Few stocks have captured Wall Street’s attention quite like Sandisk Corporation (SNDK). Over the last year, the memory and storage company has delivered an astonishing gain of more than 3,000%, riding the massive wave of spending tied to artificial intelligence (AI) infrastructure. While the company is widely associated with everyday storage products like USB flash drives, memory cards, and portable SSDs, its growth is now driven by modern data centers.

Sandisk has increasingly positioned itself as a key supplier of high-performance memory and storage solutions used inside modern data centers, where the rapid expansion of generative AI applications is driving unprecedented demand for faster and more efficient infrastructure. Additionally, Sandisk has benefited heavily from its specialization in NAND flash technology, which stores information electronically rather than through mechanical spinning disks used in traditional hard drives.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

That makes NAND flash significantly faster, more power-efficient, and better suited for modern AI-driven workloads. The result has been a remarkable surge in investor enthusiasm, pushing SNDK shares sharply higher not only over the past 12 months but throughout 2026 as well. But despite the breathtaking rally, at least some major institutional investors believe the run may still have room to continue.

One of them is Appaloosa Management, the hedge fund established by billionaire investor David Tepper. In its latest 13F filing, Appaloosa disclosed that it opened a new position in Sandisk by purchasing roughly 281,250 shares in the first quarter. The investment serves as a notable endorsement from a high-profile hedge fund manager and could signal growing confidence that further upside remains possible for SNDK shares. With that backdrop, here’s a deeper look at the company.

About Sandisk Stock

Established in 1988 and based in Milpitas, Sandisk Corporation was among the early innovators that helped bring flash memory technology into the mainstream, years before digital storage became an essential part of everyday life. The company gained widespread recognition through products such as USB flash drives, memory cards, and portable SSDs, eventually growing into one of the best-known brands in the global storage market.

In 2016, Sandisk was acquired by Western Digital (WDC) and disappeared from public markets for several years. That changed last year when Western Digital separated its flash storage operations into a standalone public company, bringing back the Sandisk brand along with its original SNDK ticker on the Nasdaq. Today, the company’s reach extends well beyond consumer storage products.

Sandisk now develops NAND flash memory, solid-state drives, and sophisticated storage technologies used in smartphones, personal computers, cloud infrastructure, and AI-driven data centers. With AI fueling an explosion in data generation and computing demand, Sandisk’s fast and power-efficient storage solutions have become increasingly critical to the systems underpinning today’s digital economy.

With a market capitalization of $206.22 billion, Sandisk has emerged as one of Wall Street’s most explosive winners. Over the past 52 weeks, shares of the memory and storage giant have skyrocketed an eye-popping 3,773.7%, leaving the broader S&P 500 Index ($SPX) and its 26.75% gain far behind. The rally has carried into 2026, with SNDK surging another 535%, massively outperforming the broader market’s modest 8.22% return and cementing its status as one of the hottest AI-driven momentum stocks in the market.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Inside Sandisk’s Q3 Earnings Report

Sandisk delivered a blockbuster fiscal third-quarter 2026 earnings report on April 30 that sent shockwaves through Wall Street and sparked an 8.25% single-day rally in the stock. The memory and storage giant didn’t just beat expectations, it completely obliterated them. Sandisk reported non-GAAP earnings per share of $23.41, representing a staggering 278% sequential surge and crushing analysts’ consensus estimate of $14.66.

Even more impressively, the quarter marked a dramatic reversal from the $0.30 per-share loss the company posted in the same period last year, highlighting the enormous operating leverage now emerging within the newly independent business. The top-line performance was equally extraordinary.

Revenue soared a massive 251% year-over-year (YOY) to $5.95 billion, comfortably exceeding both Wall Street expectations by more than 25% and management’s own guidance range. Sequentially, sales nearly doubled from the prior quarter as soaring storage-chip prices and Sandisk’s strategic push toward premium, high-margin enterprise customers continued to supercharge growth.

The standout performer was undoubtedly the company’s Data Center segment, where revenue exploded 233% sequentially and an eye-popping 644.7% YOY to reach $1.467 billion. The surge underscored how aggressively hyperscale and AI-focused customers are ramping up spending on advanced storage infrastructure. At the same time, Sandisk’s Edge segment, which includes storage solutions used in premium smartphones and personal computers, climbed 118.3% sequentially to $3.663 billion, further demonstrating the broad-based strength across the company’s business.

