The market has been punishing Duolingo, Inc. DUOL. Shares are down 79% over the past year and down 12.5% over the past three months, while the S&P 500 rose over both periods.

That gap sets up a familiar debate. Is this a rare chance to buy long-term product optionality at a better price, or a signal that near-term execution risks are rising faster than the opportunity?

DUOL’s Big Drawdown Sets Up the Debate

DUOL’s recent performance forces investors to separate time horizons. The company still has clear multi-year levers tied to product depth, new subjects, and artificial intelligence-driven personalization.

At the same time, the near-term setup tilts negatively. Management is prioritizing user growth over immediate monetization through 2026, which can pressure margins before the benefits show up in the numbers.

DUOL Revenue Mix Shows Subscription Strength

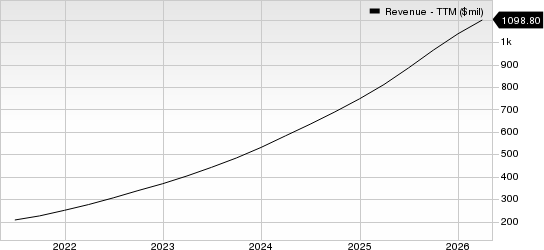

Duolingo’s revenue base is already anchored by subscriptions. Total 2025 revenue reached $1.0 billion, up 39% from $748.0 million in 2024.

Subscriptions contributed $873.4 million, about 84% of total revenue. “Other” revenue was $164.1 million, including advertising ($79.7 million), the Duolingo English Test ($42.0 million), and in-app purchases ($40.5 million).

That mix makes conversion and retention central. With subscriptions doing most of the work, the clearest upside comes from turning more free users into paying users and keeping them engaged without adding friction.

Duolingo, Inc. Revenue (TTM)

Duolingo, Inc. revenue-ttm | Duolingo, Inc. Quote

Duolingo’s 2026 Is About Users, Not Near-Term Profit

The near-term caution is straightforward. Management is keeping ad load stable, broadening access to artificial intelligence-powered learning, and running extensive pricing and tiering tests.

Those choices are likely to compress margins before benefits accrue. Broader artificial intelligence rollout raises inference costs and can lower gross margins in 2026. Operating leverage is also pressured as research and development and sales and marketing are expected to grow faster than revenue during the investment year.

DUOL Valuation: Premium Multiple vs Peers

Even after the drop, valuation is not cheap versus the benchmarks cited. DUOL trades at 34.62 times forward 12-month earnings, versus 23.01 times for the industry. The five-year median forward price-to-earnings multiple referenced is 107.32 times, which shows the stock has historically carried a premium.

Peer View

This dynamic becomes more concerning when compared to broader digital learning and skill development players such as Coursera COUR and Chegg CHGG. Coursera operates at the intersection of higher education and workforce upskilling, with enterprise and university partnerships offering diversification beyond direct-to-consumer subscriptions. Although challenged in recent quarters, Chegg still represents a large installed base in academic support services.

Coursera’s institutional relationships provide structural demand that differs from consumer-driven language learning cycles. Chegg, on the other hand, illustrates how quickly AI disruption narratives can pressure education platforms when monetization visibility weakens. In that context, Duolingo’s premium valuation appears increasingly sensitive to execution risks.

DUOL Stock: Premium Valuation Meets Near-Term Execution Risk

Duolingo’s long-term story around user growth, product expansion, and AI-driven personalization remains intact, but the near-term setup is increasingly difficult to justify at current valuation levels. The company is deliberately prioritizing scale over monetization through 2026, which is likely to pressure margins while growth moderates. At the same time, DUOL continues to trade at a premium multiple relative to peers, leaving limited room for execution missteps. With earnings expectations facing pressure and visibility on operating leverage still uncertain, the risk-reward appears skewed to the downside. Until clearer signs of monetization and margin recovery emerge, DUOL looks more like a sell than a buy.

DUOL currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chegg, Inc. (CHGG): Free Stock Analysis Report

Coursera, Inc. (COUR): Free Stock Analysis Report

Duolingo, Inc. (DUOL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).