Lam Research Corporation LRCX is likely to beat earnings estimates when it releases third-quarter fiscal 2026 results on April 22. The company expects revenues of $5.7 billion (+/- $300 million) for the quarter. The Zacks Consensus Estimate is pegged at $5.76 billion, indicating 21.9% growth from the figure reported in the year-ago quarter.

Lam Research expects earnings of $1.35 (+/- 10 cents) per share for the third quarter. The consensus mark for third-quarter earnings has been revised upward by a penny to $1.36 per share over the past seven days, implying a 30.8% year-over-year increase.

Image Source: Zacks Investment Research

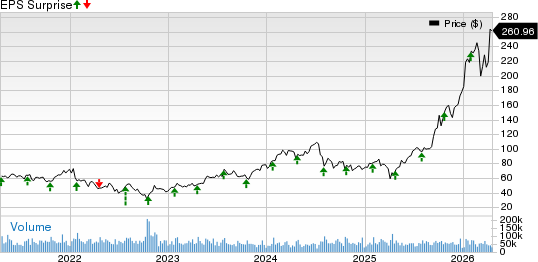

Lam Research has an impressive earnings surprise history. In the last reported quarter, it delivered an earnings surprise of 8.55%. The company’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 6.88%.

Lam Research Corporation Price and EPS Surprise

Lam Research Corporation price-eps-surprise | Lam Research Corporation Quote

Q3 Earnings Whispers for Lam Research

Our proven model predicts an earnings beat for Lam Research this earnings season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat, which is exactly the case here.

Earnings ESP of LRCX: Earnings ESP, which represents the difference between the Most Accurate Estimate ($1.38) and the Zacks Consensus Estimate ($1.36), is +1.58%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Lam Research’s Zacks Rank: LRCX presently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Likely to Influence LRCX’s Q3 Results

Lam Research has been riding on the wave of a strong rebound in the semiconductor industry, driven by the surging demand for memory and advanced AI applications. The rise in spending on artificial intelligence (AI) and machine learning, particularly with the growing influence of Generative AI, is likely to have provided a significant boost to the company's performance in the fiscal third quarter. The increasing need for advanced AI-centric chips has become a key growth catalyst.

Heightened dynamic random access memory (DRAM) spending, especially in response to demand for high-bandwidth memory, is likely to have played in Lam Research's favor. The company's momentum in 3D DRAM and advanced packaging technologies is also expected to have added to its strong performance. At the same time, ongoing technological advancements are pushing NAND spending higher, which is likely to have contributed to LRCX’s quarterly results.

Lam Research’s focus on expanding semiconductor fabrication capabilities, along with its heavy investment in research and development, positions it well in a competitive landscape. Its innovation through Semiverse solutions, particularly in high-aspect-ratio memory hole etch for NAND, is likely to have fueled this progress. LRCX’s strategic investments in cutting-edge technologies are anticipated to have bolstered its performance in the foundry and logic segment, while the increasing adoption of 3D architectures is expected to have supported growth in its etch and deposition services.

The company’s robust suite of tools, which enable foundry logic inflections, is likely to have secured strong customer traction. With the accelerating deployment of 5G and the Internet of Things (IoT), Lam Research’s semiconductor and memory solutions remain in high demand, reinforcing its market position in the fiscal third quarter.

All these factors are likely to have driven growth in system revenues. The Zacks Consensus Estimate for third-quarter systems revenues is pegged at $3.82 billion, implying year-over-year growth of 25.8%, underscoring Lam Research’s continued strength in the evolving tech landscape. The consensus mark for the Customer Support segment’s third-quarter revenues is pegged at $1.94 billion, indicating a year-over-year increase of 15.3%.

LRCX’s Stock Price Performance & Valuation

Lam Research shares have surged 309.3% over the past year, outperforming the Zacks Electronics – Semiconductors industry, which has risen 125.7%. The stock has also surpassed major semiconductor equipment providers, including ASML Holding ASML, KLA Corporation KLAC and Applied Materials AMAT. Shares of ASML Holding, KLA Corporation and Applied Materials have soared 120.4%, 173.5% and 183.7%, respectively.

LRCX One-Year Price Return Performance

Image Source: Zacks Investment Research

Let us look at the value Lam Research offers investors at current levels. Currently, LRCX is trading at a premium, with a forward 12-month P/E of 40.09X compared with the industry’s 31.29X.

Lam Research Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

Compared with semiconductor giants, the stock trades at a higher multiple than Applied Materials, ASML Holding and KLA Corporation. At present, Applied Materials, ASML Holding and KLA Corporation have forward 12-month P/E of 31.32X, 37.64X and 38.40X, respectively.

Investment Thesis on LRCX Stock

Lam Research is capitalizing on AI trends. It builds the tools chipmakers need to manufacture next-generation semiconductors, including high-bandwidth memory (HBM) and chips used in advanced packaging. These technologies are vital for powering AI and cloud data centers.

Lam Research’s products are not only critical but also innovative. For example, its ALTUS ALD tool uses molybdenum to improve speed and efficiency in chip production. Another product, the Aether platform, helps chipmakers achieve higher performance and density. These are essential capabilities as demand for advanced AI chips continues to increase.

In 2025, Lam Research’s revenues from advanced packaging grew significantly, and management anticipates strong 40% year-over-year growth for 2026. The industry’s migration to backside power distribution and dry-resist processing presents growth opportunities for LRCX’s cutting-edge fabrication solutions.

These trends are aiding Lam Research’s financial performance. The company has demonstrated consistent execution, maintaining quarterly revenues of more than $5 billion for the past three consecutive quarters, reflecting solid demand from leading chipmakers such as Taiwan Semiconductor Manufacturing and Samsung.

Conclusion: Hold LRCX Stock for Now

Lam Research’s strong technological foundation and strategic focus on high-growth markets like AI and HPC make it a compelling long-term investment. The company’s innovation and operational efficiency provide a solid foundation for future growth.

However, its lofty valuation and ongoing macroeconomic uncertainties call for a more cautious stance. Considering these factors, holding LRCX stock appears to be the most prudent strategy for investors.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

KLA Corporation (KLAC): Free Stock Analysis Report

ASML Holding N.V. (ASML): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).