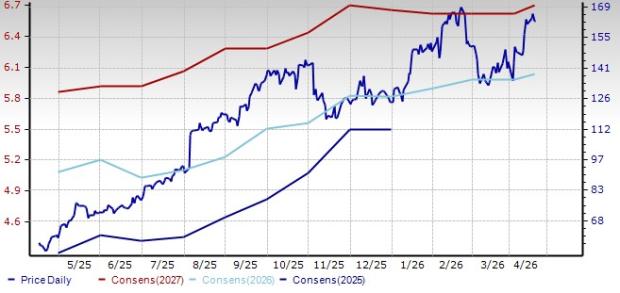

Orion: Based in Houston, TX, this company is a specialty construction firm serving infrastructure, industrial and building markets across North America and the Caribbean. Orion has solid long-term growth prospects driven by rising investment in marine, port and coastal infrastructure, supported by increased federal and defense-related spending. Expansion of U.S. Navy and Indo-Pacific military infrastructure programs, including large multi-award contract vehicles, provides multi-year bidding visibility. Growing demand for dredging, port modernization and marine maintenance supports stable activity across regions. In concrete, accelerating data center construction, reshoring-driven industrial projects and healthcare facilities create sustained private-sector demand. Expanded bonding capacity, disciplined project selection and strategic geographic expansion position Orion to capitalize on these structural tailwinds over the coming years.

Orion, currently carrying a Zacks Rank #3, has gained 95.7% over the past year. Earnings estimates for 2026 have risen to 37 cents from 36 cents per share over the past 60 days. Earnings for 2026 are expected to grow 48% from a year ago. ORN surpassed earnings estimates in all the trailing four quarters, with the average surprise being 248.1%. Again, it carries an impressive VGM Score of B.

Price and Consensus: ORN

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Dycom Industries, Inc. (DY): Free Stock Analysis Report

Orion Group Holdings, Inc. (ORN): Free Stock Analysis Report

Primoris Services Corporation (PRIM): Free Stock Analysis Report

MasTec, Inc. (MTZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).