Houston, Texas-based Waste Management, Inc. (WM) provides environmental solutions to residential, commercial, industrial, and municipal customers. Valued at a market cap of $85.3 billion, the company stands as an industry leader in converting biogenic landfill gases into clean electricity and alternative fuels, which directly power a significant portion of its massive, 26,000-vehicle collection fleet.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and WM fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the waste management industry. The company’s specialty lies in its dominant vertical integration across the entire waste lifecycle, which positions it as one of the largest environmental service providers in North America.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

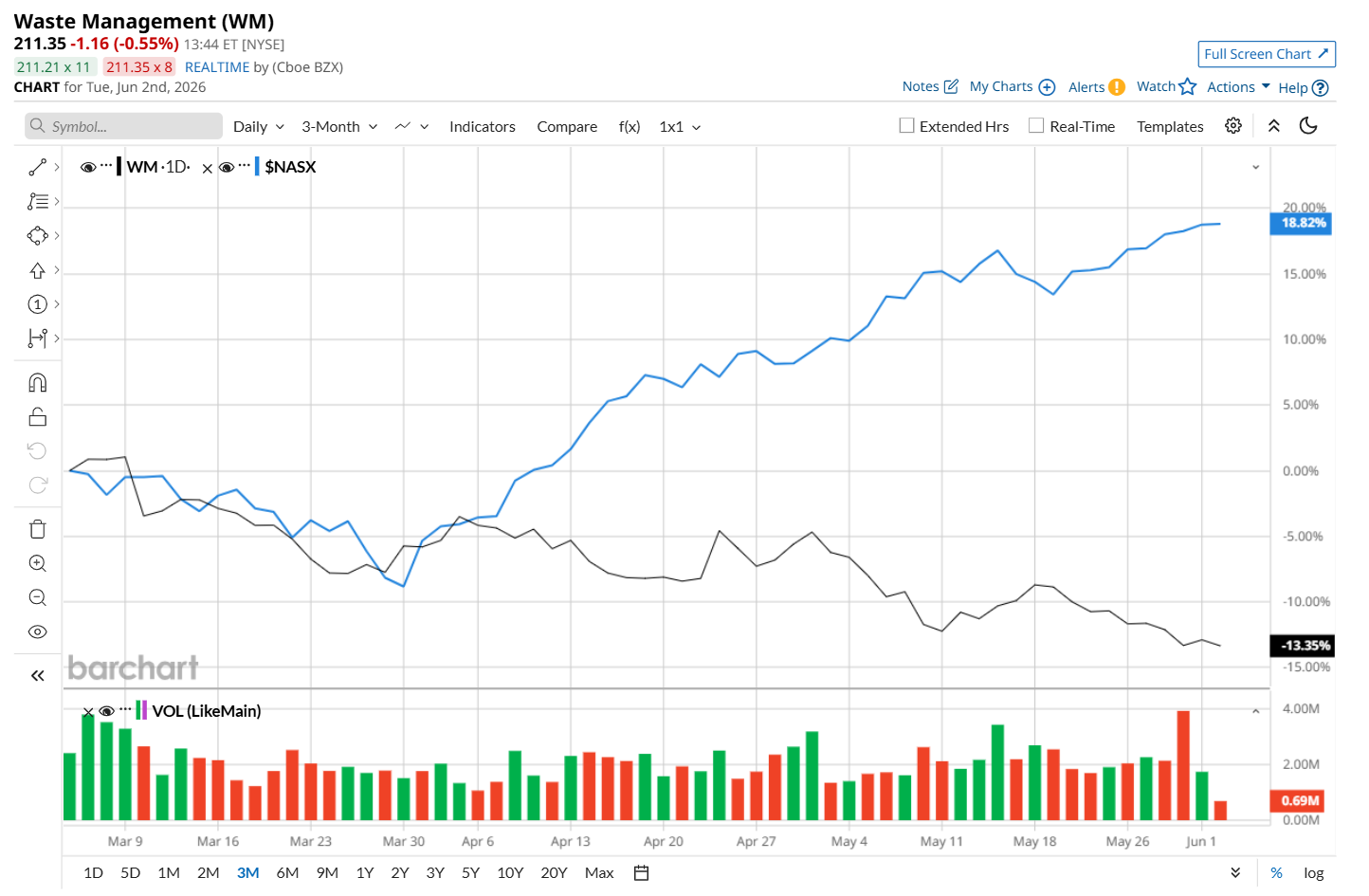

Despite its notable strength, this waste management company has slipped 14.8% from its 52-week high of $248.13, reached on Mar. 6. Moreover, shares of WM have declined 13.1% over the past three months, considerably underperforming the Nasdaq Composite’s ($NASX) 19.3% uptick during the same time frame.

www.barchart.com

www.barchart.com In the longer term, WM has fallen 12.8% over the past 52 weeks, notably lagging NASX's 41% rise over the same time period. Additionally, on a YTD basis, shares of WM are down 3.9%, compared to NASX’s 16.7% gain.

To confirm its bearish trend, WM has been trading below its 200-day moving average since early May and has remained below its 50-day moving average since early April.

www.barchart.com

www.barchart.com On Apr. 28, Waste Management reported its Q1 2026 results, and its shares gained 1.3% in the following trading session. Its revenue rose 3.5% year over year to $6.23 billion, while its adjusted EPS increased 8.4% from the year-ago quarter to $1.81, surpassing analyst expectations of $1.75. Adjusted operating EBITDA grew 5.9% to $1.85 billion, with margins expanding 70 basis points to 29.8%. Growth was primarily driven by the company’s core Collection and Disposal segment, which benefited from strong pricing execution and favorable price-to-cost spreads.

In the competitive arena of waste management, WM has outpaced its rival, Republic Services, Inc. (RSG), which declined 22.5% over the past 52 weeks and 5.6% on a YTD basis.

Despite WM’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 28 analysts covering it, and the mean price target of $257.64 suggests a 22% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Even If Eli Lilly Stock Continues to Shine, Stay Away from This Pharmaceutical ETF Micron Stock Could Still Have Nearly 70% Upside Potential Left in Its Tank Nvidia Launches AI Chip for Laptops. Count NVDA Stock Out at Your Own Peril. Greg Abel's Big Bet: Berkshire to Buy Taylor Morrison Homes in $6.8 Billion Deal