For decades, investors have treated so-called “safe-haven” stocks like shelter during economic storms. When markets turn volatile, money often flows into companies that sell everyday essentials people simply cannot avoid buying. These businesses may not always deliver explosive growth, but they tend to offer something Wall Street values even more during uncertain times – stability.

That is exactly why Walmart (WMT) has long carried the reputation of being a recession-proof giant. The retail titan caters heavily to lower-income and budget-conscious consumers, selling groceries, household products, and other basic necessities that remain in demand even when the economy weakens. Historically, WMT stock has often outperformed during periods of consumer stress, earning its place as one of Wall Street’s favorite defensive plays.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

But this time, even Walmart is starting to feel the pressure.

As the U.S.-Iran war approaches the end of its third month, concerns are growing that persistently high oil prices could begin weighing more heavily on the U.S. economy by early summer. Evercore ISI strategist Julian Emanuel recently warned that if elevated energy prices persist, the economy could slide toward recession territory by July 4.

That backdrop is now colliding directly with Walmart’s business. The company’s Q1 results highlighted how high gasoline prices are squeezing both consumers and Walmart’s own margins. Management warned that financially stretched shoppers are pulling back, while rising fuel-related costs may eventually force the retailer to raise prices.

Shares of big-box retailer Walmart slipped after its Q1 report, raising fresh questions about whether even America’s classic safe-haven stock can stay insulated from today’s economic pressures. Let’s take a closer look at WMT stock now.

About Walmart Stock

Walmart started as a traditional discount retailer in Arkansas, but today it has grown into one of the world’s largest retail and technology-driven businesses. The company serves nearly 280 million customers every week through more than 10,900 stores and multiple online platforms spread across 19 countries. Walmart built its reputation on low prices and convenience, helping shoppers buy everyday essentials both in stores and online.

Since then, Walmart has steadily expanded far beyond its big-box retail roots. Over the past few years, the company has poured billions into automation, artificial intelligence, faster delivery systems, and digital advertising to modernize its operations and compete in the fast-changing e-commerce world.

For a while, Walmart looked almost unstoppable. Just a couple of months ago, Walmart crossed the $1 trillion market-cap mark, becoming the first major brick-and-mortar retailer to enter a club usually dominated by tech giants. Even now, the company still carries a massive valuation of roughly $958.7 billion.

