lululemon athletica inc.’s LULU international unit remains a key pillar of growth. The company is relying on the international markets to drive growth, as its North American business shows signs of slowing with soft sales trends and higher markdowns. The company has been expanding in regions such as China and other global markets, where demand for premium athletic wear has been strong.

These markets are delivering robust gains, supported by brand strength, localized product offerings and disciplined full-price selling. As the company continues to increase its global footprint through store openings and expansion in new markets, international operations are expected to play a significant role in driving overall revenues.

However, the company’s margin story is complicated, with near-term profitability facing pressure from higher costs, markdown activity and investments in growth actions. lululemon’s fourth-quarter fiscal 2025 earnings per share declined 18.4% year over year, reflecting margin pressure from higher markdowns, tariff-related costs and elevated SG&A expenses. Gross profit declined 8% while the gross margin contracted 550 basis points (bps), primarily affected by a 560-bps decline in the product margin, led by increased markdowns and tariff impacts.

Tariffs had a gross negative impact of 520 bps in the quarter, partly offset by 110 bps from enterprise efficiency initiatives. Notably, markdowns increased 130 bps and fixed-cost deleverage weighed by 30 bps. SG&A expenses of $1.18 billion increased 4% from the year-ago quarter. In Q4, selling, general & administrative (SG&A) expenses, as a percentage of net revenues, of 32.5% rose 100 bps from the prior-year quarter. The increase in the SG&A expense rate was primarily due to adverse foreign exchange, fixed-cost deleverage and continued investments in brand building, partly offset by disciplined cost management initiatives across the enterprise.

That said, lululemon is actively working to mitigate these pressures by emphasizing full-price selling, tightening inventory management, reducing markdowns, leveraging scale efficiencies and diversifying its supply chain. The long-term success of its international expansion strategy will depend on how fast the global markets can scale and contribute more profitably.

LULU’s Competition

NIKE, Inc. NKE has been witnessing tariff-related costs, which have been weighing on its near-term profitability. In the third quarter of fiscal 2026, NIKE reported gross margin contraction of 130 bps, primarily reflecting a 300-bps impact from higher tariffs in North America. Nevertheless, NIKE’s “Win Now” strategy is sharpening execution through a sport-led structure, enhanced innovation and a disciplined marketplace reset. Over time, a cleaner marketplace is expected to reduce reliance on markdowns and support stronger full-price realization. NKE also prioritizes innovation, sharper execution and consumer-centric alignment across brands.

adidas AG ADDYY is navigating tariff risks, currency volatility and ongoing promotional intensity across the global markets. ADDYY is actively expanding its global presence by introducing locally relevant product lines and strengthening its brand equity through strategic collaborations and targeted marketing campaigns. adidas has been diversifying its supply chain and implementing risk-mitigation strategies. As supply-chain efficiencies improve and tariff exposure becomes more stable, these efforts are expected to support a gradual recovery in margins.

LULU’s Price Performance, Valuation and Estimates

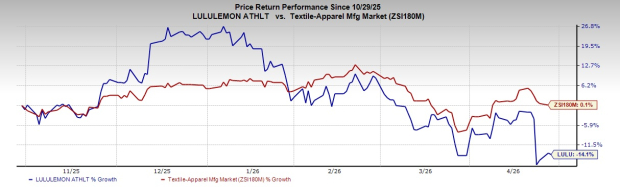

Shares of lululemon have lost 14.1% in the past six months compared with the industry’s rise of 0.1%.

Image Source: Zacks Investment Research

From a valuation standpoint, LULU trades at a forward price-to-earnings ratio of 11.68X compared with the industry’s average of 17.72.

Image Source: Zacks Investment Research

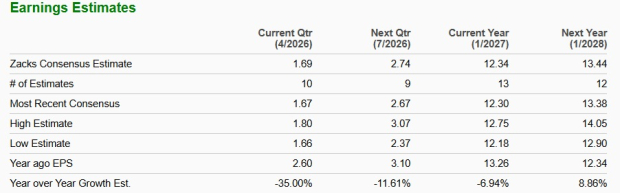

The Zacks Consensus Estimate for LULU’s fiscal 2026 earnings implies a year-over-year drop of 6.9% while that of fiscal 2027 shows growth of 8.9%. The company’s EPS estimate for fiscal 2026 and fiscal 2027 has moved down in the past 30 days.

Image Source: Zacks Investment Research

lululemon stock currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NIKE, Inc. (NKE): Free Stock Analysis Report

lululemon athletica inc. (LULU): Free Stock Analysis Report

Adidas AG (ADDYY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).