The Procter & Gamble Company PG, also known as P&G, is set to report third-quarter fiscal 2026 results on April 24, before the opening bell. The company is expected to have witnessed year-over-year sales and earnings growth in the to-be-reported quarter.

The Zacks Consensus Estimate for fiscal third-quarter revenues is pegged at $20.6 billion, indicating a 4.2% rise from the prior-year quarter’s reported figure. The consensus mark for PG’s earnings is pegged at $1.57 per share, indicating growth of 2% from the year-ago quarter’s actual. The consensus mark for earnings has been unchanged in the past 30 days.

PG has a trailing four-quarter earnings surprise of 2.2%, on average. The company delivered an earnings surprise of 0.5% in the second quarter of fiscal 2026.

PG’s Earnings Whispers

Our proven model does not conclusively predict an earnings beat for Procter & Gamble this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Procter & Gamble has an Earnings ESP of -1.17% and a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Key Trends to Watch Ahead of PG's Q3 Earnings

PG’s resilient performance underscores the power of its brand portfolio and disciplined operating strategy. Despite a mixed consumer backdrop, the company continues to generate steady organic sales, supported by pricing strength and broad-based category growth. Procter & Gamble continues to leverage its strong portfolio of daily-use products, wherein performance directly drives consumer brand choice, to deliver steady organic growth.

Our model predicts year-over-year organic sales growth of 2.4% for PG in the third quarter of fiscal 2026. Our model estimates organic sales growth of 2% each for the Beauty, Health Care and Fabric & Home Care segments, 5% for the Grooming segment, and 3% for the Baby, Feminine & Family Care segment.

The company’s integrated strategy, built on innovation, market expansion and productivity, has enabled it to adapt to shifting consumer dynamics and maintain competitiveness.

Innovation execution is a key swing factor. The company is rolling out major product upgrades and new formats across core franchises, with management repeatedly emphasizing that sustainable growth will come from superior performance rather than price-led tactics. The company’s focus on core categories and innovation continues to fuel performance, likely aiding organic sales in the fiscal third quarter.

Procter & Gamble Company (The) Price and EPS Surprise

Procter & Gamble Company (The) price-eps-surprise | Procter & Gamble Company (The) Quote

Investors should watch progress on restructuring and productivity initiatives. PG has actively been streamlining its portfolio, supply chain and organizational structure to fund reinvestment in brands while improving agility. Evidence that these actions are translating into better execution, cost discipline and reinvestment capacity will be important, especially as the company navigates tariff and cost-related uncertainty.

However, Procter & Gamble’s third-quarter fiscal 2026 results are expected to reflect the mounting pressures from elevated commodity costs, rising tariffs and higher financing expenses, which are expected to have weighed on its margin performance. The gross margin has been contracting despite productivity gains, while tariff headwinds and higher interest and taxes threaten earnings growth.

On the last reported quarter’s earnings call, management acknowledged ongoing pressure from raw materials, packaging, transportation and other supply-chain-related expenses, which have been weighing on the cost of goods sold and limited margin expansion. We expect the core cost of products sold to increase 3.6% year over year in third-quarter fiscal 2026. Our model predicts the core gross margin to contract 10 bps year over year to 50.9%.

Management also highlighted that trade-related costs are creating incremental pressure on sourcing, manufacturing and cross-border supply chains. Given PG’s global footprint, tariffs can disrupt cost structures across multiple categories and geographies, limiting the company’s ability to fully offset impacts through productivity alone. While selective pricing actions and supply-chain adjustments provide partial mitigation, tariffs remain largely outside management’s control and can compress margins if sustained.

