Avnet Inc. AVT and Arrow Electronics Inc. ARW are two of the world’s largest players operating in the electronic components industry. Avnet is engaged in the distribution of semiconductors and Interconnect, passive and electromechanical devices (IP&E) and provides supply chain management services. Arrow Electronics focuses on selling semiconductor products, IP&E components and IT hardware and software to original equipment manufacturers and electronics manufacturing services providers.

Both AVT and ARW play key roles in the global technology supply chain by helping manufacturers and businesses source semiconductors, electronic components and infrastructure solutions. However, from an investment point of view, one stock offers a more favorable outlook than the other right now. Let’s break down their fundamentals, growth prospects, market challenges and valuation to determine which stock offers a more compelling investment case.

The Case for AVT Stock

Avnet is benefiting from strong demand in AI infrastructure, networking and industrial markets. In the third quarter of fiscal 2026, the company reported revenues of $7.1 billion, up 34% year over year and 13% sequentially. Management stated that AI data center, networking and industrial markets were the biggest growth drivers during the third quarter. The company also delivered record sales of $6.67 billion in its Electronic Components business, which increased 34.7% year over year on the back of robust demand across most end markets.

AI-related demand is becoming a larger part of AVT’s business. In the third quarter of fiscal 2026, management stated that the company’s direct exposure to AI and data center customers has increased from around 5-7% previously to nearly 10-15% now. Most of this business is tied to Asia, especially Taiwan, where demand from hyperscalers and server customers remains strong. Networking demand also improved across regions, with the Americas showing strong growth during the third quarter.

The company is also benefiting from demand for components that support AI infrastructure. AI buildouts are increasing demand for products tied to power management, cooling systems, connectors, capacitors, resistors and sensors. This helped AVT’s interconnect, passive and electromechanical (IP&E) business grow 25% year over year in the third quarter.

However, one of the weaker areas in AVT’s third quarter was gross margin performance. AVT’s gross margin in the third quarter contracted 68 basis points year over year to 10.4%. A major problem is the growing dependence on Asia. Asia now contributes nearly half of AVT’s total revenues. The region usually operates at lower margins because pricing is highly competitive and customers buy in large volumes. As a result, as Asia becomes a larger part of the business, it puts pressure on AVT’s consolidated gross margins.

The Case for ARW Stock

Arrow Electronics is witnessing strong growth in its Enterprise Computing Solutions (ECS) business on the back of strong demand for AI and cloud infrastructure. In the first quarter of 2026, ECS sales increased 39% year over year to $2.8 billion, while billings also rose 39% to $6.4 billion. Management stated growth was driven by cloud, AI, infrastructure software, cybersecurity and data intelligence demand. This shows that the company continues to benefit from rising enterprise spending on AI workloads and data center expansion.

Arrow Electronics also saw stronger demand for storage and computing products during the first quarter. Management stated that memory supply constraints encouraged customers to place orders earlier to secure product availability. Hyperscaler customers accelerated data center deployments into the first quarter, which supported ECS growth and increased supply chain services revenues. Arrow Electronics expects AI-related infrastructure demand to remain healthy through the rest of the year.

Another important factor is the diversified nature of the ECS business. The Hardware business contributes only about 25% of ECS revenues. The remaining contribution comes from software, cloud and infrastructure-related offerings. This reduces Arrow Electronics’ dependence on hardware demand alone and may help support more stable growth over time. If memory shortages continue, customers could shift more workloads toward public cloud solutions, which may further benefit ARW’s cloud business.

Arrow Electronics is also expanding its digital platform, Arrowsphere, which helps customers source, manage and scale cloud technologies. Management believes the platform supports recurring revenue growth and deeper customer relationships. While some of the growth in the first quarter benefited from extra shipping days and accelerated customer orders, ARW’s strong exposure to AI infrastructure, cloud and enterprise software markets could continue supporting ECS momentum in 2026.

AVT vs. ARW: Earnings Estimate Trend

The earnings estimate revision trend for the two companies reflects that analysts are turning more bullish toward ARW.

The Zacks Consensus Estimate for AVT’s 2026 and 2027 EPS is pegged at $5.12 per share and $7.30 per share, respectively. The estimates for 2026 and 2027 have been revised up by 4.1% and 3%, respectively, over the past seven days.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for ARW’s 2026 and 2027 EPS is pinned at $17.97 per share and $19.48 per share, respectively. The estimates for 2026 and 2027 have been revised up by 10.5% and 8.5%, respectively, over the past seven days.

Image Source: Zacks Investment Research

AVT vs. ARW: Price Performance and Valuation

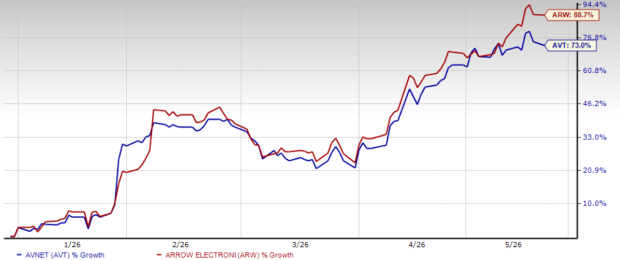

Year to date, shares of AVT and ARW have surged 73% and 88.7%, respectively.

AVT vs. ARW: YTD Price Return Performance

Image Source: Zacks Investment Research

Currently, AVT is trading at a forward sales multiple of 0.25X, lower than ARW’s forward sales multiple of 0.30X. ARW does seem pricey compared with AVT. However, ARW’s robust financial performance and stronger earnings estimate revisions justify its higher valuations.

AVT vs. ARW: Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

Conclusion: ARW Has an Edge Over AVT

Both AVT and ARW are key players in the electronic components industry. However, AVT continues to face pressure on gross margins as Asia becomes a larger part of its revenue mix. In contrast, ARW is seeing strong results supported by rising AI and cloud spending, demand for its products remains strong, and earnings estimates are moving higher.

Currently, ARW sports a Zacks Rank #1 (Strong Buy), making the stock a clear winner over AVT, which has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Avnet, Inc. (AVT): Free Stock Analysis Report

Arrow Electronics, Inc. (ARW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).