The memory industry has mostly remained cyclical. However, now artificial intelligence (AI) is consuming memory at a pace that might be difficult to sustain for years. Advanced AI systems require significantly larger memory to function, and memory-chip companies like Micron (MU) are capitalizing on this. Micron Technology designs and manufactures the chips that store, move, and process data inside devices. Its products include DRAM memory, NAND flash storage, and high-bandwidth memory (HBM).

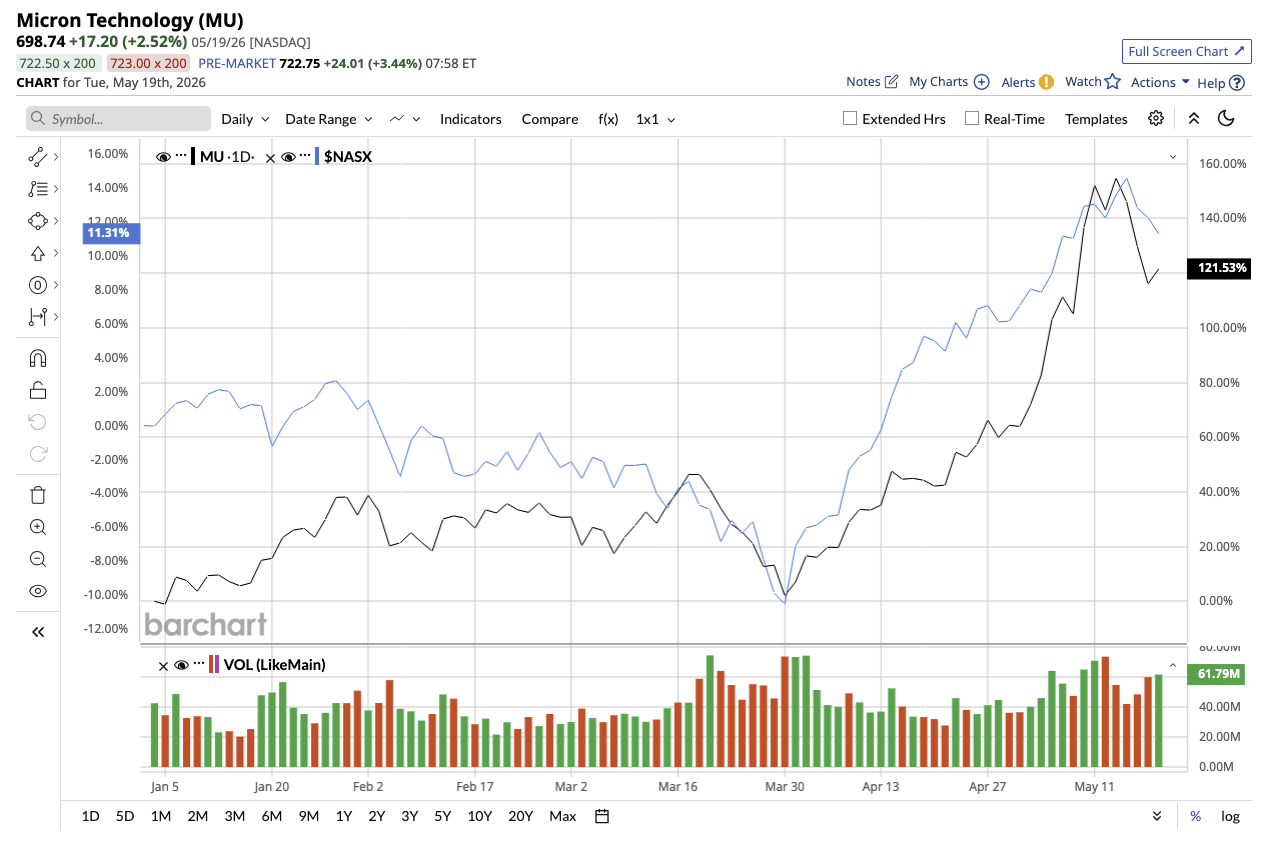

Micron shares have surged an eye-popping 153% year-to-date, and 637% over the past year. But its fiscal Q2 earnings implies this rally may just be the beginning. I believe the stock still does not fully reflect how dramatically the memory market is changing.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comThe HBM Opportunity Could Be Huge

In the second quarter of fiscal 2026, Micron reported a 196% year-over-year increase in revenue to $23.9 billion. The quarter also marked the largest sequential increase of 75%, with sales rising by $10.2 billion in just one quarter. DRAM contributed 79% to total revenue, generating a record $18.8 billion in sales. NAND also generated $5 billion in sales. But the most drastic improvement was in profitability. Adjusted earnings-per-share climbed to $12.20 per share from $1.56 in the year-ago quarter. Gross margin also expanded to 75%, nearly doubling from the prior-year quarter.

Micron’s HBM is its prized jewel. These are ultra-fast stacked memory chips used in advanced AI accelerators and GPUs from companies like Nvidia (NVDA). HBM helps AI systems rapidly process massive datasets during training and inference workloads.

