Ulta Beauty, Inc. ULTA used its first-quarter call to make a broader point than the headline beat. Management argued the business is gaining traction across channels, categories and newer growth vehicles while keeping a tighter grip on profitability.

That message mattered because the company left its sales outlook unchanged in a tougher consumer backdrop, while still lifting profit and EPS expectations for fiscal 2026.

ULTA Builds on a Strong Core

President and CEO Kecia Steelman said the U.S. business remains fundamentally strong, with growth supported by stores, e-commerce and major product categories.

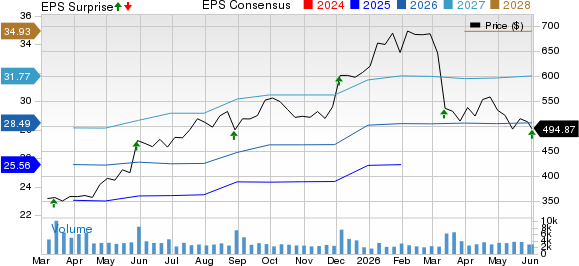

Net sales rose 11.1% to $3.16 billion, surpassing the consensus estimate by 1.64%. Adjusted earnings per share of $7.74 topped the Zacks Consensus Estimate of $6.90 by 12.2%.

Comparable sales increased 5.3%, driven by a 3.7% increase in average ticket and a 1.6% gain in transactions. Steelman said performance was broad-based, with prestige share gains and roughly flat share in mass beauty.

Management also pointed to digital momentum. E-commerce posted mid-teen sales growth, helped by same-day delivery expansion, Klarna buy now, pay later options and buy online, pick up in store capabilities.

Ulta Beauty Inc. Price, Consensus and EPS Surprise

Ulta Beauty Inc. price-consensus-eps-surprise-chart | Ulta Beauty Inc. Quote

Ulta Beauty Expands Beyond the Core

Steelman spent meaningful time on growth initiatives that extend beyond the legacy U.S. beauty model. Space NK continued to post healthy growth, while Ulta added stores in Mexico and opened a third Middle East location through franchise partner Alshaya.

The company also highlighted marketplace, wellness and media as incremental growth drivers. Marketplace ended the quarter with more than 325 brands and over 8,000 SKUs, while wellness benefited from assortment expansion in supplements, self-care and intimate care.

Social commerce emerged as another priority. Steelman said TikTok Shop is being used less as a pure sales channel and more as a customer acquisition and brand-building tool, especially for younger shoppers and Ulta’s exclusive brands

ULTA Finds Profit Levers in the Model

Chief financial officer Chris DelOrefice framed the quarter as proof that Ulta can drive profitable growth, not just sales growth. Gross margin expanded 100 basis points to 40.1%, helped by lower inventory shrink and better merchandise margin.

Shrink improvement stood out as a recurring theme. DelOrefice said targeted actions in higher-risk stores, better processes and training, and data-driven execution produced shrink reductions across every category and region.

Those gains helped offset higher fuel-related transportation costs and a 14.6% increase in SG&A expense.Management tied the expense growth mainly to Space NK and investments already underway in the Ulta Beauty Unleashed strategy.

Ulta Beauty Keeps Sales View Intact

Despite the strong quarter, management did not raise its top-line outlook. Ulta still expects fiscal 2026 net sales growth of 6% to 7% and comparable sales growth of 2.5% to 3.5%.

What did change was the profit outlook. Operating income growth guidance moved to 6.5% to 9% from 6% to 9%, and EPS guidance increased to $28.36 to $28.80 from $28.05 to $28.55.

DelOrefice said the company is taking a measured stance because of macro uncertainty, even as first-quarter execution came in strong. He added that Ulta expects stronger sales growth in the first half, aided by Space NK and a tougher comparison base later in the year.

ULTA Faces Questions on Traffic and Competition

Analysts repeatedly pressed management on the cadence of comparable sales, traffic and the competitive backdrop. Steelman said February benefited from lapping a weak comparison, while March and April comps were in the low single digits, largely in line with expectations.

Questions also centered on whether the beauty category is getting more promotional and whether Ulta needs extra investment to protect its share.

Steelman responded that beauty remains competitive, but said exclusivity, brand building and the company’s mass-to-luxury assortment remain clear differentiators.

On traffic, management emphasized marketing, events, loyalty and personalization rather than a broad pricing response. The company’s loyalty base reached nearly 47 million members, up 4% year over year, which executives described as a major advantage in targeted engagement.

Ulta Beauty Puts Cash Behind the Plan

Capital allocation was another key message on the call. Ulta repurchased 958,323 shares for $555 million in the quarter and ended May with $1.3 billion still available under its authorization.

DelOrefice said the company now plans to buy back $1.5 billion of stock in fiscal 2026, up from the prior $1 billion target. He said management views the current environment as an attractive opportunity to deploy capital while still funding growth.

The company also continued investing in stores and infrastructure. Ulta opened 16 net new U.S. stores and one Space NK location in the quarter, and it is planning a highly experiential Times Square flagship for late 2027.

ULTA Stays Focused on Share and Discipline

The tone coming out of the call was confident but controlled. Steelman consistently returned to the idea that Ulta can still gain share while staying disciplined on costs and selective on where it invests.

That balance now looks central to the 2026 story. Management is pushing digital, international, marketplace, wellness and AI initiatives, but it is also signaling that margin protection and earnings growth matter just as much as top-line expansion.

Zacks Signals Favor Growth, But Rank Stays Neutral

ULTA carries a Zacks Rank #3 (Hold), along with a Growth Score of A, Momentum Score of B, Value Score of C and VGM Score of A. That combination points to favorable growth and blended style characteristics, even if the rank itself is not in the most bullish tier. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores are designed to complement the Zacks Rank, not override it. A Zacks Rank #3 can still support a neutral stance, while the strong Growth and VGM grades indicate better underlying style characteristics than the rank alone. That said, the Zacks Rank can change as earnings estimate revisions move in the wake of quarterly results.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ulta Beauty Inc. (ULTA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).