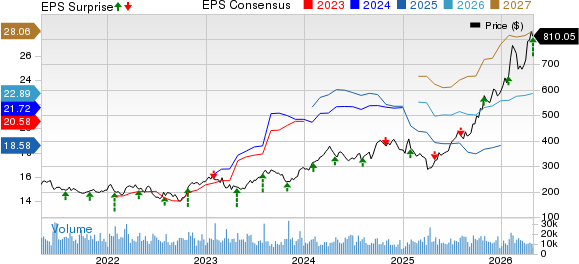

Caterpillar Inc. CAT reported adjusted earnings per share of $5.54 for the first quarter of 2026, which beat the Zacks Consensus Estimate of $4.55 by a margin of 21.8%. The bottom line was 30.4% higher than the year-ago quarter, driven by higher volumes across all segments. These gains were partially offset by elevated tariff-related costs.

Including one-time items, Caterpillar’s earnings per share were $5.47, a 30% increase from the reported figure of $4.20 in the year-ago quarter.

Caterpillar Inc. Price, Consensus and EPS Surprise

Caterpillar Inc. price-consensus-eps-surprise-chart | Caterpillar Inc. Quote

CAT’s Revenue Growth Powered by Volume and Price

Caterpillar’s revenues came in at $17.42 billion, a 22.2% increase from the year-ago quarter and 6% ahead of the consensus mark of $16.44 billion.

The top-line expansion was primarily driven by higher sales volume, which was quantified at $2.3 billion. Favorable price realization added $426 million, while currency also provided a lift and Financial Products revenues contributed incrementally. Our model had projected volume growth of $1.4 billion, an favorable price impact of around $560 million and a positive currency impact of $22.4 million.

Within the volume story, dealer inventory dynamics played a meaningful role. Dealer inventory increase was higher during the first quarter of 2026 than in the prior-year period, alongside higher sales of equipment to end users, supporting broad-based improvement across the company’s three primary operating segments.

Caterpillar witnessed revenue growth in all regions, led by 32% in North America, followed by 20% in EAME, 5% in Latin America and a 4% rise in Asia Pacific.

CAT also exited the period with a record order backlog of $62.7 billion, which marked a $27.7 billion increase from last year, underscoring solid demand as it moves through a tariff-inflated cost environment.

Caterpillar’s Q1 Margins Pressured by Tariffs & Expenses

Cost of sales increased 26% year over year to approximately $11.3 billion, primarily driven by unfavorable manufacturing costs, including the impact of higher tariffs. Gross profit was up 15.6% to $6.1 billion from the prior-year quarter. The gross margin, however, contracted 200 basis points to 35.1% from the year-ago quarter.

Selling, general and administrative (SG&A) expenses moved up 14% year over year to around $1.8 billion and research and development (R&D) expenses were up 12% to $537 million, driven largely by higher compensation expense.

CAT reported an operating profit of $3.085 billion, a 19.6% increase from the year-ago quarter. However, operating margin slipped to 17.7% from 18.1% a year ago, reflecting pressure from manufacturing costs and higher operating expenses.

Adjusted operating profit was around $3.13 billion, up 19.7% from the year-ago quarter. The adjusted operating margin was 18% compared with 18.3% in the first quarter of 2025.

Caterpillar’s Segments Show Mixed Profitability Trends

Total Machinery, Power & Energy (MP&E) sales rose 23% year over year to around $16.47 billion, attributed to higher volumes on increased sales of equipment to end users as well as changes in dealer inventories. Total Machinery, Power & Energy operating profit was around $3 billion, up 19% year over year. Our model’s projection was $2.8 billion.

Construction Industries posted the sharpest sales growth of 38%, with total sales increasing to $7.16 billion on higher sales volume and favorable price realization. The segment’s total sales came in higher than our estimate of $5.69 billion.

The segment’s operating profit was up 50% year over year to $1.53 billion. Our projection was $1.32 billion. Margin expanded to 21.4% from 19.8% in the year-ago quarter, aided by volume growth and pricing strength, with dealer inventory rebuilding a key contributor compared with the year-ago quarter.

Total sales in the Resource Industries segment were up 4% year over year to around $3.8 billion on higher sales volumes and pricing impact. The segment’s first-quarter total sales were higher than our projection of $3.01 billion. The Resource Industries was the outlier on profitability as the segment’s operating profit slumped 39% year over year to around $0.38 billion. Our estimate for the segment’s operating profit was $0.61 billion. Margin compressed to 10.0% from 17% in the first quarter of 2025, as unfavorable manufacturing costs weighed heavily.

Sales of the Power & Energy segment were around $7.03 billion, a 22% increase from last year’s quarter, mainly aided by higher sales volumes. Our estimate was $8 billion. The segment reported sales growth in Power Generation (41%), Oil and Gas sector (13%), followed by Industrial at 5%.

