The excitement around artificial intelligence (AI) has returned to Wall Street after a struggle in the last four months. As capital pours back into AI-related stocks, Nvidia (NVDA) is once again the poster child of investor enthusiasm.

While NVDA stock is up just 5% year-to-date (YTD), it has climbed roughly 11% in the last month alone. There is no doubt whether Nvidia is still the king of the semiconductor industry. But after its massive rally of 1,294% over the past five years, the question is whether the stock still has room to reward new investors. Should you buy Nvidia stock now?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com A Market Leader in a Once-in-a-Generation Shift

Nvidia’s explosive growth happened when the AI market was in its experimental stage. Although Nvidia has always been working behind-the-scenes, its graphic processing units (GPUs) became the global industry standard after the AI frenzy took over. The scale of the AI opportunity continues to expand at a breathtaking pace. The global AI market, valued at roughly $57 billion in 2020, surged to about $757.6 billion by 2025 and is projected to reach more than $3.6 trillion by 2034. This isn’t a short-term trend. It is a structural transformation across industries, ranging from cloud computing and enterprise software to healthcare, banking, and autonomous systems.

For new investors, the concern is whether Nvidia has already peaked. But they are overlooking an important aspect. Nvidia remains the undisputed leader in AI chips, not just because of performance, but because of its deeply embedded ecosystem. Its CUDA software platform, full-stack infrastructure, and continuous innovation create a powerful moat that competitors are still struggling to match. While companies like Advanced Micro Devices (AMD) and Intel (INTC) are making progress, they are still trying to catch up in both hardware efficiency and software adoption.

Nvidia ended fiscal 2026 with 65% increase in revenue to $215.9 billion and 60% increase in adjusted EPS. The data-center segment alone generated $194 billion in revenue, up 68% year-over-year (YOY). CFO Colette Kress stated that the data-center business has now scaled "by nearly 13x since the emergence of ChatGPT in fiscal 2023." Demand is being driven by both training and inference workloads. Blackwell chips are gaining strong traction with 9 gigawatts already deployed and consumed by major cloud providers, hyperscalers, AI companies, and enterprises. Notably, even Nvidia’s previous-generation hardware, including Hopper and even six-year-old Ampere chips, is fully booked across cloud platforms. This highlights how strong and widespread demand has become.

What makes Nvidia’s data-center business stand out is efficiency, as it generates the lowest cost per token and the highest revenue output for data centers. Most data centers worldwide are increasingly constrained by power. But Nvidia’s GB300 NVL72 systems offer as much as 50 times greater performance per watt and reduce cost per token by roughly 35 times compared to Hopper. At the same time, ongoing CUDA enhancements have boosted GB200 NVL72 performance by up to fivefold within just four months. The company's annual R&D budget of $20 billion supports this superior performance across chips, systems, networking, algorithms, and software.

Nvidia’s ecosystem is deeply tied to leading AI companies as it maintains strong partnerships with OpenAI, Meta Platforms (META), and Anthropic. Meta is rolling out Blackwell and Rubin GPUs at a massive scale, with deployments reaching into the millions. Production for the next-generation Rubin platform is expected to start in the second half of 2026. Meanwhile, Nvidia has invested $10 billion in Anthropic and its Claude platform, which is boosting enterprise AI use. Furthermore, Nvidia’s sovereign AI business — which surpassed $30 billion, more than tripling YOY — is another area for long-term growth. The company has seen demand coming from countries like Canada, Singapore, the U.K., France, and the Netherlands. Overtime, Nvidia believes sovereign AI spending will grow in line with GDP, as countries invest in AI the same way they built electricity and internet infrastructure.

Nvidia’s financial strength is as impressive as its growth rate. It generated $97 billion in free cash flow in fiscal 2026. The firm also returned $41 billion to shareholders through buybacks and dividends, reflecting a balance between aggressive investment and capital returns.

