Shares of EMCOR Group, Inc. EME have gained 35.7% in the past six months, underperforming the Zacks Building Products - Heavy Construction industry but outperforming the Construction sector and the S&P 500 Index, as evidenced by the chart below.

EME Stock’s Past 6 Months’ Price Performance

Image Source: Zacks Investment Research

This Connecticut-based infrastructure service provider continues to benefit from favorable trends across several end markets. Strong demand for healthcare and institutional projects, improving activity in warehousing and logistics facilities, and a growing contribution from higher-margin service work are supporting business momentum. At the same time, ongoing investments in workforce development, prefabrication and project execution capabilities are enhancing the company's ability to capitalize on opportunities across complex construction markets. These factors, together with healthy project activity across key end markets, provide support for EMCOR's long-term growth outlook.

Let us take a closer look at the factors shaping EMCOR stock’s prospects.

Record RPOs Enhance EMCOR’s Growth Visibility

Strong project awards across data centers, water and wastewater, healthcare and institutional markets helped EMCOR build a record Remaining Performance Obligations (“RPO”) position. RPOs totaled $15.62 billion at the end of the first quarter of 2026, reflecting a 32.9% increase from the prior-year period and sequential growth from $13.25 billion at year-end 2025.

The increase reflects healthy demand across several end markets, including AI infrastructure, cloud infrastructure and digital transformation projects. Approximately 78% of the current RPO balance is expected to convert into revenues over the next 12 months, providing strong visibility into future business activity. The record backlog position supports EMCOR’s ability to sustain growth across its construction operations.

EMCOR’s Healthcare and Institutional Markets Add Growth Visibility

Beyond data centers, EMCOR is seeing healthy project activity across healthcare and institutional end markets, helping diversify growth sources. Demand for healthcare facility modernization projects and upgraded laboratory space at colleges and universities contributed to project awards during the quarter. Management also indicated that institutional spending has remained more resilient than expected, supporting activity across several regions.

The mechanical construction segment benefited from strong institutional demand, with revenues from the market more than doubling year over year. Healthcare customers are continuing to invest in more flexible and efficient facilities, while universities are increasing spending on research and laboratory infrastructure. The broad-based demand across these sectors provides EMCOR with additional growth opportunities outside its core data center business.

Recovery in Warehousing and Logistics Activity Supports Construction Growth

Improving activity in warehousing, distribution and logistics projects is creating another source of growth for EMCOR’s construction operations. After a period of softness, commercial market demand has started to recover, supporting project volumes across several regions.

Within the mechanical construction segment, commercial revenues increased 33% year over year in the first quarter of 2026, driven largely by warehousing, distribution and logistics projects. The recovery has also supported fire protection activity, where EMCOR continues to expand project opportunities. As customer spending in logistics infrastructure improves, the company is positioned to benefit from additional construction and service work tied to these facilities.

EMCOR’s Productivity Investments Strengthen Execution Capabilities

EMCOR continues to invest in operational capabilities that improve project execution and support long-term growth. The company is expanding workforce training programs, prefabrication capabilities, virtual design technologies and advanced project planning processes to improve efficiency across its construction operations.

The company expects to invest approximately $115 million to $125 million in capital expenditures during 2026, with a significant portion directed toward fabrication facilities and operational capabilities. At the same time, EMCOR continues to expand training programs and leadership development initiatives to support growth. These investments should improve execution efficiency while helping the company capitalize on opportunities across mission-critical construction markets.

Earnings Estimate Revision of EME

EME’s earnings estimates for 2026 and 2027 have moved upward in the past 30 days to $28.84 and $32.21 per share, respectively. The estimates for 2026 and 2027 imply year-over-year growth of 11.5% and 11.7%, respectively.

Image Source: Zacks Investment Research

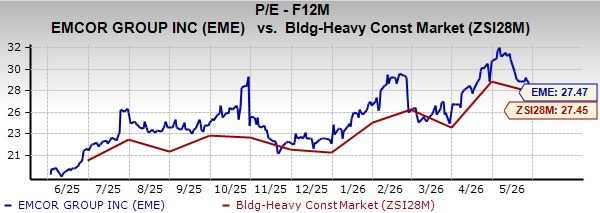

EME’s Premium Valuation

EME stock is currently trading at a premium compared with the industry, with a forward 12-month price-to-earnings (P/E) ratio of 27.47, as evidenced by the chart below.

Image Source: Zacks Investment Research

EMCOR vs. Other Market Players

EMCOR competes closely with Quanta Services, Inc. PWR, Dycom Industries, Inc. DY and MasTec, Inc. MTZ in the infrastructure and engineering construction market.

Quanta operates across electric power transmission, distribution and grid modernization markets, providing the infrastructure needed to support growing electricity demand. Its integrated solutions model, large skilled workforce and deep utility relationships provide a competitive advantage in large-scale power projects tied to grid expansion and data center-related power demand. On the other hand, the company remains heavily exposed to utility capital spending trends and the execution of large transmission programs.

Meanwhile, Dycom is a pure-play digital infrastructure contractor focused on fiber, broadband and communications network deployment. Strong demand for fiber-to-the-home, long-haul fiber routes and data center connectivity continues to support growth opportunities across the communications market. However, Dycom's concentrated exposure to telecommunications infrastructure increases dependence on customer network investment programs and broadband spending cycles.

Conversely, MasTec maintains a diversified infrastructure platform spanning telecommunications, power delivery, clean energy, industrial construction and pipeline markets. This broad exposure allows MasTec to benefit from multiple infrastructure investment themes, including data center development, grid modernization and energy infrastructure expansion. However, participation across several cyclical end markets can create greater earnings variability depending on project timing and execution.

EMCOR’s execution-focused operating model, diversified end-market exposure and balanced project portfolio provide a competitive advantage in terms of stability and demand resilience. However, Quanta’s scale in power infrastructure, Dycom’s communications specialization and MasTec’s diversified infrastructure presence may shape competition as investment in digital and critical infrastructure continues to increase.

How to Play EMCOR Stock?

Expanding opportunities across healthcare, institutional and logistics markets are providing EMCOR with additional avenues for growth beyond its core data center business. Record RPOs, a favorable shift toward higher-margin service work and continued investments in productivity initiatives further support the company's long-term growth prospects.

While the stock trades at a premium valuation relative to many peers, the company's improving earnings outlook, diversified project pipeline and strong execution capabilities help support the premium. Backed by healthy demand trends and solid visibility into future projects, this Zacks Rank #2 (Buy) stock appears well positioned for continued growth. Investors may consider adding EME stock to their portfolios.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Dycom Industries, Inc. (DY): Free Stock Analysis Report

MasTec, Inc. (MTZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).