Financial software company Intuit (INTU) is looking to be the latest to trim its workforce. In an internal email circulated among employees, CEO Sasan Goodarzi has reportedly said that the move to shed about 3,000 jobs in the company is being done to operate more effectively and focus on assimilating AI across its products and services.

To put it simply, AI may do the jobs of these people, and the company will save costs. Consequently, the shares should have reacted positively, right? Wrong. INTU stock ended 4% lower in yesterday's trading session.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Intuit

Founded in 1983, Intuit develops financial and tax software for consumers, small businesses, accountants, and self-employed workers. Its popular products include TurboTax, QuickBooks, CreditKarma, and MailChimp. Notably, across its ecosystem, there are about 100 million customers worldwide.

Valued at a market cap of $106 billion, INTU is down 53% on a YTD basis. The stock also offers a dividend yield of 1.19%, and has been raising dividends consecutively over the past 14 years. Further, with a payout ratio of about 20%, dividend raises have more room to run.

www.barchart.com

www.barchart.com So, will the lightening of its employee list jolt INTU shares back toward an upward path? Let's find out.

Beat & Raise Q3

Intuit's Q3 was marked by a beat and raise, with both revenue and earnings exceeding Street estimates.

Total revenues went up by 10% from the previous year to $8.6 billion. All key products, except ProTax, saw their revenues increase when compared to the prior year. While TurboTax and Credit Karma revenues were up 7% and 15% to $4.4 billion and $631 million, respectively, ProTax revenue at $278 million remained flat.

Earnings rose by 10% in the same period to $12.80 per share, surpassing the consensus estimate of $12.57 per share. Notably, this was the ninth consecutive quarter of earnings beat from a company that has increased its revenue and earnings at impressive CAGRs of 16.24% and 22.9%, respectively.

Moreover, the company raised its dividend by 15% to $1.20 per share while getting approval for a new $8 billion share buyback program.

For Q4, Intuit expects revenue to grow by 11% to 12%, with earnings per share forecasted to be between $3.56 to $3.62. Street estimates for the same is pegged at $3.26 per share.

Notably, the company's workforce expenses for the likes of engineers, marketing, and finance are spread across three heads: “selling and marketing,” “research and development,” and “general and administrative.” In Q3 2026, the total expenses for these heads came in at about $3 billion, up about 12% from the previous year.

Over the past five years, these segments have seen their share of revenues decline. While it was 55% of total revenues in FY21, the same for FY25 stood at 50.7%. And although there was a job cut of 1,800 within this period, it was more of a reallocation for hiring in areas that the company considered required for its growth, like engineering, product, and customer relations. Yet net margins have actually declined over this period, from 21.4% in FY21 to 20.55% in FY25.

Meanwhile, net cash from operating activities increased to $7.5 billion for the nine months ended April 30, 2026, from $5.8 billion in the year-ago period. Overall, Intuit closed the quarter with a cash balance of $4.7 billion, much higher than its short-term debt levels of $750 million.

The stock is also trading at reasonable levels. While its forward P/E and P/CF of 17.21x and 15.31x are below the sector medians of 24.24x and 18.53x, respectively, the forward P/S of 5.20x is just above the sector median of 3.29x.

Go Into Intuit

Just like I had highlighted in my Zscaler piece, the fears around “SaaSpocalypse” are overblown. There it was, cybersecurity, and with Intuit, it is financial data. Both are critical areas that users and enterprises would not like to outsource to “vibe coding.”

One of the early companies to pivot into an integrated, AI-driven financial platform, Intuit is deeply embedded in its users' accounting and tax systems. This is reflected in its offerings. While QuickBooks and Mailchimp serve a broad range of customers spanning small and medium-sized businesses, the self-employed, and an increasingly significant cohort of mid-market enterprises, TurboTax approaches the tax preparation challenge differently, pairing AI capabilities with human expertise to guide users through the filing process. Credit Karma rounds out the ecosystem by helping users identify loan and credit card options, drawing on the data it holds to inform and support the approval process.

Notably, what is particularly telling about Intuit's position is that free alternatives exist in virtually every category it competes in, and customers continue to pay regardless. TurboTax makes this point most forcefully. The IRS has maintained free filing options for years, and H&R Block's free tier handles a respectable range of returns, yet TurboTax continues to command premium pricing and the loyalty that goes with it. The reason comes down to three things that users point to repeatedly. Guided prompting that surfaces deductible items they would otherwise overlook, accuracy checks that catch errors before a return is submitted, and direct imports of W-2 and 1099 data that remove manual entry from the equation entirely. Free tools can replicate the price point but not the accumulated experience baked into the product.

QuickBooks operates on an even more entrenched dynamic. With roughly 80% of American small businesses that use financial software already running on QuickBooks, accountants have a strong practical incentive to learn the platform and recommend it to their clients. That creates a two-sided network effect where the value of the software compounds as the number of professionals fluent in it grows, a moat that no newer or cheaper competitor can shortcut without years of patient organic adoption.

The productivity gains attached to the platform are concrete as well, with QuickBooks Online users leveraging AI-powered bank feeds reporting time savings of around 12 hours per month on bookkeeping tasks as of April 2025. For a small business owner with limited hours and real opportunity costs attached to each one, that figure alone makes the subscription an easy decision to justify. On the other hand, Credit Karma operates on a structurally different but equally durable model. Because it generates revenue through recommendations for financial products rather than charging users directly, it is free at the point of consumption while monetizing through lenders and insurers on the other side of the transaction.

