The word “bottleneck” is now familiar to all retail investors. First, it was the GPU bottleneck that caused Nvidia's (NVDA) stock to skyrocket. Then came the energy bottleneck. Causing nuclear energy stocks like Constellation Energy (CEG) and Vistra Corp (VST) to grow manifold. The market then moved on to memory makers as the next bottleneck, and it is anybody’s guess when that will be resolved. Micron (MU) and SanDisk (SNDK) continue to nudge up every day, with some analysts still expecting them to double from here.

The memory bottleneck isn’t a tough nut to crack. Sooner or later, someone is going to come up with a better technology or an alternate technology that could significantly reduce the need for high-bandwidth memory. What can’t be resolved so easily, however, is the power bottleneck.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

It can take years to bring a new power source online and connect it to the grid. Of all the bottlenecks, this is likely to stay a bottleneck for some years to come. For now, companies have to do what’s needed at their end, i.e., optimize power management within the data center, and that’s where a company like Texas Instruments (TXN) shines.

While energy companies solve the power bottleneck from the outside, TXN does so from the inside. It doesn’t get the same hype, though, but that could be because analysts covering the stock see it as a semiconductor company first, and they’re not wrong, as that is what the company does. At some point in the future, analysts are going to wake up to TXN's unique position, and understanding how that could happen is essential for today’s investor.

Where Does Texas Instruments Fit in the Power Bottleneck Picture?

As rack densities rise, companies need to manage the immense power these racks consume. The move from air cooling to liquid cooling has mitigated a part of the problem, but the analog layer that helps convert, regulate, and distribute power has become exponentially more complex. This complexity is where Texas Instruments comes in. The company makes the analog parts that help thermal sensors and power management ICs, among others, work with the rest of the rack. TXN’s wide range of general-purpose analog products makes it the right vendor to deal with when it comes to data centers, and that is where the company’s growth is coming from.

In the first quarter alone, the company saw its data center revenue as a percentage of total revenue nearly double. This confirms how modern data centers are increasingly relying on TXN for their power management needs. At the same time, this is also resolving an issue that has plagued the company for some years now. Texas Instruments was considered a heavily cyclical company, since its products were mainly used in cyclical sectors like automotive and consumer electronics. The data center opportunity and the power bottleneck now allow the company to shed that baggage and take its fair share of business coming from the AI boom.

One could argue that the firm already has significant inventory to deal with, but at the same time, its fab utilization rates are climbing. This is the same capacity that the firm was criticized for in the past, but the fact that utilization is rising bodes extremely well for the company. This points to a sustained high utilization, resulting in higher visibility into future demand and earnings, helping the company shed the cyclical label.

About Texas Instruments Stock

Texas Instruments Inc. is a global semiconductor company that manufactures, designs, and sells semiconductor products to electronics manufacturers and designers. The company operates through two business segments: Embedded Processing and Analog. Its product portfolio includes power management solutions, processors, microcontrollers, signal processing components, wireless connectivity, and radar technologies.

Over the past year, the stock remained relatively stable for most of the period before rising sharply in recent months. It delivered returns of around 65%, while the iShares Semiconductor ETF gained about 173% during the same time period. This indicates that although the semiconductor industry delivered strong returns, the stock’s gains fell short of the broader sector’s performance.

www.barchart.com

www.barchart.comThe improving stock prospects are now resulting in a high valuation, but the valuation is fully justified as long as investors believe the demand will stay. TXN is expected to grow its earnings at 40% this year, and that is reflected in the TXN stock’s performance as well. Over the next three years, the consensus earnings growth rate of around 25% is not bad, and for a company that could potentially solve the power bottleneck, the estimates could be very conservative.

Texas Instruments Improves Gross Margins

Texas Instruments reported its first-quarter fiscal 2026 earnings on April 22. During the quarter, the company generated $4.8 billion in revenue and $2.8 billion in gross profit. Gross margin improved to 58%, increasing 210 basis points from the previous quarter. Operating profit came in at $1.8 billion, representing 37% of revenue, while operating expenses reached $974 million. The company generated $1.5 billion in operating cash flow and invested $676 million in capital expenditures.

For the second quarter, revenue is expected to range from $5 billion to $5.4 billion. On the earnings side, the company guided EPS in the range of $1.77 to $2.05. The effective tax rate is projected to be around 13%. Despite strong demand signals, management remained cautious, noting an uneven recovery in 2025.