CEO David Goeckeler described the quarter as a major inflection point for Sandisk, noting that the company’s technology leadership is helping drive a strategic shift toward higher-value end markets, particularly within the Data Center business. He also emphasized that Sandisk is transitioning toward a new business model focused on multi-year customer agreements supported by firm financial commitments, a move he believes is creating structurally stronger and more durable earnings power for the company.

Looking ahead, management expects the momentum to continue into fiscal fourth-quarter 2026 results. The company projected revenue in the range of $7.75 billion to $8.25 billion, alongside non-GAAP gross margins between 79% and 81%. Sandisk also forecasts a non-GAAP EPS of $30 to $33, signaling that the AI-driven storage boom may still be in its early innings for the company.

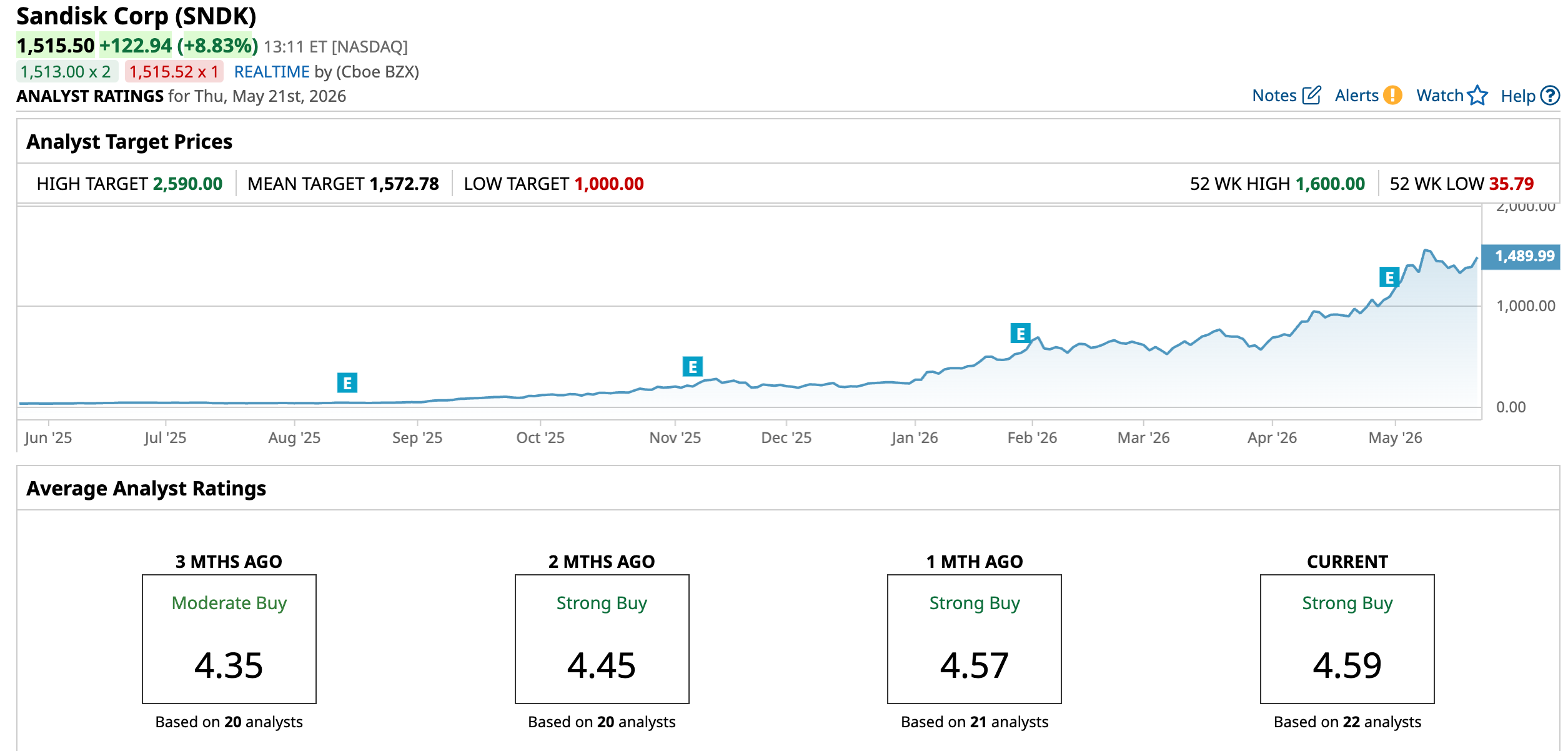

How Are Analysts Viewing Sandisk Stock?