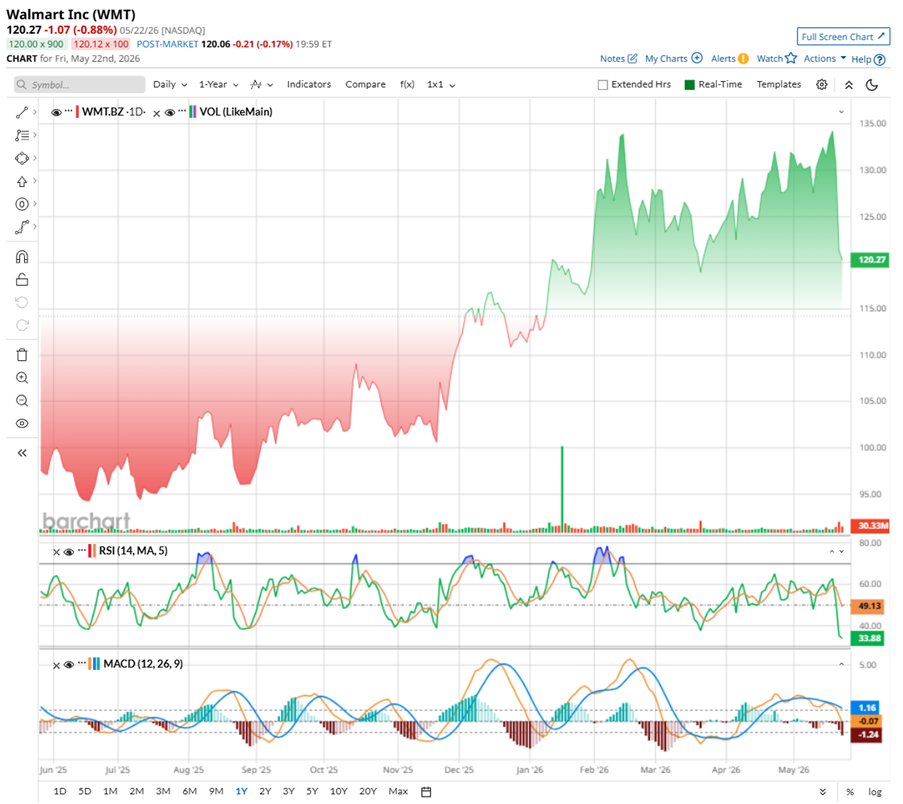

Shares of Walmart have been on a stellar climb this year and in fact, hit an all-time high of $135.16 in May. But the mood shifted quickly after the company’s fiscal Q1 2027 earnings report last week. Investors were disappointed by the management’s cautious outlook around fuel prices and consumer spending, sending the stock down sharply. By the end of the week following earnings, shares had fallen about 8.5%, leaving the stock nearly 11% below its recent peak.

Still, the bigger picture is not entirely negative. Over the past 52 weeks, Walmart’s shares are still up 22.56%, and the stock has gained 5.98% so far in 2026.

From a technical standpoint, though, momentum has clearly cooled. Selling pressure has picked up noticeably after earnings, with rising red volume bars suggesting investors are becoming more defensive. The 14-day RSI has slipped to 31.21, moving close to oversold territory, which signals weakening momentum.

Meanwhile, the MACD indicator has turned bearish after the MACD line crossed below the signal line. Expanding red histogram bars also suggest downside momentum is still building rather than fading.

www.barchart.com

www.barchart.com Even after the recent pullback, WMT stock still looks pretty expensive for a company growing at a relatively slow pace. Priced at 41.57 times forward adjusted earnings and around 1.28 times sales, WMT is trading above sector averages and Walmart’s own historical medians. That rich valuation worked fine when investors saw Walmart as untouchable. But once cracks started showing from fuel costs and margin pressure, the stock quickly lost balance. And honestly, for a business delivering mostly single-digit growth, there may still be more downside ahead.

At least one thing still gives long-term investors some comfort – Walmart remains a reliable dividend machine. The retail giant has raised its dividend for 52 consecutive years, earning its place among the market’s elite Dividend Kings. Walmart currently pays annualized dividends of $0.99 per share through quarterly payouts. The yield sits at a modest 0.82%, so investors are not exactly buying it for huge income, but the consistency still adds a layer of stability during uncertain times.

A Closer Look at Walmart’s Q1 Numbers

When Walmart reported its fiscal 2027 first-quarter results on May 21, the numbers initially looked exactly like what investors expect from a retail giant built for uncertain times. Revenue climbed 7% year-over-year (YOY) to $177.8 billion, while adjusted earnings rose 8.2% annually to $0.66 per share. Both figures topped Wall Street’s expectations, showing that Walmart is still finding ways to grow even as consumers wrestle with inflation and high fuel costs.

A big part of that strength came from Walmart’s rapidly expanding digital business. U.S. sales were powered by accelerating e-commerce demand and the company’s growing use of stores as fulfillment hubs. Store-fulfilled deliveries have more than doubled in the past two years, and over 36% of those orders in Q1 delivered in under three hours. That speed is helping Walmart strengthen its omnichannel strategy while also winning market share in both groceries and general merchandise, particularly among higher-income shoppers.

Globally, e-commerce sales jumped 26% annually, with online operations now making up 23% of total net sales. Walmart’s advertising business also continued booming, rising 37% worldwide and 36% in the U.S., while membership fee income increased 17.4%.