At Nvidia’s GTC (GPU Technology Conference), Micron announced that it had begun mass shipments of its HBM4 36GB 12-Hi memory solution built for NVIDIA’s Vera Rubin platform. One of the reasons why I like Micron is how quickly the company is progressing generations of HBM. The company stated that volume production for HBM4E is expected to begin in 2027.

Micron Is Preparing for a Decade of Demand Growth

Micron issued a bold target for the third quarter, expecting revenue of $33.5 billion, plus or minus $750 million. The company believes this single quarter revenue will exceed its annual revenue in years prior to fiscal 2024. Gross margin is projected to climb to around 81%, while earnings per share are expected to reach a record $19.15.

Another reason why Micron is already my 2026 winner is because it isn’t preparing just for the next quarter. In fact, Micron is gearing up for a decade of demand growth. Micron expects fiscal 2026 capital expenditures to exceed $25 billion. The company is aggressively expanding manufacturing capacity in Idaho, New York, Singapore, Japan, Taiwan, and India to meet its multi-year demand supercycle. Additionally, post the completion of acquisition of the Tongluo site from Powerchip Semiconductor, Micron now expects meaningful production shipments from the existing fab to begin in fiscal 2028.

Micron also confirmed that commercial shipments have already started from its assembly and test facility in India. The company won’t be making such huge capital commitments globally unless it is confident that demand visibility will extend years into the future.

Management also believes its current revenue and earnings strength is sustainable. This is likely why the company announced a dividend increase of 30% in the quarter to $0.15 per share. Micron generated $6.9 billion in free cash flow, that allowed it reduce debt by $1.6 billion. It ended Q2 with $16.7 billion in cash and investments.

Analysts predict a 603% increase in earnings in fiscal 2026, followed by 76% increase in fiscal 2027. Despite these exceptional growth targets, Micron is trading at a discount of 6 times forward earnings, probably because investors still view the memory industry as cyclical.

Why this Rally May Go On

Memory is no longer a cyclical component in modern devices. It is a critical resource for AI infrastructure, autonomous systems, advanced robotics, and next-generation computing platforms. And Micron, with its tried-and-tested successful storage products has built a loyal client base. While semiconductor growth stocks may remain volatile in the short run, Micron’s long-term growth story remains intact.

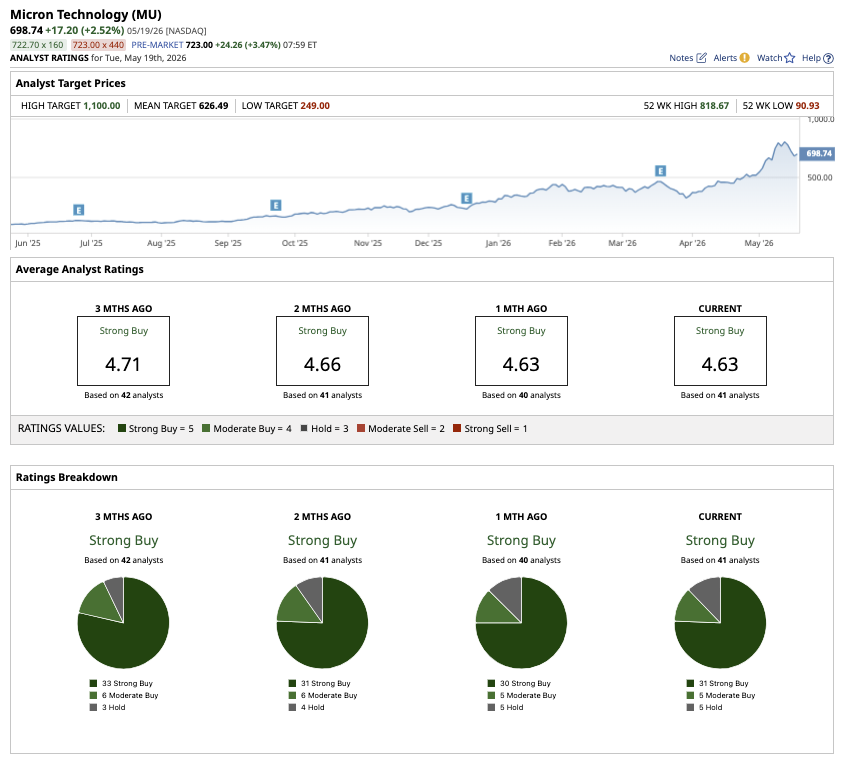

Overall, Wall Street remains strongly bullish about MU stock. Of the 41 analysts covering the stock, 31 rate it as a “Strong Buy,” five have a “Moderate Buy” rating, and five analysts recommend a “Hold.” The stock has surpassed its average target price of $626.49. But the high price stands of $1,100 suggests potential upside of 54% over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Is Warming Up to ServiceNow Stock. That’s Because It’s Now a Bet on Agentic AI. INM Stock Alert: What to Know as InMed, Mentari Announce Merger The $2.6 Billion Power Play: How Akamai Is Weaponizing Debt to Build the AI Edge Up 153% YTD, Here's Why Micron Stock Is Already My 2026 Winner