Over the last few weeks, shares of Apple rallied from about $245 to a high of $303.20. All thanks to exceptional quarterly results, strong guidance, a massive $100 billion stock buyback, and strong demand for its iPhone 17 in the U.S. and China. In fact, in its most recent quarter, Apple said revenue soared 17% year-over-year (YOY) to $111.18 billion. Analysts were only looking for $109.66 billion. EPS of $2.01 easily beat expectations of $1.95 per share. Investor confidence strengthened considerably after Apple delivered another quarter that exceeded Wall Street expectations across several key metrics.

www.barchart.com

www.barchart.com Moving forward, the company expects revenue to increase between 14% and 17% YOY, which is above analyst expectations for 9.5% YOY growth. All of which is great news, and would explain the reason that Apple soared in recent weeks.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

However, Apple’s Current Valuation May be Difficult to Justify

Analysts at KeyBanc Capital argue that Apple’s current valuation is “stretched” and that spending data points to “initial cracks in the bulls’ multi-year compounding growth view,” as quoted by StreetInsider.com.

In fact, as per the firm, spending data suggests U.S. consumer demand for Apple hardware is returning to more typical seasonal patterns after several years of unusually strong growth. They also argue that this could signal the end of the expansion cycle that helped force Apple’s valuation higher. Analysts point out that future growth may increasingly depend on international markets, particularly China.

Apple is stretched, overdue for healthy profit-taking

At the moment, Apple trades at 34.07 times price-to-earnings, which is well above its five-year range of between 30 times and 35 times EPS. Furthermore, It’s 40.6% higher than the sector average of 24.24 times. Technically, Apple is stretched at all-time highs, which isn’t sustainable, especially with how stretched the stock has become using indicators, such as relative strength (RSI), MACD, Williams’ %R, and Full Stochastics. In addition, we have to consider that the Apple iPhone prices are being slashed in China. According to MacRumors.com, Apple cut prices on its iPhone 17 Pro Series in China by about 1,000 yuan, or $138 USD, as it faces intense competition. In fact, competitors such as Huawei are taking smartphone market share from Apple in China. As noted by the South China Morning Post, Huawei claimed the top spot in China’s smartphone market with “its highest share in five years.”

Plus, Apple is seeing margin headwinds thanks to higher prices for DRAM and NAND memory chips. Current CEO Tim Cook even noted that memory costs could be “significantly higher” in the June quarter. "I can tell you that beyond the June quarter, we believe memory costs will drive an increasing impact on our business. And we'll continue to evaluate this,” Cook added, as quoted in an Apple earnings call.