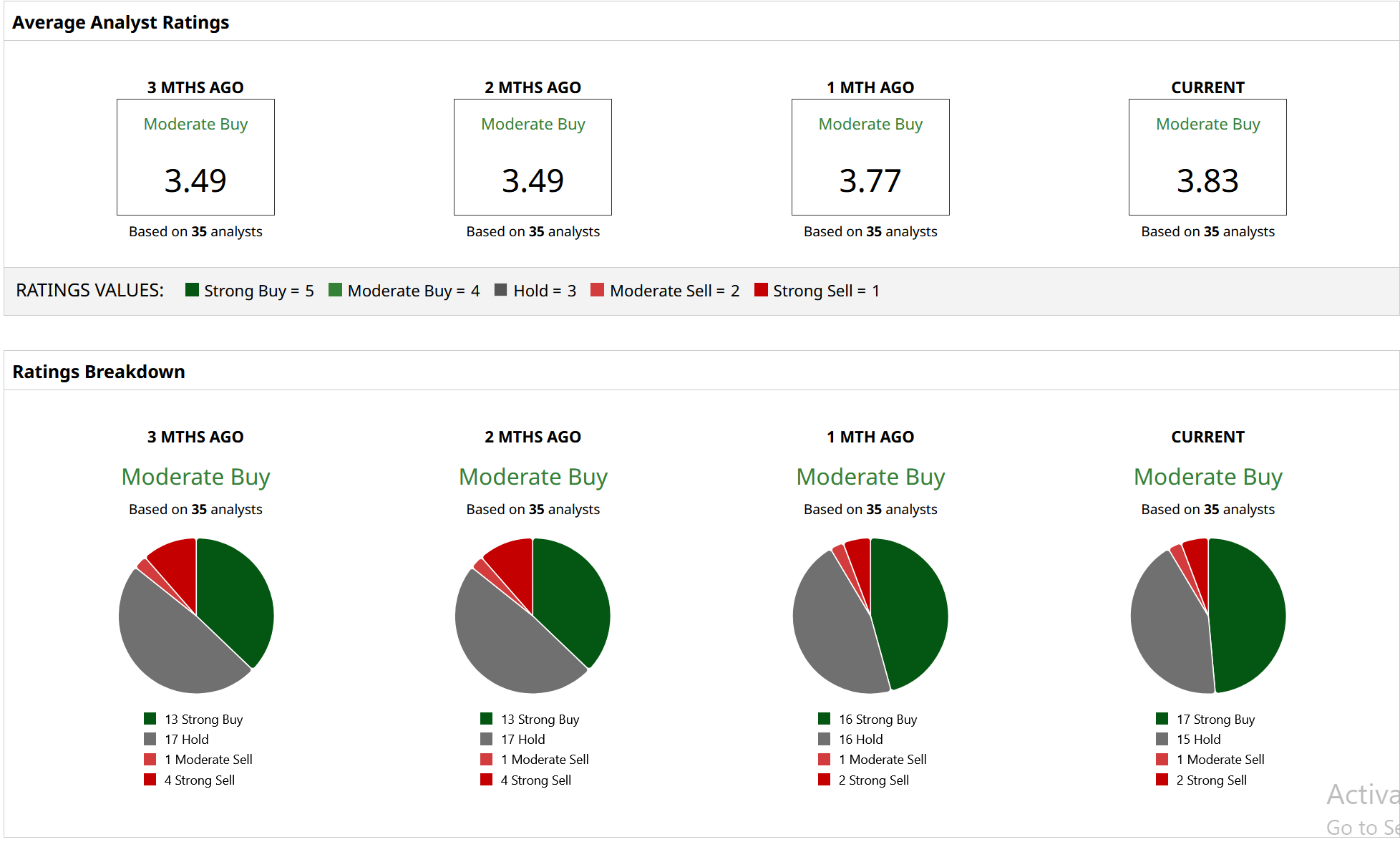

What Are Analysts Saying About Texas Instruments Stock?

Most analysts have revised their price targets upward post-earnings report. Seaport Research’s analyst Jay Goldberg was among them and now has the highest price target of $400 on the stock, implying about 30% upside. On May 25, Bank of America Securities’ analyst Vivek Arya also provided a boost to the stock by revising his price target up from $320 to $370. He is also of the view that the company’s role in power management is underappreciated and that its core markets in automotive and industrial sectors are finally seeing cyclical tailwinds. This opportunity, along with the AI data center growth, makes the stock a “Buy” at this point.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Texas Instruments Is a Major Winner of the AI Power Bottleneck, Investors Just Aren’t Seeing It Yet Dell’s Bull Rally Will Continue. Don’t Fall Into the Trap of Thinking It’s Just a Low-Margin Hardware Assembler. A $2 Billion Reason to Buy Little-Known Gorilla Technology Stock Right Now Cadence Design Is Cementing Its Place in the 2nm AI Chip Race By Solving the Die Size Limit in Partnership With a Major Chipmaker