AppLovin Corporation APP will report its first-quarter 2026 results on May 6, after the bell.

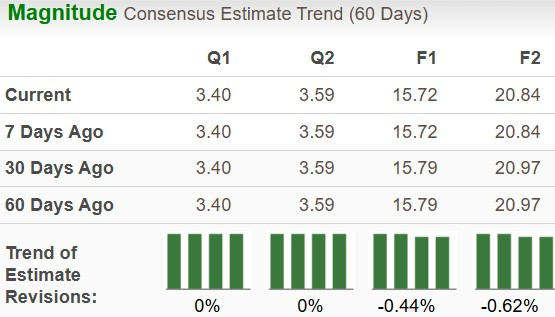

The Zacks Consensus Estimate for earnings in the to-be-reported quarter stands at $3.4, indicating 103.6% growth from the year-ago reported quarter. The consensus estimate for revenues stands at $1.77 billion, implying 19.5% year-over-year growth. There have been no changes or revisions to analyst estimates lately.

The company has a strong history of earnings surprises. Earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, with an earnings surprise of 11.1%, on average.

Q1 Earnings Beat likely for APP

Our proven model does not conclusively predict an earnings beat for APP this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

APP has an Earnings ESP of -0.18% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

APP’s Price Dynamics and Valuation

The stock has plunged 24% over the past six months compared with the broader industry's 8% decline, but the sell-off could not make valuations compelling. Even after the correction, ARM continues to trade at a forward 12-month price-to-earnings multiple of 27.19x, above the industry average of 23.01x. It trades at a forward 12-month price-to-sales multiple of 18.13x, way above the industry average of 2.49x, suggesting the stock remains far from inexpensive.

Investment Considerations

AppLovin’s integrated marketplace continues to demonstrate meaningful structural strengths. The combination of MAX’s real-time bidding infrastructure and Axon 2.0 model enhancements is driving higher bid density and improved ad matching, translating into strong operating momentum. This has been evident through the fourth quarter of 2025, with management signaling confidence in continued sequential growth into early 2026 despite typical seasonal softness.

A key long-term lever remains the company’s ability to improve conversion rates from historical low single-digit levels toward a higher steady-state range. This potential is supported by increasing advertiser diversity beyond gaming and ongoing model refinement. As more bidders enter the ecosystem, AppLovin benefits from expanding demand and favorable take-rate dynamics, positioning the platform for sustained monetization gains and share expansion over time.

Despite these positives, the early-stage nature of its e-commerce initiatives and elevated valuation contribute to a balanced investment case. With the company carrying a Zacks Rank #3 (Hold), a cautious stance appears appropriate as investors weigh the company’s structural strengths against near-term uncertainties. Existing shareholders may benefit from staying invested to capture long-term upside, while new investors could consider waiting for greater clarity or more attractive entry points.

How AppLovin Compares With Key U.S. Peers

TheTrade Desk TTD operates a demand-side platform focused on programmatic advertising, with a strong focus on data-driven targeting. While The Trade Desk benefits from premium brand exposure, its margin profile is more sensitive to advertising cycles than AppLovin. The Trade Desk emphasizes reach and transparency, whereas AppLovin emphasizes performance. As a result, TTD competes more on scale than efficiency.

Unity Software U also intersects with advertising through its real-time 3D and monetization tools. However, Unity Software’s ad business is closely tied to developer ecosystems and remains more volatile. Unlike AppLovin, Unity Software is still balancing growth with profitability, making AppLovin’s margin stability a key differentiator among these peers.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AppLovin Corporation (APP): Free Stock Analysis Report

The Trade Desk (TTD): Free Stock Analysis Report

Unity Software Inc. (U): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).