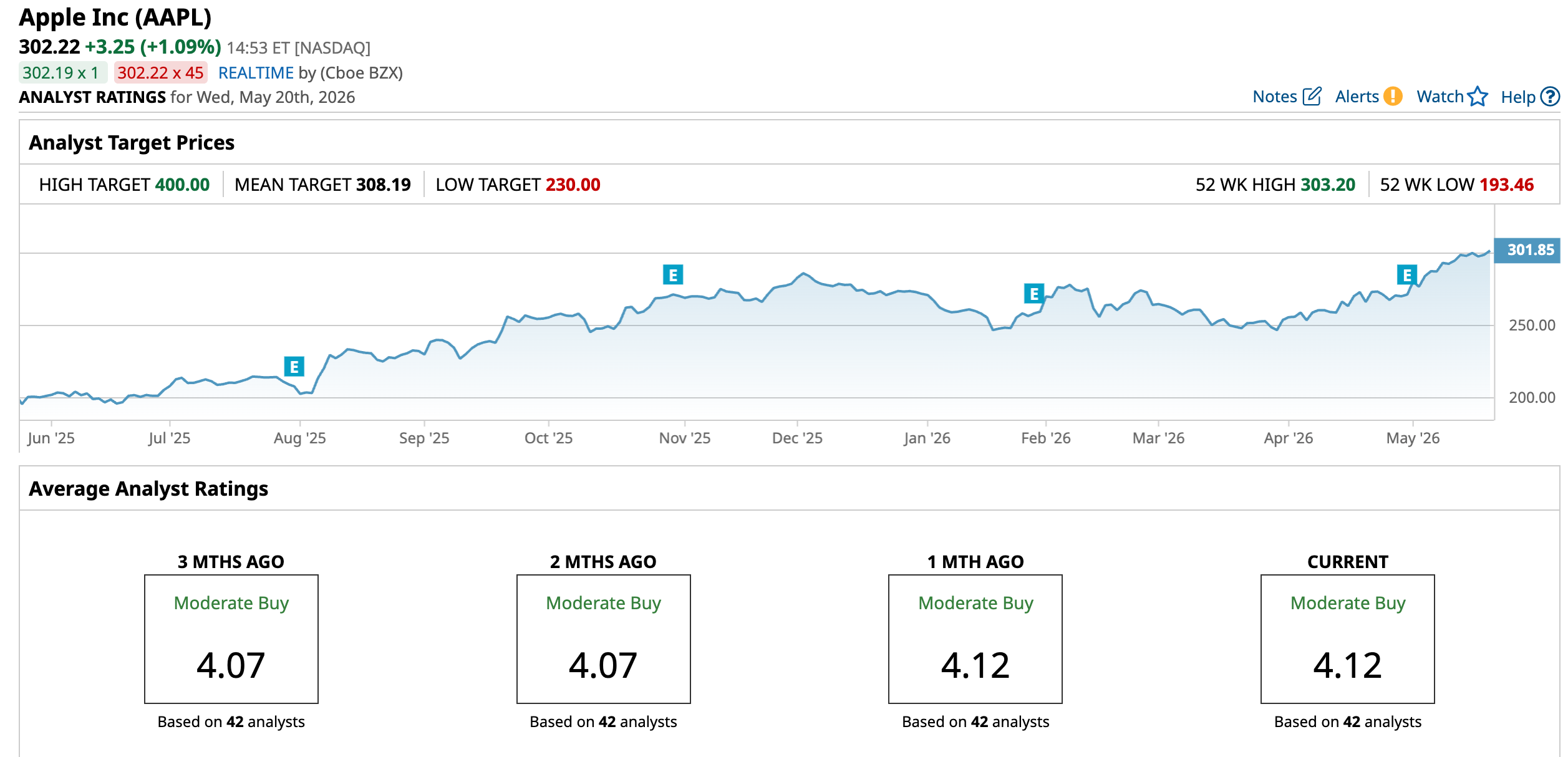

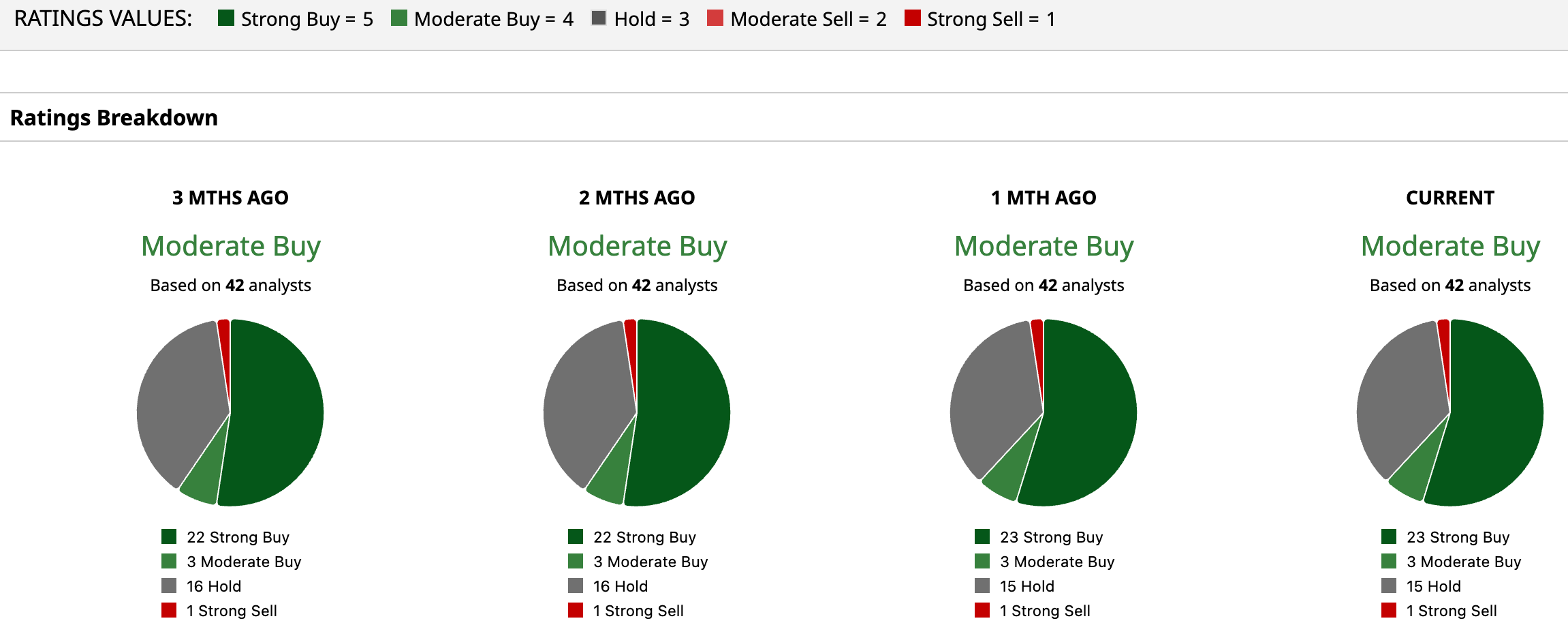

What Do Analysts Say About AAPL Stock?

Of the 42 analysts covering the Apple stock, 23 have a “Strong Buy” rating, three have a “Moderate Buy” rating, 15 have a “Hold” rating, and one has a “Strong Sell” rating. The mean target price of $308.19 implies a marginal 1.98% potential upside from current levels. Meanwhile, the high-end target of $400 implies as much as 32.4% possible growth from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com For us, we agree with the “stretched” assessment, technically and fundamentally. We’d wait for healthy pullbacks in the stock before taking a position. In the end, Apple remains one of the strongest companies in the tech industry, backed by strong sales, earnings, massive cash flow, impressive guidance, and a $100 billion buyback program to boot. Still, despite that, some analysts argue its current valuation has become far too stretched, especially as U.S. consumer demand returns to normal seasonal patterns. Nevertheless, future growth may depend more on international markets, like China, as noted by analysts at KeyBanc. Over the long haul, Apple is a strong buy opportunity. Short-term, expectations remain very high, with a stretched valuation.

On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Fervo Energy Is Already Cooling Off. This AI Infrastructure IPO Needs Time to Show Real Results. KeyBanc Turns Cautious on Apple Stock as Valuation Concerns Grow. It’s Due for Profit-Taking. Berkshire Hathaway Sold Off 5 Longtime Warren Buffett Stocks. What the New Abel Era Means for You. Activist Investors Are Determined to Turn CarMax Stock Around. How to Play KMX Here.