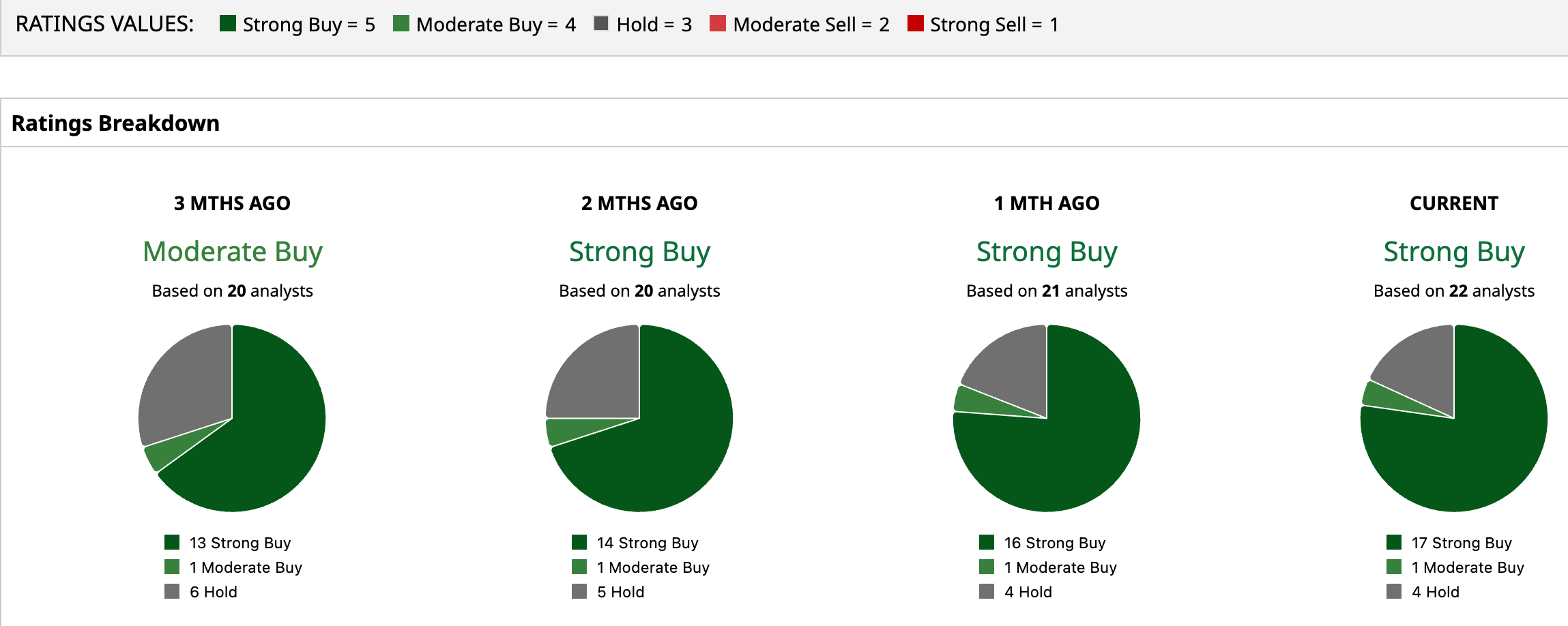

The bullishness surrounding Sandisk extends far beyond billionaire investor David Tepper and Appaloosa Management. Wall Street analysts remain overwhelmingly optimistic on the AI-fueled storage giant, with the stock currently carrying a consensus “Strong Buy” rating. Out of the 22 analysts covering the company, 17 have assigned “Strong Buy” recommendations, one rates it a “Moderate Buy,” and only four remain neutral with “Hold” ratings, a clear sign that confidence in Sandisk’s growth story remains exceptionally strong despite its massive rally.

Analysts also believe the stock may still have meaningful room to run. The average price target of $1,572.78 implies roughly 3.8% upside from current levels, suggesting Wall Street expects the company’s momentum to continue. Even more striking, the Street-high target of $2,590 points to potential upside of as much as 71%, highlighting just how bullish some analysts remain on Sandisk’s ability to capitalize on the surging demand for AI-driven memory and data storage infrastructure.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Sandisk Stock Is Up 535% in 2026. That Didn’t Stop Billionaire David Tepper from Buying 281,250 Shares. Nvidia Delivered a Stellar Quarter. Its Unusual Options Activity Points to 2 Asymmetric Bets on NVDA Stock. An Apparent Short Squeeze Is Brewing in T1 Energy Stock Intuit Is Slashing More Than 3,000 Jobs. Why Wall Street Is Punishing INTU Stock for the AI Pivot.