Plus, the company is still spending heavily to fuel future growth. Walmart ended the quarter with $10.7 billion in cash and cash equivalents and $58.1 billion in total debt. Operating cash flow slipped to $4.7 billion, while free cash flow turned negative at -$1.9 billion because of aggressive investments in automation, delivery infrastructure, and omnichannel expansion. Walmart also bought back $2.1 billion worth of shares during the quarter.

Still, the market came away with mixed feelings. On one hand, Walmart continues to pull customers from across income groups with its low-price strategy, fast delivery network, and massive product selection. The company is still gaining market share as shoppers look for value in an expensive economy. But on the other hand, that same affordability-focused model is starting to face serious pressure as inflation stays hot and the conflict in Iran keeps pushing fuel prices higher.

That is why investors were spooked after the report as they focused more on what could come next. WMT stock slipped as management struck a more cautious tone about the months ahead. With climbing gasoline prices, the management warned that shoppers are starting to feel the pressure, raising fresh concerns about the strength of the U.S. consumer.

The company said sales growth for the May-to-July period could slow to around 4% to 5%, while adjusted earnings are expected to land between $0.72 and $0.74 per share. That softer outlook rattled investors who were hoping Walmart’s defensive reputation would fully shield it from the broader economic squeeze.

The mega retailer also maintained its full-year fiscal 2027 guidance, but that outlook itself has already become a source of concern on Wall Street. Annual net sales growth is anticipated to be between 3.5% and 4.5%, alongside adjusted operating income growth of 6% to 8%. Adjusted EPS is still projected in the range of $2.75 to $2.85. The numbers are steady, but in today’s nervous market, “steady” was not enough to calm investors worried about rising living costs and slowing consumer spending.

Analysts tracking Walmart anticipate Q2 2027 revenue to be around 186.7 billion, while adjusted EPS is anticipated to be $0.74, up 8.8% YOY. For fiscal 2027, adjusted EPS is expected to rise 9.5% annually to $2.89, and surge by another 13.5% YOY to 3.28 in fiscal 2028.

What Do Analysts Expect for Walmart Stock?

Even though analysts still see long-term strength in Walmart, rising fuel costs are starting to chip away at profitability expectations. RBC Capital recently trimmed its price target on WMT stock to $137 from $140, while keeping its “Outperform” rating. The brokerage firm pointed to higher transportation and fuel-related expenses that created slightly weaker margin flow-through than expected.

Still, RBC believes Walmart may actually strengthen its competitive position by choosing not to fully pass those higher costs onto shoppers. Keeping prices relatively stable could help Walmart grab even more market share from rivals. The brokerage slightly lifted its Q2 fiscal 2027 net sales growth forecast to 5.3% from 5%, reflecting confidence in Walmart’s ability to keep attracting customers. But RBC lowered its adjusted EPS forecast for the quarter to $0.75 from $0.76. The same trend carries into the longer-term outlook. RBC now expects constant-currency sales growth of 5.3% for fiscal 2027 and 5% for fiscal 2028. However, adjusted EPS forecasts are lowered to $2.92 and $3.27 from earlier estimates.

