Nike’s (NKE) stock has been weak lately, but the good news is that CEO Elliott Hill just bought 24,000 shares, along with Apple (AAPL) CEO Tim Cook, who snapped up 25,000 shares, which grabbed investors’ attention. These purchases, worth roughly $1 million each, totaling $2 million in inside activity.

In fact, Nike shares popped 2.81% on Wednesday's regular session, after the company disclosed that Hill and Cook bought stock at roughly $42.27 per share.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

It’s rare for top executives to put fresh cash into beaten-down stocks, and Wall Street took note. But Nike’s business has faced headwinds, and analysts have been cautious. Does Hill’s buy signal a turnaround, or is it just a sign of confidence amid uncertainty?

About Nike Stock

Founded in 1964, Nike is the world’s largest athletic footwear and apparel maker. It designs, markets, and sells sports shoes, clothing, and equipment under the Nike brand and the Converse label. North America is its biggest market accounting for nearly 50% of sales, with the rest split between Europe, China, and other regions. Nike sells products through wholesale partners, its own Nike stores, and online channels.

Nike’s shares have struggled recently. They’re down 27.96% year-to-date (YTD). In early April, the stock hit an 11-year low near $42, and it still trades around $46 now. Investors blame a few factors, such as weak demand in China, higher input costs, tariffs on imports, and slow innovation in key categories.

But Nike is not the only company that is down. Rival Lululemon’s (LULU) stock is also down about 21% YTD, and Adidas (ADDYY) recently warned of a sales slump, as its shares fell after a weak outlook. In short, most athletic apparel stocks have cooled off as consumer spending and supply chain issues are strained.

After the recent correction, Nike doesn’t look outrageously expensive right now. Its trailing price-to-earnings is 30 times, which is actually higher than many high-growth peers. By comparison, some fast-fashion or tech apparel names trade well below 30 times. Also, Nike pays a solid dividend, 3.4% yield, so it returns cash to shareholders even during the downturn.

www.barchart.com

www.barchart.com Nike Turnaround Still in Early Stages

Nike’s latest quarter didn’t bring surprises, but it did reinforce the idea that this is a transition year, not a recovery year.

For the third quarter, revenue came in at $11.3 billion, essentially flat year-over-year (YOY) and down 3% on a currency-neutral basis. Under the surface, the mix tells the real story. Wholesale held up well, rising about 5% to $6.5 billion, while the higher-margin Direct-to-Consumer segment declined roughly 4% to $4.5 billion. China remained soft, and Converse saw a sharp drop tied to inventory clearance.

Margins moved lower. Gross margin slipped to 40.2%, down 130 basis points, reflecting heavier promotions and tariff pressure. That flowed through to earnings, with net income falling 35% to $520 million and adjusted EPS at $0.35. The EPS figure beat lowered expectations, but only because estimates had already reset downward.

Cash generation remained positive, though less robust. Nike ended the quarter with $8.1 billion in cash, down from last year, while continuing shareholder returns through dividends and buybacks.

CEO Elliott Hill struck a cautiously upbeat tone. He said Nike has “taken meaningful actions to improve the health and quality of our business,” and that the company’s “foundation is getting even stronger.” But CFO Matthew Friend warned that these “Win Now” actions, clearing excess inventory, discounting classics, would keep sales flat or down for a while.

Nike gave a forecast that FYQ4 sales would decline by 2%–4%. In fact, company guidance for the June quarter was $10.7–10.9 billion in revenue, versus Wall Street’s $11.3 billion estimate – implying another dip.

Analysts have digested this: consensus estimates now call for fiscal 2026 sales to be roughly flat at mid-$40 billion and EPS around $1.46. For fiscal 2027, analysts expect a recovery with sales rising back toward $50 billion and EPS closer to $2.30.

Nike is not broken, but the turnaround is still in its early innings, and investors should expect a gradual, not immediate, rebound.

Recent News and Developments

Nike hasn’t been idle outside of earnings. The company continues to invest in product and tech. For example, Nike recently unveiled its biggest 2026 FIFA World Cup collaboration lineup ever, teaming with streetwear brands like Palace, Patta, and NOCTA on new soccer-inspired shoes and apparel. This “ambitious” World Cup program is designed to energize fans and boost brand excitement.