Procter & Gamble’s Price Performance & Valuation

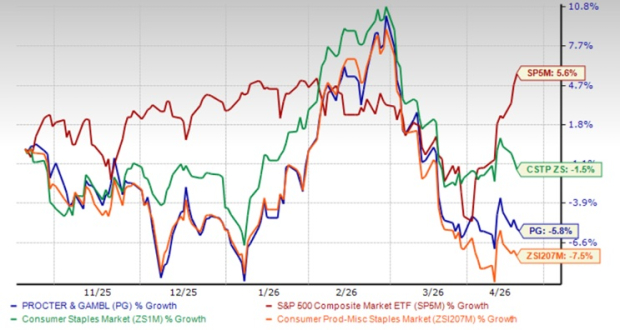

PG shares have declined 5.8% in the past six months compared with the industry’s drop of 7.5%. The stock has lagged the Zacks Consumer Staples sector’s fall of 1.5% and the S&P 500’s 5.6% growth.

PG’s 6-Month Performance

Image Source: Zacks Investment Research

The Procter & Gamble stock has outperformed The Clorox Company’s CLX decline of 14.4% in the past six months. However, the PG stock has underperformed its peers, Colgate-Palmolive Company CL and Church & Dwight Co., Inc. CHD, which have rallied 6.2% and 7.4%, respectively, in the past six months.

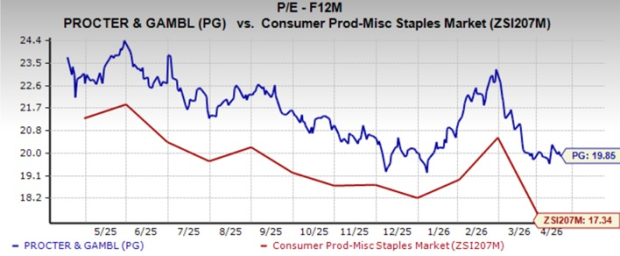

From the valuation standpoint, Procter & Gamble is trading at a forward 12-month P/E multiple of 19.85X, exceeding the industry’s average of 17.34X but below the S&P 500’s average of 21.91X. PG’s valuation appears pricey relative to the industry.

Image Source: Zacks Investment Research

Given the premium valuation, investors may face significant risks if the company's future performance does not meet expectations. The consumer goods market is becoming increasingly competitive, and Procter & Gamble’s innovation and market expansion may not suffice to drive significant growth. Macroeconomic challenges and heightened competition may impede the company's ability to sustain its current growth trajectory.

Investment Thesis

Procter & Gamble’s investment appeal rests on the durability of its brand portfolio, disciplined execution and a strategy designed to perform through volatile consumer and macro conditions. Management emphasized consistent organic growth, driven by broad-based demand, strong brand equity and a steady cadence of innovation across core daily-use categories. The company’s integrated superiority model, linking product innovation, brand communication, retail execution, productivity and portfolio focus, is helping PG defend value positioning in developed markets while accelerating momentum in faster-growing regions, such as China and Latin America.

While near-term pressures from competitive intensity, tariffs and input costs persist, PG is proactively addressing these through restructuring, supply-chain modernization and targeted portfolio exits to improve agility and returns. Strong cash generation continues to support shareholder returns and reinvestment in innovation, reinforcing PG’s profile as a resilient consumer staples leader with the ability to compound value across cycles.

Conclusion

Procter & Gamble offers a balanced near-term risk-reward profile heading into fiscal third-quarter results. Its defensive model, strong brands and resilient organic growth provide stability in a challenging macro environment. However, commodity inflation, tariff pressures and intense competition may continue to weigh on margins and limit near-term earnings upside.

With the stock trading at a premium and earnings estimates edging down, caution seems appropriate. Existing investors may choose to hold for PG’s long-term strength, while monitoring execution on pricing, innovation and productivity. New investors may prefer to wait for clearer margin recovery or a more attractive valuation before taking positions.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Procter & Gamble Company (The) (PG): Free Stock Analysis Report

Colgate-Palmolive Company (CL): Free Stock Analysis Report

The Clorox Company (CLX): Free Stock Analysis Report

Church & Dwight Co., Inc. (CHD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).