The company is also pushing into territory that has the potential to reshape the competitive landscape in adjacent markets. The Intuit Enterprise Suite is an AI native enterprise resource planning platform aimed squarely at mid-market businesses that have grown beyond what QuickBooks alone can accommodate, positioning it as a direct challenger to established players like Oracle (ORCL), NetSuite, and SAP (SAP) in that segment. Alongside this, Intuit has been aggressively promoting what it describes as done-for-you experiences, a model in which AI agents take over processes that have historically required human labor, reducing the burden on business owners and their teams in a meaningful way.

Finally, earlier this year, the company announced a partnership with Anthropic to embed custom AI agents across its full ecosystem, touching TurboTax, QuickBooks, Mailchimp, and Credit Karma. The early results attached to its AI agent deployments are encouraging, with a virtual agent team now serving more than 3 million customers and sustaining repeat engagement rates above 85%. Alongside this, the company has been scaling Intuit Intelligence, a system it describes as fundamentally changing how customers interact with the platform to run and grow their businesses, adding a layer of ambient intelligence that deepens the relationship between the product and the people who depend on it every day.

Analyst Opinions

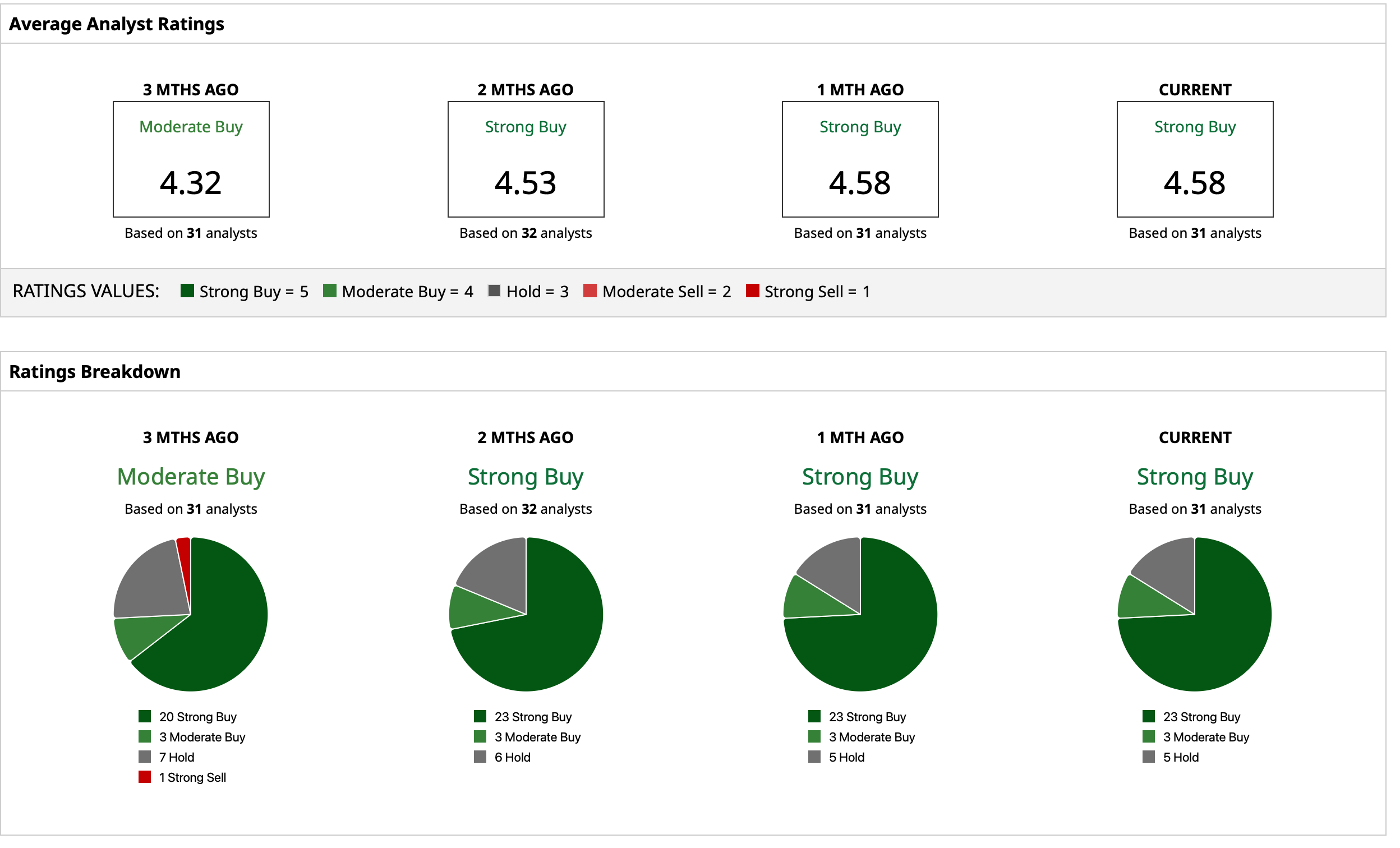

Taking all of this into account, analysts have attributed an overall rating of “Strong Buy” for the stock. The mean target price of $620.87 indicates an upside potential of about 104.7% from current levels. Out of 31 analysts covering the stock, 23 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and five have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

An Apparent Short Squeeze Is Brewing in T1 Energy Stock Intuit Is Slashing More Than 3,000 Jobs. Why Wall Street Is Punishing INTU Stock for the AI Pivot. The Market Is Too Exciting. Protect Yourself with Boring Sysco Stock. Dear Box Stock Fans, Mark Your Calendars for May 26