On the corporate front, Nike has shuffled its leadership a bit. In April, long-time Innovation Chief Tony Bignell exited, and Nike promoted sportswear design head Andy Caine to replace him. Further, Nike refilled its sustainability chief slot with Cimarron Nix, a 9-year Nike veteran, who was named Chief Sustainability Officer to lead its environmental goals.

What Analysts Are Saying About NIKE Stock?

Wall Street’s take on Nike is mixed. Most analysts have moved to the sidelines, given Nike’s cautious outlook.

Bank of America recently cut Nike to a “Neutral” with an $55 price target. BofA’s Lorraine Hutchinson bluntly noted that management’s guidance implies “sales to remain negative” well into 2026.

JPMorgan’s Matthew Boss likewise warned that Nike’s “international regions…remain challenged globally,” suggesting it will be months before growth resumes.

Even positive firms are cautious. Jefferies still has a “Buy” on Nike but trimmed its target to $90 from $110, citing channel and inventory resets.

On the flip side, some experts still see potential. Jefferies’ Randal Konik pointed out that core categories like running are growing, though he conceded that “sportswear declined” sharply and investors should “reset expectations” for Nike’s recovery.

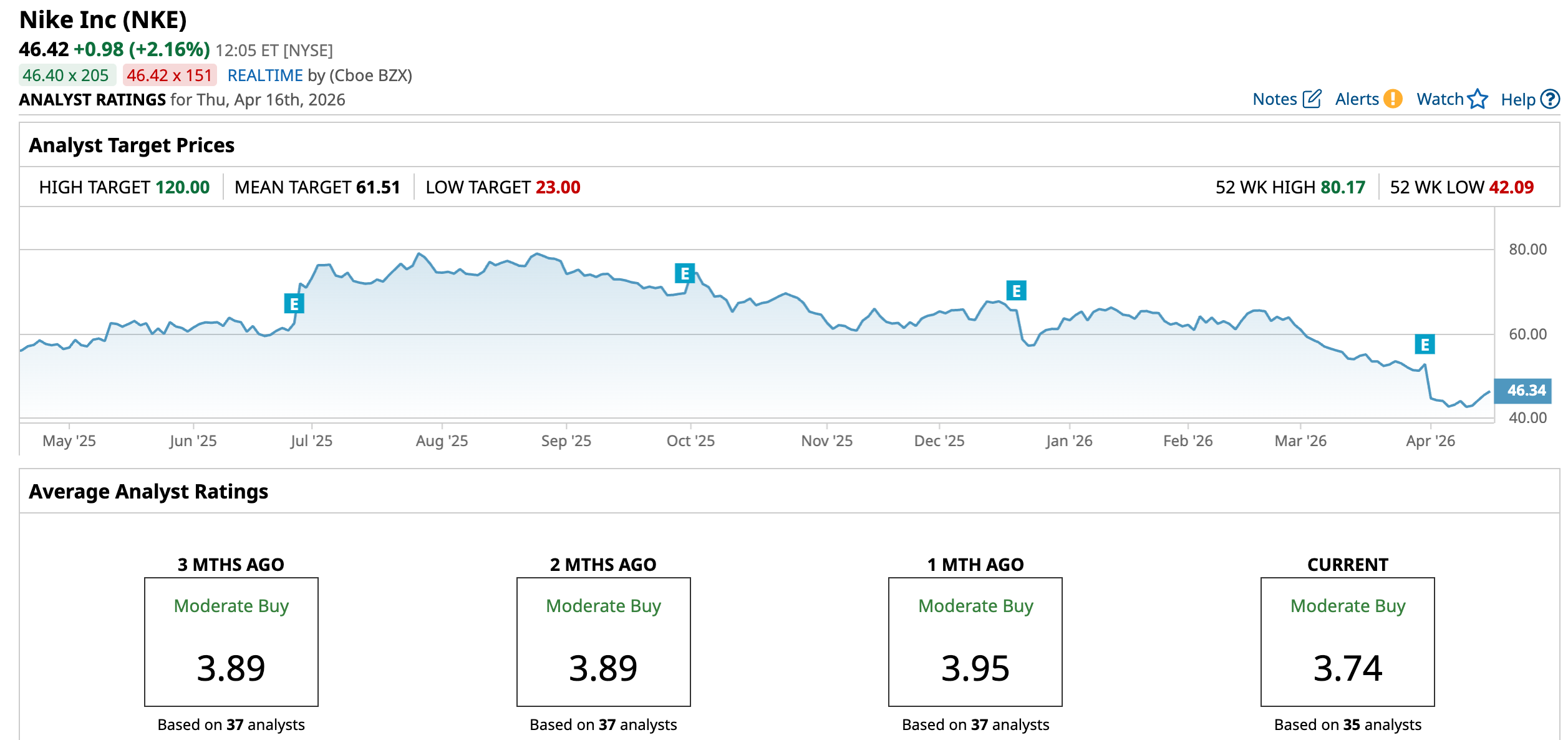

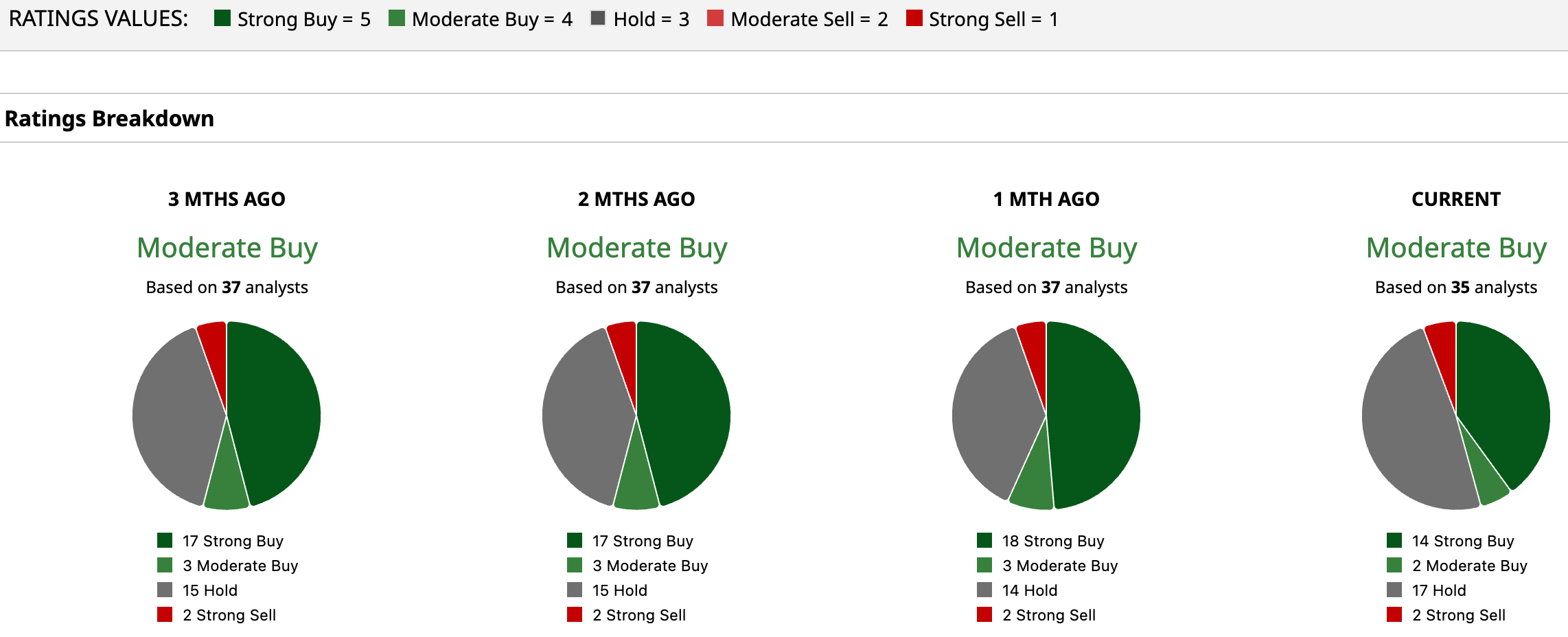

Overall, data aggregator Barchart shows a consensus "Moderate Buy" rating on Nike, with about half the analysts on “Buy” and half on “Hold.” The average 12-month price target is roughly $61.51, about 32.5% above the current price.

In other words, the Street sees some upside if Nike hits its turnaround goals, but most expect several more quarters of tough times.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Up Nearly 60% in 5 Days, Should You Chase the Rally in D-Wave Quantum Stock? CEO Eliott Hill Just Bought 24,000 Shares of Nike Stock. Should You? Analysts Are Divided Over Tesla Ahead of Q1 Earnings, but TSLA Stock Is a Buy Anyway Microsoft Stock Warning: Why Piper Sandler Analysts Just Slashed Their MSFT Price Target by More Than 15%