Medifast, Inc. MED reported first-quarter 2026 results, wherein both the top and bottom lines surpassed the Zacks Consensus Estimate. However, both metrics saw year-over-year declines.

Medifast’s Quarterly Performance: Key Insights

Medifast posted a loss of 19 cents per share, narrower than the Zacks Consensus Estimate of a loss of 55 cents. However, the bottom line deteriorated from a loss of 7 cents per share reported in the year-ago quarter.

MEDIFAST INC Price, Consensus and EPS Surprise

MEDIFAST INC price-consensus-eps-surprise-chart | MEDIFAST INC Quote

Net revenues declined 34.3% year over year to $76 million from $115.7 million, primarily due to a significant reduction in the number of active earning OPTAVIA coaches. Despite the decline, net revenues of this Zacks Rank #3 (Hold) company surpassed the Zacks Consensus Estimate of $73.8 million, reflecting a 3.05% positive surprise.

The company continued to face pressure on its coach network, with active earning coaches declining 44.9% year over year to 14,000 from 25,400 in the same period last year. This drop has been attributed to challenges in client acquisition and the growing popularity of GLP-1 weight-loss medications.

Despite the decline in coach count, productivity improved meaningfully. The average revenue per active earning coach increased 19.2% year over year to $5,432 from $4,556 in the prior-year period.

MED’s Margin & Cost Details

Gross profit declined 38.6% year over year to $51.8 million from $84.2 million in the prior-year period, while gross margin contracted to 68.1% from 72.8% in the prior-year period, mainly due to the deleveraging of fixed costs.

Selling, general and administrative (SG&A) expenses decreased 35.6% year over year to $55.1 million, driven by lower coach compensation, lower volume and fewer active earning coaches with reduced marketing expenses. As a percentage of revenue, SG&A declined 150 basis points to 72.4%, primarily due to lower company-led marketing expenses and a one-time gain from the Maryland Distribution Center sale, partially offset by fixed-cost deleverage from lower sales volume.

The company reported an operating loss of $3.3 million, significantly wider than the loss of $1.3 million in the prior-year quarter.

Medifast’s Financial Health Snapshot

As of March 31, 2026, Medifast maintained a strong balance sheet position with $168.9 million in cash, cash equivalents, and investment securities and no debt.

Sneak Peek Into MED’s Future Outlook

The company expects revenues for the second quarter of 2026 between $60 million and $80 million, with loss per share projected to be between 50 cents and $1.00. Management anticipates continued coach productivity growth, both year over year and sequentially, during the second quarter.

For full-year 2026, revenue is expected to be in the range of $270 million to $300 million, while loss per share is projected to be between $1.55 and $2.75.

The company also expects profitability improvements to begin in the fourth quarter of 2026 following the launch of its new product line, with earnings improvement targeted to continue through 2027 and beyond.

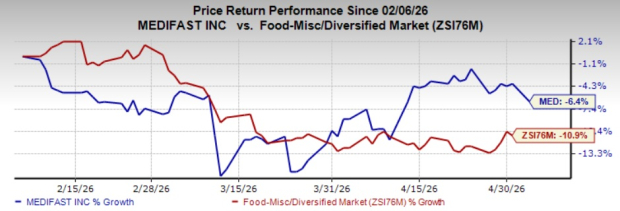

Shares of MED have lost 6.4% over the past three months compared with the industry’s decline of 10.9%.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks have been discussed below:

The Chef’s Warehouse, Inc. CHEF distributes specialty food and center-of-the-plate products in the United States, the Middle East, and Canada. CHEF currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for CHEF’s current fiscal-year sales and earnings indicates growth of 8.3 and 24.7%, respectively, from the year-ago reported figures. CHEF delivered a trailing four-quarter earnings surprise of 28.9%, on average.

Armanino Foods of Distinction, Inc. AMNF produces and markets frozen food products in the United States. AMNF currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Kimberly-Clark's current fiscal-year sales indicates growth of 7%, and the same for earnings implies a decline of 3.3% from the year-ago actuals. AMNF delivered a trailing four-quarter earnings surprise of 30.8%, on average.

Post Holdings, Inc. POST operates as a consumer packaged goods holding company in the United States and internationally. POST currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Post Holdings' current fiscal-year sales and earnings implies growth of 2.7% and 0.1%, respectively, from the year-ago actuals. POST delivered a trailing four-quarter earnings surprise of 19.6%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Chefs' Warehouse, Inc. (CHEF): Free Stock Analysis Report

Post Holdings, Inc. (POST): Free Stock Analysis Report

MEDIFAST INC (MED): Free Stock Analysis Report

Armanino Foods of Distinction Inc. (AMNF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).