ServiceNow (NOW) stock crashed on Thursday after the software giant posted its Q1 earnings that failed to provide the reassurances investors so desperately needed amid artificial intelligence (AI) disruption fears.

While revenue of $3.77 billion topped Street estimates, a disappointing subscription gross margin outlook and a slowdown in contract obligations triggered a sharp selloff.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The post-earnings weakness pushed NOW decisively below its 20-day moving average (MA), a technical breakdown that signals bearish momentum may sustain in the near term.

Versus its year-to-date high, ServiceNow stock is now down nearly 45%.

www.barchart.com

www.barchart.comIs It Worth Investing in ServiceNow Stock Today?

Investors are advised to keep on the sidelines in NOW shares primarily because the firm’s Q1 release demonstrated cracks in its growth engine.

Subscription revenue growth, while technically up 19% in constant currency, showed clear signs of deceleration compared to previous years, bringing into question the efficacy of its Now Assist AI platform that management has marketed heavily as a growth re-accelerator.

More concerning was the company’s lowered gross margin forecast for 2026, now pegged at 81.5% against the 82.1% analysts expected.

Management attributed this to the integration of recent large-scale acquisitions like Armis, but for investors, it signals the organic growth premium ServiceNow Inc once enjoyed is being diluted by expensive M&A.

This means that the Nasdaq-listed firm must now spend more aggressively to maintain its market position, squeezing profitability in the process.

NOW Shares Remain Expensive Despite AI Disruption Risks

Caution is warranted in buying the dip in ServiceNow shares also because they’re still trading at a premium 40x forward earnings multiple, leaving little room for error as the federal procurement environment weakens.

Recent analyst notes from Stifel and Macquarie have highlighted a 72% year-over-year contraction in federal obligations, which is a massive headwind for the firm’s cRPO.

Plus, the rise of AI-native competitors is beginning to challenge NOW’s core workflow dominance, with UBS analyst Karl Keirstead recently conceding that AI is proving a bigger threat for it than anticipated.

Meanwhile, despite a massive year-to-date decline, ServiceNow’s relative strength index (14-day) still sits in the mid-30s currently, indicating further downside room before the stock hits “oversold” territory.

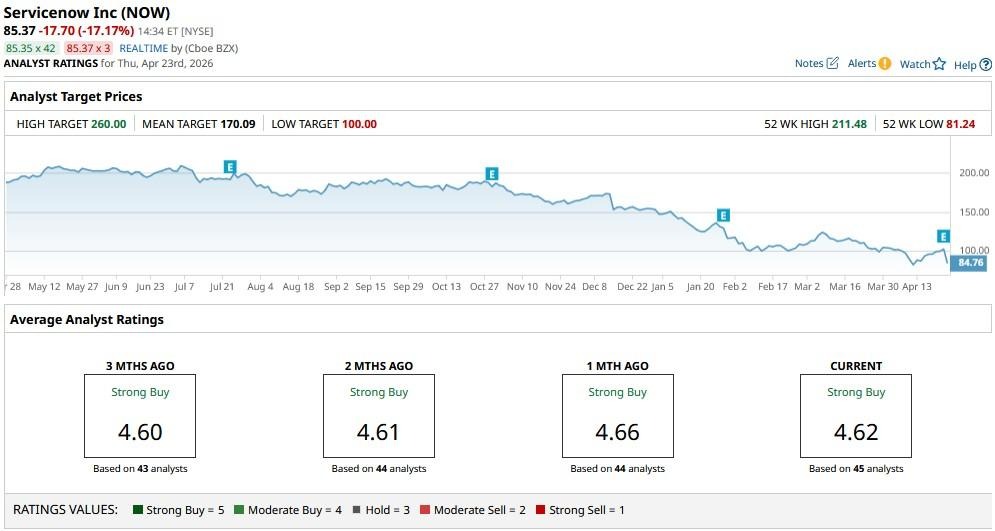

What’s the Consensus Rating on ServiceNow?

Investors should note, however, that Wall Street remains bullish as ever on ServiceNow, despite the aforementioned risks.

The consensus rating on NOW stock remains at “Strong Buy,” with the mean price target of about $170 indicating potential for a 100% rally from here.

www.barchart.com

www.barchart.com On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tesla Beats in Q1—But TSLA Stock’s Bull Case Still Needs Fuel KeyBanc Sees AI Saving the Day for CrowdStrike Stock Despite Broad Wall Street Panic. Who’s Right? Amazon Aims to Take Over the GLP-1 Market Next. Will That Move the Needle for AMZN Stock? Should You Buy the Dip in ServiceNow Stock Today?