Chewy Inc. CHWY is currently trading at a trailing 12-month price-to-sales (P/S) multiple of 0.59X, which is at a discount compared with the industry’s average of 2.03X. The company is a leading online pet retailer, utilizing its robust e-commerce platform to serve a growing population of pet owners. The key issue for investors is whether this discounted valuation reflects underlying business challenges or presents a buying opportunity.

CHWY’s Valuation Snapshot

Image Source: Zacks Investment Research

This valuation is especially notable when compared with peers such as Central Garden & Pet Company CENT, which has a trailing 12-month P/S of 0.78X, Petco Health and Wellness Company, Inc. WOOF at 0.13X and BARK, Inc. BARK at 0.18X.

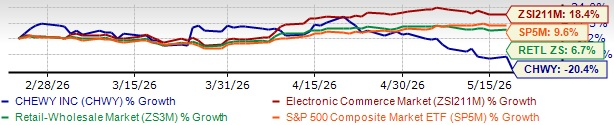

However, Chewy’s recent stock performance partly explains its discounted valuation. Closing yesterday’s trading session at $19.66, the stock has tumbled 20.4% in the past three months, underperforming the industry’s growth of 18.4%. The company also trailed the Retail - Wholesale sector’s 6.7% increase and the S&P 500 index’s 9.6% rise.

Image Source: Zacks Investment Research

Chewy’s share performance has been pressured by moderating pet industry growth, softer household formation trends and the absence of meaningful pricing tailwinds. Investor sentiment was further impacted by expectations for slower near-term sales growth, particularly with first-quarter growth projected to mark the low point of 2026.

CHWY has underperformed peers such as Central Garden and Petco Health, while outperforming BARK. In the same period, shares of Central Garden and Petco Health have declined 2.6% and increased 0.4%, respectively. Meanwhile, BARK’s shares plunged 39.5%.

CHWY’s Performance vs. Peer Performance

Image Source: Zacks Investment Research

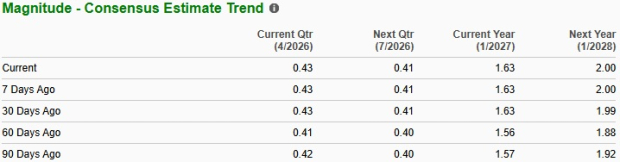

Despite CHWY’s recent stock decline, upward estimate revisions have helped build some confidence in the stock. The Zacks Consensus Estimate for earnings per share (EPS) has moved higher over the past 60 days. Estimates for the current quarter have increased 2 cents to 43 cents per share, while estimates for the next quarter have risen 1 cent to 41 cents.

Image Source: Zacks Investment Research

What Is Driving Chewy’s Upward Earnings Estimate Revisions?

Chewy’s upward earnings estimate revisions are being supported by improving business momentum and its ability to gain market share within the resilient pet care industry. Demand trends remain stable due to recurring purchase behavior and strong emotional attachment between consumers and their pets, allowing Chewy to benefit from consistent engagement across its platform. The company’s active customer base reached 21.3 million in fiscal 2025, while management also highlighted continued sequential customer additions, reinforcing confidence in sustainable long-term growth.

A major contributor to the improving earnings outlook is Chewy’s highly recurring revenue structure. The company’s Autoship program now accounts for more than 83.3% of total net sales and continues to grow faster than overall revenues. This recurring model improves revenue visibility, enhances customer retention and supports stronger customer lifetime value. At the same time, growth in higher-margin categories such as health, wellness and veterinary services is driving higher spending per active customer and strengthening profitability trends.

Chewy is also leveraging technology and artificial intelligence to improve efficiency and customer experience across its operations. Management noted that the company has built a unified enterprise data platform and is embedding AI across customer service, fulfillment, pharmacy operations and marketing functions. These initiatives are expected to improve personalization, optimize workflows and lower operating costs, creating a stronger margin profile over time. Management anticipates that AI-led efficiencies will generate a financial benefit in the low tens of millions of dollars in fiscal 2026, with the potential to scale to more than $50 million in annualized savings by fiscal 2027 as adoption broadens.

In addition, strategic expansion initiatives are further supporting analysts’ confidence in Chewy’s long-term earnings potential. The company continues to scale the Chewy Vet Care platform, which now operates 18 locations across five states, helping deepen customer relationships and expand its presence in the high-growth pet healthcare market. CHWY is also expanding its private-label offerings through Chewy Made, creating additional opportunities in the large consumables category while supporting higher-margin growth.

What to Expect From CHWY in the Future?

On its fourth-quarter earnings call, CHWY projected fiscal 2026 net sales of $13.6-$13.75 billion, representing approximately 8-9% year-over-year growth. The outlook is expected to be supported by continued market-share gains, stable pet industry demand and balanced contributions from active customer growth and higher spending per active customer. Management also noted that the forecast does not rely on any meaningful pricing inflation, highlighting confidence in the underlying strength of demand and customer engagement.

The company also anticipates another year of meaningful profitability expansion, guiding for adjusted EBITDA margins of 6.6-6.8%, implying nearly 100 basis points of year-over-year improvement. Notably, EBITDA growth is expected to significantly outpace revenue growth, driven by operating leverage, disciplined cost management and structural margin drivers. These include SG&A efficiencies, growth in higher-margin categories such as health and sponsored advertising, fulfillment optimization and AI-led productivity initiatives, which will contribute meaningful cost savings over time.

How to Play CHWY Stock: Buy, Hold or Sell?

Chewy offers an attractive long-term opportunity, supported by its resilient Autoship-driven business model, expanding customer base and steady market-share gains. The company’s growing presence in vet care, private-label products and AI-enabled operations is enhancing customer engagement, improving efficiency and supporting long-term profitability despite recent stock weakness.

Given this backdrop, existing investors may consider gradually increasing their exposure, while new investors could view the recent pullback as an attractive entry opportunity. Chewy currently has a Zacks Rank #2 (Buy).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Central Garden & Pet Company (CENT): Free Stock Analysis Report

Petco Health and Wellness Company, Inc. (WOOF): Free Stock Analysis Report

Chewy (CHWY): Free Stock Analysis Report

BARK, Inc. (BARK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).