Comfort Systems USA, Inc. FIX is doubling down on growth while raising a key question for investors, that whether its rising capital expenditures translate into sustained returns or not. In the first quarter of 2026, the company significantly ramped up capital expenditure (CapEx) to $147 million, up by a whopping 564.4% from $22 million a year ago, signaling an aggressive push toward expanding its modular construction capabilities.

Management highlighted that spending includes a major modular assembly facility and continued automation upgrades, positioning the company to scale production efficiently. Modular construction, which allows off-site fabrication and faster on-site installation, is increasingly critical for large, complex projects like data centers, a segment driving robust demand. Notably, modular revenues already accounted for 17% of total revenues in the first quarter of 2026, underscoring their growing importance. Comfort Systems reiterated it is on track to reach 4 million square feet of modular capacity by the end of 2026 and said it is actively evaluating additional capacity investments.

The timing of this investment aligns with strong business momentum. FIX reported a 56% year-over-year first-quarter revenue surge and record backlog of $12.45 billion (up from $11.94 billion at year-end 2025 and $6.89 billion a year earlier), reflecting sustained demand, particularly from technology clients. However, elevated CapEx levels, which are expected to remain around 5% of revenues for the full year, raise execution and return-on-investment considerations.

By owning and automating facilities, Comfort Systems aims to enhance productivity, reduce project timelines and capture higher-margin work. If demand remains resilient, especially in data center construction, these modular investments could emerge as a key differentiator. CapEx spike may pressure near-term cash flows, but it positions the company to capitalize on structural shifts in construction.

Comfort Systems vs. EMCOR & Quanta: Modular Edge or Scale Wins?

Comfort Systems shares competitive space with EMCOR Group, Inc. EME and Quanta Services, Inc. PWR in the data center and AI infrastructure demand market.

EMCOR operates a broader and more diversified mechanical and electrical services platform, with strong exposure to both construction and recurring facilities services. While it also benefits from data center demand, its growth tends to be steadier due to its scale and diversified backlog, making it less reliant on any single end market. Conversely, Quanta plays a different role, focusing on power, grid and communications infrastructure, which indirectly benefits from rising data center demand through increased electricity and connectivity requirements. Its exposure is more upstream, tied to long-cycle energy and transmission investments rather than building-level execution.

Overall, FIX offers higher growth tied to modular innovation, EMCOR provides balanced and resilient exposure and Quanta captures structural infrastructure demand, creating distinct competitive positioning across the data center value chain.

FIX Stock’s Price Performance & Valuation Trend

Shares of this Texas-based heating, ventilation, air conditioning and electrical contracting service provider have spiked 97.1% year to date, significantly outperforming the Zacks Building Products - Air Conditioner and Heating industry, the broader Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

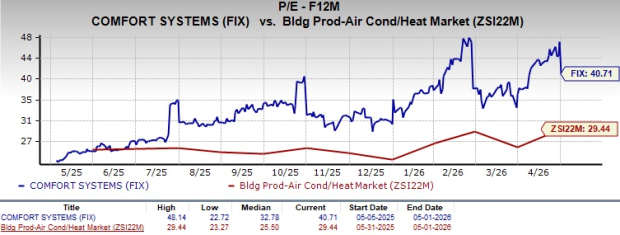

FIX stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 40.71, as the trend lines suggest below.

Image Source: Zacks Investment Research

Earnings Estimate Trend Favors FIX

FIX’s earnings estimates for 2026 and 2027 have moved upward in the past seven days to $43.03 and $51.36 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 49% and 19.4%, respectively.

Image Source: Zacks Investment Research

Comfort Systems currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Comfort Systems USA, Inc. (FIX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).