MP Materials Corp. MP reported an operating loss of $24 million in the first quarter of 2026 compared with the year-ago loss of $34.8 million. Despite this narrower loss, the company extended its streak of operating losses to 11 consecutive quarters, reflecting ongoing margin pressure as it continues transitioning toward higher-value separated rare earth products.

During the quarter, revenues increased strongly 49% year over year, but were outweighed by a sharp rise in costs. Cost of sales climbed 52% due to higher sales volumes of NdPr oxide, metal and magnetic precursor products. Selling, general and administrative expenses (SG&A) rose 39.2% due to increased personnel costs.

Start-up costs surged 503%, reflecting the ramp-up of start-up activities related to magnet production and chlor-alkali facilities. Advanced projects and development expenses spiked 302% due to higher costs incurred for legal, consulting and advisory services to support growth initiatives.

This cost escalation trend has been building as MP accelerated its shift toward separated rare earth production. These products carry higher per-unit costs than rare earth concentrates because of the additional processing involved. Key cost components include chemical reagents, labor, maintenance and other consumables. In 2024, the cost of sales nearly doubled year over year to $192.6 million. In 2025, the cost of sales remained elevated at $192.8 million.

Operating expenses also trended higher. SG&A expenses rose 5% in 2024 and surged a further 35% in 2025, driven by workforce expansion to support downstream growth initiatives. MP Materials thus reported an operating loss of $169 million in 2024 and $149.4 million in 2025.

Looking ahead, MP’s ongoing ramp-up of separated rare earth production at Mountain Pass, along with the expansion of magnetic precursor and magnet output at the Independence Facility, is expected to keep the cost of sales elevated in 2026. Continued investment in downstream capabilities is also likely to sustain high SG&A expenses, maintaining pressure on near-term profitability.

At the same time, NdPr production volumes continue to rise as process optimization and ramp-up efforts progress. Higher output, increased sales volumes and the United States Department of War’s (DoW) Price Protection Agreement will offset some of the margin pressure.

How Are MP’s Peers Faring?

Energy Fuels UUUU reported an operating loss of $16.9 million in the first quarter of 2026 compared with a loss of $26.2 million in the year-ago quarter. Energy Fuels reported a 18.5% rise in its cost of sales. Total operating expenses increased 22.5% year over year to $52.8 million in the quarter, attributed to a 26% surge in exploration, development and processing expenses and 8% increase in standby costs. Energy Fuels has reported an adjusted operating loss in the last eight consecutive quarters.

USA Rare Earth Inc. USAR reported early-stage revenues of $5.7 million in Q1 2026, generated entirely from its Less Common Metals acquisition completed in 2025. It has not yet begun meaningful revenue generation from magnet manufacturing or mineral production. Total operating expenses surged 322% year over year. Selling, general and administrative increased 201%, due to higher legal and consulting costs and increased headcount. Operating loss in the quarter was $36.7 million compared with $8.7 million in the year-ago quarter.

MP’s Price Performance, Valuation & Estimates

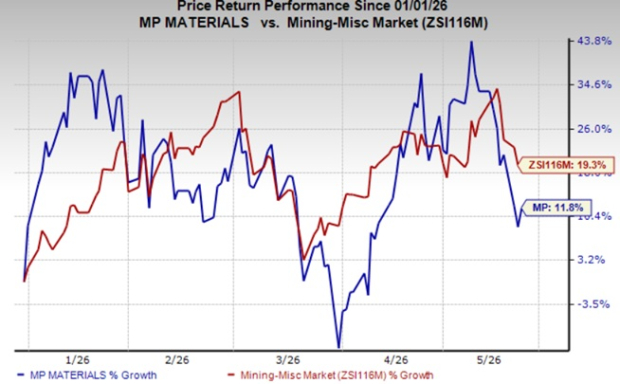

MP Materials’ shares have gained 11.8% in a year compared with the industry’s 19.3% growth.

Image Source: Zacks Investment Research

MP is trading at a forward 12-month price/sales multiple of 17.27X, a significant premium to the industry’s 1.35X.

Image Source: Zacks Investment Research

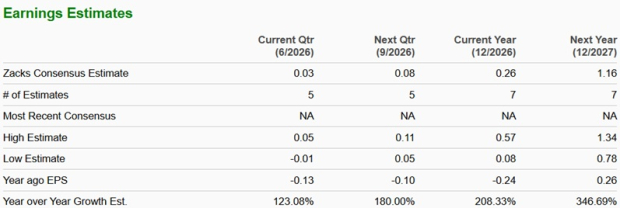

The Zacks Consensus Estimate for MP Materials’ 2026 earnings is pegged at 26 cents per share, indicating a solid improvement from the loss of 24 cents in 2025. The estimate for 2027 is $1.16 per share, indicating a 347% year-over-year improvement.

Image Source: Zacks Investment Research

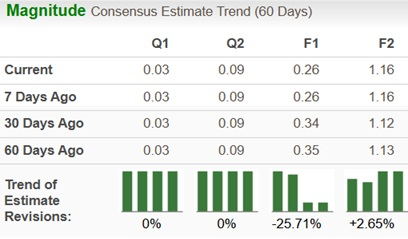

The estimate for 2026 has moved down in the past 60 days, while the same for 2027 has moved up, as shown in the chart below.

Image Source: Zacks Investment Research

The company currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

MP Materials Corp. (MP): Free Stock Analysis Report

Energy Fuels Inc (UUUU): Free Stock Analysis Report

USA Rare Earth Inc. (USAR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).