Nvidia will report earnings for the first quarter of fiscal 2027 on May 20. Analysts expect another blockbuster quarter, estimating a 79% increase in revenue to $78.8 billion and a 119% increase in EPS to $1.77. For fiscal 2027, analysts predict earnings will increase by 70% to $7.78, followed by 35% growth in fiscal 2028 to $10.51.

Should You Buy Nvidia Now?

For new investors with a long-term investment horizon, Nvidia is one of the purest bets on AI infrastructure, backed by real revenue and earnings growth, a robust balance sheet, strong partnerships, and sustained demand. AI demand is still in its early years. Even as competition grows, the overall market is expanding so rapidly that Nvidia can continue to grow while maintaining its dominant position.

With that said, I believe it is not too late to buy NVDA stock. The stock is still a reasonable buy at 25.5 times forward earnings.

What Do Analysts Think of NVDA Stock?

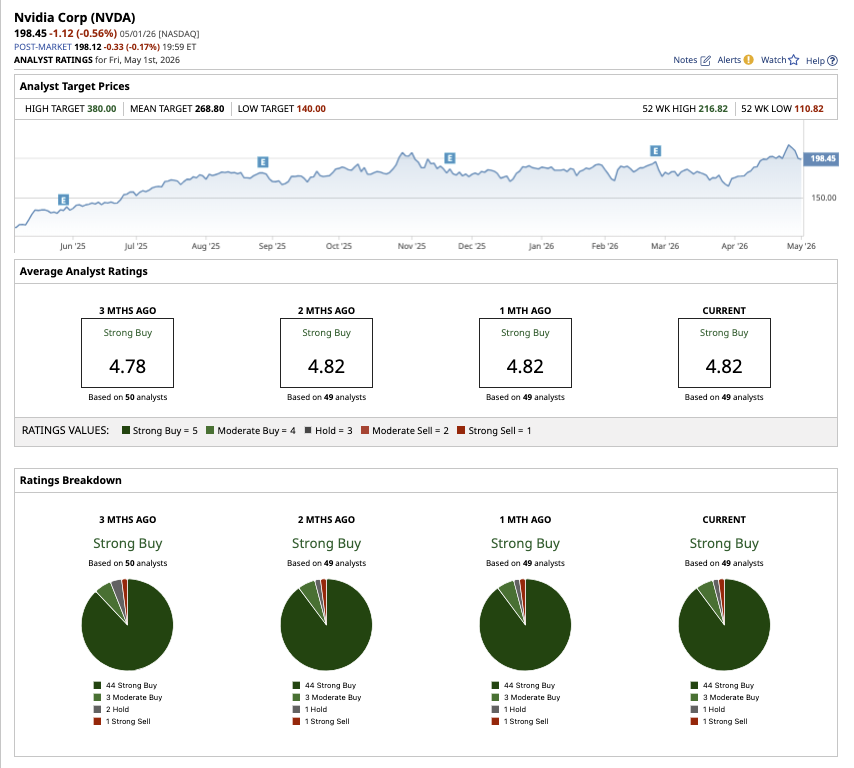

Wall Street has a mean target price of $268.80 for Nvidia stock, which implies potential upside of 37% from current levels. Plus, the high price estimate of $380 implies potential upside of 93% over the next 12 months.

Overall, NVDA stock has a consensus “Strong Buy" rating. Out of the 49 analysts covering the stock, 44 have a “Strong Buy” recommendation, three rate it a “Moderate Buy,” one has a “Hold” rating, and one analyst has a “Strong Sell" rating.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Pinterest Stock Skyrockets on Better-Than-Expected Earnings. Here's Why It's Not Too Late to Buy Wall Street Is Chasing AI Again. It’s Not Too Late to Buy Nvidia Stock. Abbott Stock Is Trading at 52-Week Lows but Insiders Are Gobbling Up Shares of This Blue-Chip Dividend Payer GameStop Stock Is Selling Off on Its Bid for eBay. Wall Street Doesn't Think the Deal Will Go Through Anyway.