The Power & Energy segment reported a 13% year-over-year increase in operating profit to $1.45 billion, lower than our estimate of $1.7 billion. However. segment margin moderated to 20.6% from 22.3% a year ago, reflecting cost pressure despite healthier demand.

Financial Products’ total revenues rose 9% from the year-ago quarter to $1.096 billion. The segment reported a profit of $245 million, marking a 14% increase year over year. Our model had projected revenues of $1.08 billion and an operating profit of $226.5 million for the first quarter of 2026.

Caterpillar’s Cash Returns Stayed Aggressive in Q1

Caterpillar generated an operating cash flow of around $1.9 billion in the first quarter of 2026 compared with $1.3 billion in the prior-year quarter. CAT ended the quarter with cash and equivalents of around $4.1 billion compared with the cash holding of around $9.98 billion at 2025-end.

The company returned around $5.7 billion in cash to shareholders as dividends and share repurchases through the first quarter.

CAT’s Expectations for Q2 & 2026

Looking to second-quarter 2026, management expects sales and revenues to be higher than the year-ago period. The company flagged tariff costs of around $700 million. However, even including tariffs, CAT anticipates the adjusted operating margin to be higher year over year in the second quarter. For context, the adjusted operating margin was 17.6% in the second quarter of 2025.

For full-year 2026, Caterpillar expects low double-digit sales and revenue growth compared with 2025. The company had earlier expected year-over-year revenue growth near the upper end of its long-term 5-7% CAGR target.

The company now forecasts tariff costs in the range of $2.2-$2.4 billion, lower than the $2.6 billion expected earlier. CAT expects adjusted operating margin to remain near the bottom of its annual target range (including tariffs) while also indicating that margins would be higher than previous expectations.

MP&E capital expenditures are expected to be roughly $3.5 billion for the year.

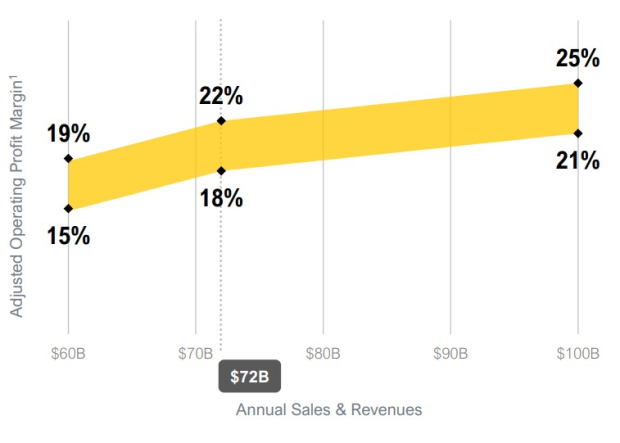

The company maintain its adjusted operating margins of 15–19% at revenue levels of around $60 billion. If revenues reach $72 billion, operating margins are expected to be 18–22%, while revenues of $100 billion could support margins in the range of 21–25%. This is shown in the chart below.

Image Source: Caterpillar Inc.

Caterpillar Stock’s Price Performance & Zacks Rank

Over the past year, Caterpillar stock has gained 161.9% compared with the industry’s 143.6% growth.

Image Source: Zacks Investment Research

Caterpillar carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

How did Caterpillar’s Peer Perform in the Quarter?

Komatsu KMTUY reported earnings per share of 75 cents in the fourth quarter of 2025 (ended March 31, 2026), down 18% year over year. Komatsu’s revenues came in at around $7.76 billion, marking a 3% rise on a year-over-year basis. Komatsu’s Construction, Mining & Utility Equipment sales increased 6.5% in the quarter, while Industrial Machinery & Others sales decreased 1.2%.

Other Manufacturing & Construction Stocks Awaiting Results

Terex Corporation TEX is slated to release first-quarter 2026 results tomorrow. The Zacks Consensus Estimate for Terex’s first-quarter 2026 earnings is pegged at 78 cents per share, suggesting a year-over-year decline of 6%. Terex has a trailing four-quarter average surprise of 23.95%. The consensus estimate for Terex’s revenues for the quarter is $1.7 billion, suggesting 38% growth from the year-ago quarter.

Astec Industries ASTE is expected to release its first-quarter 2026 results on May 6. The Zacks Consensus Estimate for Astec’s earnings is pegged at 88 cents per share, indicating in-line results from the year-ago quarter. The consensus estimate for Astec’s top line is pegged at $394 million, indicating a 19.6% rise from the prior year’s actual. Astec has a trailing four-quarter average surprise of 23.84%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Caterpillar Inc. (CAT): Free Stock Analysis Report

Astec Industries, Inc. (ASTE): Free Stock Analysis Report

Terex Corporation (TEX): Free Stock Analysis Report

Komatsu Ltd. (KMTUY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).