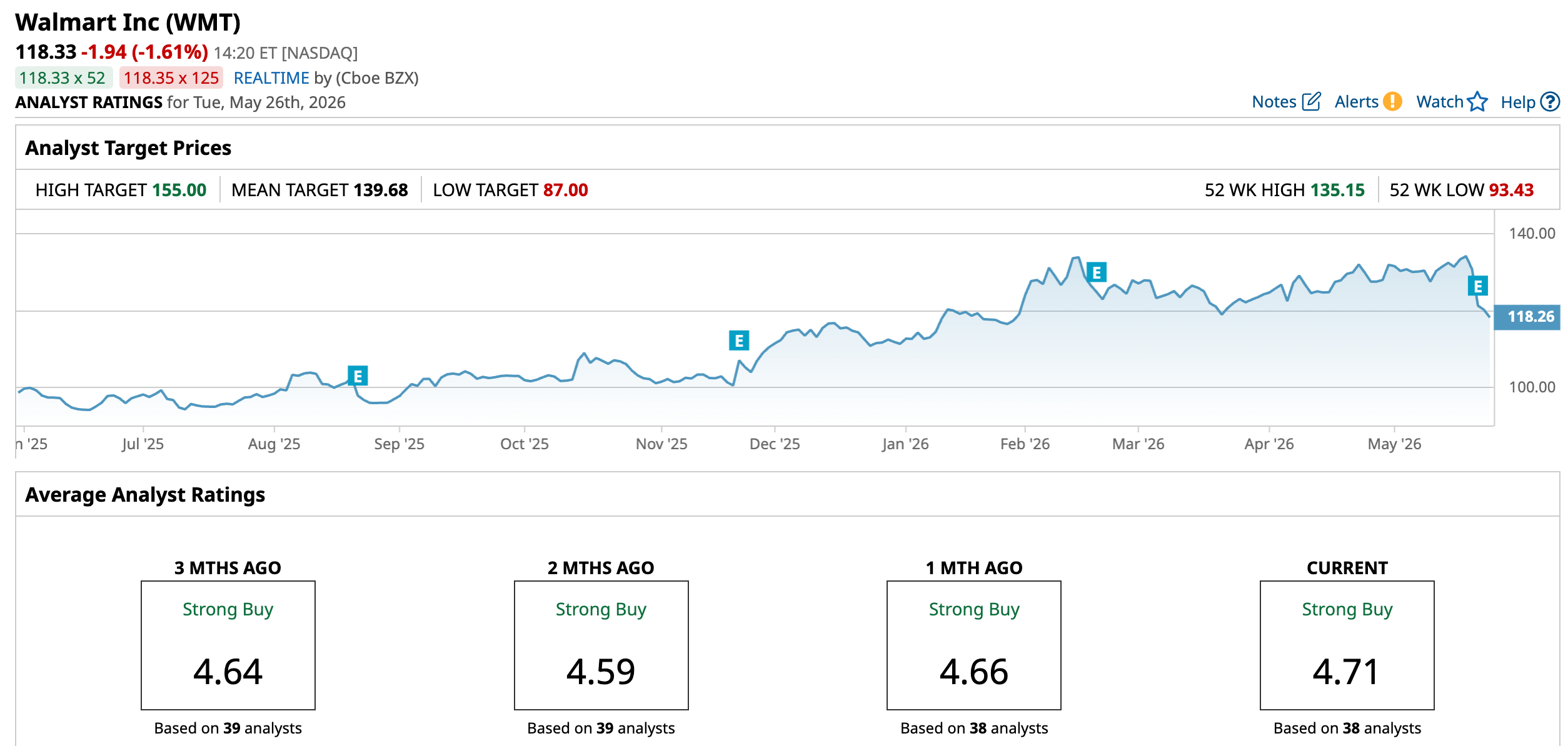

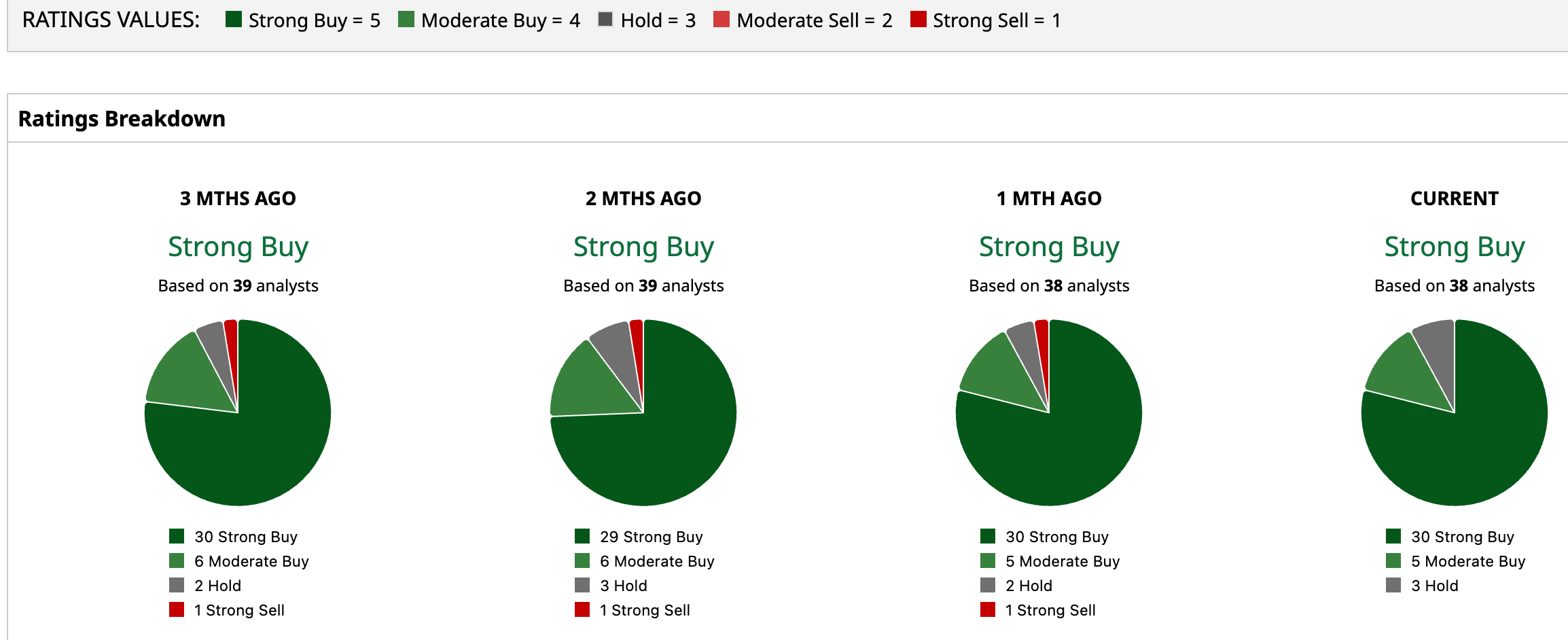

WMT stock has a consensus “Strong Buy” rating overall. Out of 38 analysts covering the quantum computing stock, 30 advise a “Strong Buy,” five recommend a “Moderate Buy,” and the remaining three analysts are playing it safe with a “Hold” rating.

WMT’s mean target price of $139.68 implies potential upside of approximately 18% from current levels. The Street-high target of $155 suggests the stock could rally as much as 31% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Walmart still appears to be in a firm position given all of the economic uncertainty. As fuel prices rise and inflation continues to pressure household budgets, many consumers are becoming even more focused on value, discounts, and convenience. These are all areas in which Walmart has historically thrived. The company is still gaining market share, attracting shoppers across income levels, and benefiting from its massive store network and fast-growing digital business.

But investors are starting to focus less on what Walmart delivered last quarter and more on what could happen next.

Walmart finds itself in a difficult balancing act of protecting low prices to keep customers loyal while also managing higher operating costs. WMT stock may still be one of retail’s safest names, but the road ahead suddenly looks slightly less comfortable than it did a few months ago.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Walmart Is Supposed to Be a Safe-Haven Stock. High Gas Prices Are Hitting Its Shares Instead. Billionaire Dan Loeb Cashed Out of Microsoft Stock. Shares Are Down 14.2% YTD. Nvidia Just Raised Its Dividend by 2,400%. NVDA Stock Is Still a Bet on Growth, Not Income. Short Sellers Aren’t Relenting Against Qualcomm. The Chipmaker Needs to Quickly Deliver on Its AI Pivot for Bulls to Win.