Petrobras PBR and Chevron Corporation CVX are among the world’s leading integrated energy players, with operations spanning upstream, downstream and emerging low-carbon initiatives. While both benefit from resilient global oil demand, their strategic focus, cost structures and risk exposures differ meaningfully.

Petrobras is increasingly positioned as a high-growth offshore producer, leveraging its world-class Brazilian pre-salt assets. Chevron, on the other hand, is taking a more balanced route, focusing on steady returns, disciplined spending and diversification. With oil markets still unpredictable due to macro and geopolitical factors, it’s worth looking at which of these two might offer better potential right now.

The Case for Petrobras

Petrobras continues to stand out as a growth-driven energy player backed by strong execution and high-margin assets. The company delivered solid production performance in 2025, with output reaching 2,990 thousand barrels of oil equivalent per day (MBOE/D), up 11% year over year and ahead of guidance. This growth was primarily driven by its pre-salt portfolio, including highly productive fields like Búzios. Its reserves are another major strength. Petrobras added 1.7 billion barrels of oil equivalent in proved reserves, translating to a reserve replacement of 175% and extending reserve life to 12.5 years. This enhances long-term production visibility.

Even with softer oil prices, the company generated around $36 billion in operating cash flow, highlighting how cost-efficient its offshore operations are. Petrobras’ dividend policy — returning 45% of free cash flow — also makes it attractive for income-focused investors.

Additionally, ongoing efficiency gains contributed nearly 100,000 barrels per day of incremental production without significant capital deployment. Overall, Petrobras’ strong production growth, robust reserves, disciplined capital allocation and consistent cash generation reinforce its position as a compelling long-term energy investment.

The Case for Chevron

Chevron offers a more balanced and stable investment profile, supported by a diversified asset base and disciplined capital allocation. The company delivered solid production in 2025, reaching approximately 3,723 MBOE/D, driven by high-return assets in the Permian Basin and Kazakhstan’s Tengiz expansion. Looking ahead, Chevron expects production to grow further, with 2026 guidance of 3,980-4,100 MBOE/D.

One unique advantage is its presence in Venezuela, where Chevron operates under special authorization. Through partnerships with PDVSA, Chevron plays a meaningful role in the country’s oil production and is working to expand further. This could become a meaningful growth driver in the coming years. Recent developments suggest the company is increasing its stake in key projects and could boost output materially over the next couple of years.

Financially, Chevron remains robust, generating strong cash flow and maintaining one of the healthiest balance sheets among oil majors. Its integrated model — spanning upstream, refining and chemicals — helps cushion earnings during commodity price swings. Chevron’s shareholder return strategy is another key strength. The company continues to prioritize dividends and buybacks, supported by steady free cash flow generation and long-term cost discipline.

In addition, ongoing cost discipline and capital efficiency initiatives have strengthened margins, allowing Chevron to remain competitive even in lower oil price environments.

Price Performance

Over the past six months, Petrobras has significantly outperformed, with its stock rising more than 85.5%, compared with Chevron’s 23.9%.

Image Source: Zacks Investment Research

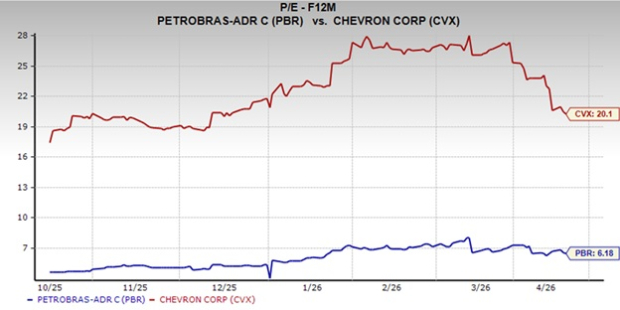

Valuation

In terms of valuation, Petrobras is considered undervalued with a much lower forward P/E of about 6.18. This suggests that the market sees it as relatively cheap, possibly due to Petrobras’ higher risks despite a stronger growth outlook. On the other hand, Chevron is overvalued in comparison, trading at a higher P/E multiple. This suggests investors are willing to pay more for Chevron's stock, likely due to its lower perceived risk and more stable growth.

Image Source: Zacks Investment Research

Earnings Estimate Revisions: Rising Optimism for Both Stocks

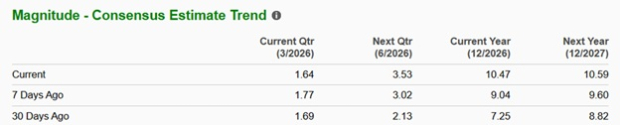

Rising geopolitical tensions, particularly around the Middle East and key shipping routes like the Strait of Hormuz, have added a risk premium to oil prices. Over the past 30 days, the Zacks Consensus Estimate for Petrobras’ 2026 and 2027 earnings has moved higher, reflecting improving sentiment.

Image Source: Zacks Investment Research

Chevron has also seen upward revisions in earnings estimates for both years, supported by strong operational momentum and stable cash flow expectations.

Image Source: Zacks Investment Research

Final Verdict: Growth vs. Stability – Which Stock Has the Edge?

Both companies have their strengths, but they cater to slightly different types of investors. Petrobras is the more aggressive growth play, backed by rising production, strong reserves and solid cash flow. It is better suited for those looking for higher upside. Chevron, meanwhile, offers stability. Its diversified operations, strong financials and consistent shareholder returns make Chevron a safer, more predictable choice. Right now, Petrobras seems to have the edge in terms of growth potential. But Chevron remains a reliable option if you prefer steady performance over higher risk. CVX and PBR currently sport a Zacks Rank #1 (Strong Buy) each.

You can see the complete list of today’s Zacks #1 Rank stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chevron Corporation (CVX): Free Stock Analysis Report

Petroleo Brasileiro S.A.- Petrobras (PBR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).