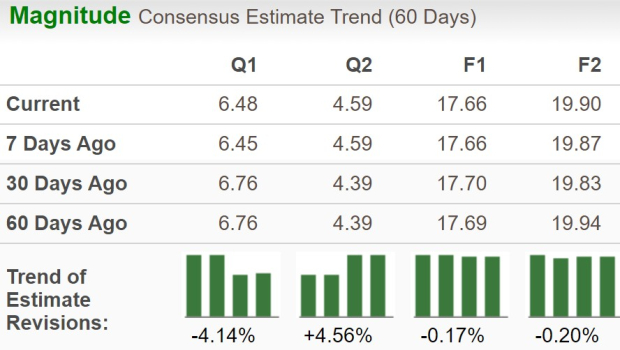

UnitedHealth Group Incorporated UNH is set to report first-quarter 2026 results on April 21, 2026, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $6.48 per share on revenues of $109.45 billion.

First-quarter earnings estimates witnessed one upward revision and no downward movement over the past week. The bottom-line projection indicates a decrease of 10% from the year-ago reported number. Also, the Zacks Consensus Estimate for quarterly revenues suggests a marginal year-over-year decline of 0.1%.

For the current year, the Zacks Consensus Estimate for UnitedHealth’s revenues is pegged at $440.36 billion, implying a fall of 1.6% year over year. However, the consensus mark for current-year earnings per share is pegged at $17.66, implying an improvement of 8% on a year-over-year basis.

UnitedHealth beat the consensus estimate for earnings in two of the last four quarters and missed twice, with the average surprise being negative 2.4%. This is depicted in the figure below.

UnitedHealth Group Incorporated Price and EPS Surprise

UnitedHealth Group Incorporated price-eps-surprise | UnitedHealth Group Incorporated Quote

Q1 Earnings Whispers for UNH

Our proven model predicts a likely earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That is precisely the case here.

UNH currently has an Earnings ESP of +2.77% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

What’s Shaping UNH’s Q1 Results?

The Zacks Consensus Estimate for premium revenues for the first quarter indicates 0.5% year-over-year decline, whereas our model estimate suggests a 0.9% fall. Lower contributions from the UnitedHealthcare division and Optum Health are expected to have caused the decrease.

The Zacks Consensus Estimate for UnitedHealthcare’s total domestic commercial customers suggests a 2.8% year-over-year decline, whereas our estimate implies a 1.1% slip. The consensus mark for Medicare Advantage members indicates an 11% year-over-year decrease. The same for Medicaid memberships implies a 6.4% fall from the year-ago level. These are likely to have pushed total memberships in the domestic market down from the year-ago period. The consensus estimate implies around 4.5% decline year over year.

Rising medical costs, as utilization stays high, are expected to have kept UnitedHealth’s overall expenses elevated in the quarter. The Zacks Consensus Estimate for UNH’s medical care ratio is pegged at 85.7%, up from 84.8% in the year-ago quarter. Moreover, the Zacks Consensus Estimate for operating income from the Optum business segment suggests a 12.9% year-over-year decrease.

The negatives are expected to have been partially offset by a rise in service and products revenues. The consensus estimate implies a 3.1% increase in total service revenues. Similarly, the Zacks Consensus Estimate for product revenues indicates a 3.8% increase. Meanwhile, the Zacks Consensus Estimate for operating income from UnitedHealthcare indicates a 0.4% year-over-year increase, which is likely to have positioned the company for a beat.

UNH’s Price Performance & Valuation

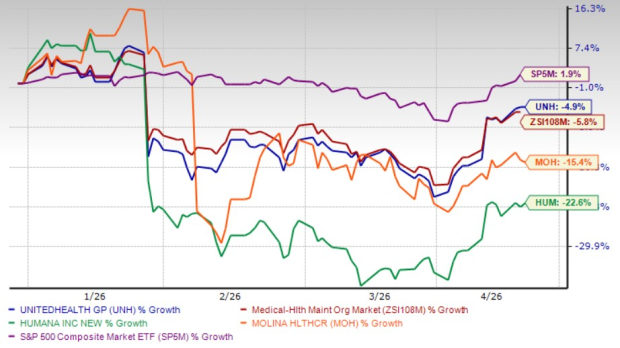

UnitedHealth's stock has lost 4.9% in the year-to-date period, compared with the industry’s fall of 5.8%. Its peers, such as Humana Inc. HUM and Molina Healthcare, Inc. MOH, have lost 22.6% and 15.4%, respectively, during this time. Meanwhile, the S&P 500 has gained 1.9%.

YTD Price Performance – UNH, HUM, MOH, Industry & S&P 500

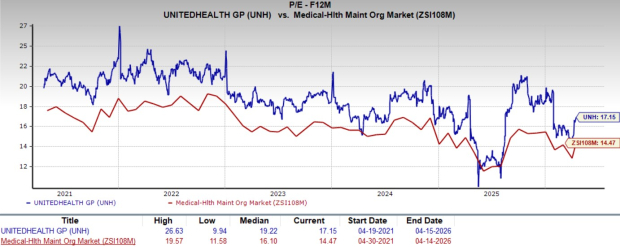

Now, let’s look at the value UnitedHealth offers investors at current levels.

UNH is trading at 17.15X forward 12-month earnings, below its five-year median of 19.22X, but above the industry’s average of 14.47X. In comparison, Humana and Molina Healthcare are currently trading at 18.38X and 24.51X, respectively.

How Should You Play UNH Stock Now?

UnitedHealth heads into its first-quarter 2026 report with expectations set fairly low. The Zacks Consensus Estimate sees earnings and revenues both below last year, as medical costs stay elevated and membership trends down. Still, estimate revisions have turned modestly positive, on growing service and products revenues and stable UnitedHealthcare operating income, which keeps the odds of a beat in play.

The bigger shift is happening outside the quarter. CMS surprised the market by raising 2027 Medicare Advantage rates by 2.48%, easing pressure after a near-flat January proposal. That change matters for UNH given its scale in Medicare, even as the company intentionally trims less profitable plans to protect margins.

With the stock down modestly year to date and still trading below its historical valuation, UNH looks stable, even if near-term pressures haven’t fully eased. The upcoming earnings report will be an important reality check on costs and membership trends. For now, the smarter move may be to stay patient and wait for the results before taking a fresh position.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

UnitedHealth Group Incorporated (UNH): Free Stock Analysis Report

Humana Inc. (HUM): Free Stock Analysis Report

Molina Healthcare, Inc (MOH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).