EMCOR Group, Inc.’s EME growing exposure to data center infrastructure emerged as a key growth driver in the first quarter of 2026, reflecting rising AI-driven demand across electrical construction markets. In its U.S. electrical construction segment, revenues from network and communications, where EMCOR houses its data center business, rallied nearly 50% year over year, driven by strong data center demand. This surge served as a powerful engine for the broader segment, single-handedly accounting for approximately two-thirds of the electrical division's total quarterly revenue growth.

The momentum was even more pronounced within the mechanical construction segment, which saw network and communications revenues surge by 86% year over year. This explosive expansion was directly underpinned by escalating cooling requirements and rapid advancements in liquid cooling technologies, which are tailored precisely for high-intensity AI workloads and are continuing to unlock robust, large-scale opportunities across their mechanical operations.

Management pointed to “no sign of slowing demand” in data centers, citing customer investments in AI infrastructure, cloud infrastructure and broader digital transformation. This momentum also helped lift EMCOR’s remaining performance obligations to a record $15.62 billion, up 32.9% year over year, giving the company stronger revenue visibility for the rest of 2026.

The AI opportunity is not just boosting sales, but also expanding EMCOR’s strategic relevance. Management noted that data center bookings are coming from both electrical and mechanical scopes, with revenue growth in network and communications up by roughly $240 million in electrical and $280 million in mechanical. However, growth may come with some margin trade-offs, as newer AI data center projects can involve evolving designs, larger scopes and more GMP or cost-plus contract structures.

Overall, AI appears to be a clear tailwind for EMCOR’s growth outlook. The company raised its 2026 revenue guidance to $18.5 billion-$19.25 billion and EPS guidance to $28.25-$29.75, reflecting strong demand, a record backlog and confidence in execution across large-scale, mission-critical projects.

EMCOR’s Competitive Landscape: AI Infrastructure in Focus

EMCOR operates in an increasingly competitive mission-critical infrastructure market alongside major industry players such as Sterling Infrastructure, Inc. STRL and Quanta Services, Inc. PWR. All three companies are benefiting from accelerating investment tied to AI-driven data centers, electrification, grid modernization and large-scale infrastructure development, though their operating models and execution capabilities differ meaningfully.

Sterling has recently delivered exceptional momentum in mission-critical site development. In the first quarter of 2026, revenues surged 92% year over year, adjusted EBITDA more than doubled and margins reached a record 20%. Growth was driven by the E-Infrastructure segment, where revenues climbed 174% on strong hyperscale data center demand, semiconductor-related awards and expanding multi-year customer programs. Sterling’s backlog reached $5.2 billion, including more than $5 billion of visibility within E-Infrastructure alone.

Quanta, meanwhile, continues to benefit from its unmatched scale in electric power transmission, distribution and utility infrastructure. The company reported a record backlog of $48.5 billion, supported by strong demand across power delivery, technology-load infrastructure, renewable energy and grid modernization markets. Quanta’s investments in transformer manufacturing and off-site fabrication further strengthen its execution capabilities as customers increasingly prioritize schedule certainty in complex infrastructure projects.

EME Stock’s Price Performance & Valuation Trend

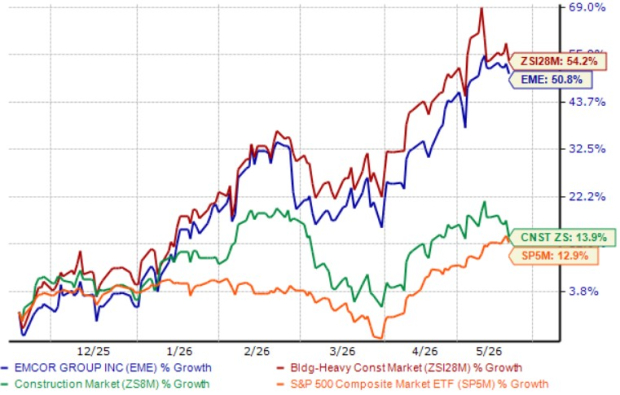

Shares of this Connecticut-based infrastructure service provider have gained 50.8% in the past six months, underperforming the Zacks Building Products - Heavy Construction industry, but outperforming the Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

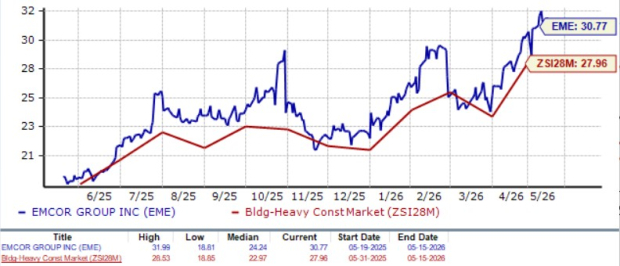

EME stock is currently trading at a premium compared with the industry, with a forward 12-month price-to-earnings (P/E) ratio of 30.77, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of EME

EME’s earnings estimates for 2026 and 2027 have moved upward in the past 30 days. The estimates for 2026 and 2027 imply year-over-year growth of 10.8% and 9.3%, respectively.

Image Source: Zacks Investment Research

EMCOR stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Sterling Infrastructure, Inc. (STRL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).