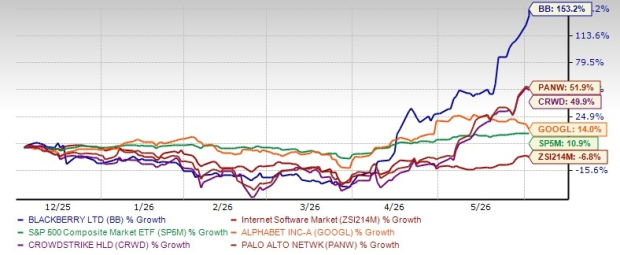

BlackBerry Limited’s BB shares have rallied 153.2% in the past six months, outperforming the Computer Software industry (down 6.8%) and the S&P 500 composite (rise of 10.9%). Yesterday, BB stock gained 6.2% and closed at $10.32, after hitting a fresh 52-week high of $10.33.

Price Performance

Image Source: Zacks Investment Research

Once known for smartphones, BB has pivoted to a software-centric business focused on automotive operating systems and secure communications.

This sharp rally reflects increasing investor confidence in the company’s turnaround story and improving fundamentals.

But the question now is: Does BB’s rally still have room to run, or is most of the upside already priced in?

Let’s explore the catalysts behind the surge and assess whether you should double down or stay on the sidelines.

BB: Turnaround Story Turning Into a Growth Narrative

BlackBerry has been undergoing a turnaround for some time now. On the last earnings call, management emphasized that the turnaround is complete, highlighting eight consecutive quarters of improving GAAP profitability and consistent execution across the business. This was reiterated by CFO Tim Foote at the Baird Global Consumer, Technology & Services Conference yesterday. Foote re-emphasized that “BlackBerry is now a growth company”, sending the stock surging yesterday.

The company delivered a strong finish to fiscal 2026, with fourth-quarter revenues growing 10% year over year and adjusted gross margin expanding to more than 78.2%. Adjusted EBITDA expanded 71% year over year to $36.1 million. Fiscal 2026 revenues of $549.1 million were up 3% year over year. Adjusted EBITDA of $107.1 million surged 27% year over year.

The company also demonstrated solid cash generation, producing meaningful operating cash flow. For the quarter that ended on Feb. 28, 2026, BlackBerry generated $45.6 million of net cash from operating activities and free cash flow of $44.4 million.

QNX: Driving Long-Term Upside

At the center of BlackBerry’s growth story is the QNX division. QNX is a Real-Time Operating System for embedded systems widely used in automotive and is now gaining traction in physical AI, medical, robotics, industrial and emerging markets.

QNX delivered record quarterly revenues of $78.7 million, up 20% year over year. Record royalties and development revenues were the key catalysts. It has also achieved the “Rule of 40”.

QNX’s royalty backlog reached roughly $950 million, offering clear visibility into sustained, multi-year growth. The growing relevance of software-defined vehicles is fueling QNX’s momentum.

BlackBerry Limited Price, Consensus and EPS Surprise

BlackBerry Limited price-consensus-eps-surprise-chart | BlackBerry Limited Quote

Apart from automotive, strengthening positioning within the general embedded markets (“GEM”) is a strong tailwind. About 20% of QNX revenues now come from non-automotive segments, where the market opportunity may exceed auto, added Blackberry. Robotics is a key long-term opportunity for BlackBerry as it taps into the rise of physical AI. With growing pipeline momentum, the company expects this segment to become a meaningful driver of GEM growth.

Management highlighted partnerships with major chipmakers such as NVIDIA and Qualcomm, underscoring QNX’s role as a foundational software layer in next-generation intelligent systems. The upcoming launch of the Alloy Kore platform, which moves BlackBerry up the software stack into middleware, could significantly increase average selling prices and deepen customer relationships.

Secure Comms: Inflects to Growth

The Secure Communications business is showing signs of resurgence, delivering 8% year-over-year growth in the fiscal fourth quarter and approaching “Rule of 40” performance. Annual recurring revenues rose 1% sequentially to $218 million, up 5% year over year, while DBNRR improved to 94%, gaining 2 points sequentially.

Rising NATO and global defense spending is driving strong momentum in BlackBerry’s Secure Communications unit. Secusmart, its military-grade encrypted platform, posted solid year-over-year growth, led by demand from the German government, where it meets strict BSI standards.

The growth is also fueled by a powerful macro trend — digital sovereignty. Governments and enterprises increasingly demand secure, sovereign communication systems that protect sensitive data from foreign access. A major validation came from the Government of Canada expanding its partnership and increasing adoption of BlackBerry’s Secusmart licenses across federal agencies. This deal is expected to drive a strong start to fiscal 2027 with meaningful revenue contributions.

Recently, BB’s AtHoc just secured FedRAMP High re-certification for 2026. AtHoc is already trusted by 80% of U.S. federal agencies, law enforcement, defense organizations, emergency services and critical infrastructure operators. It remains the only CEM platform to hit this bar recently.

Guidance Points to Continued Momentum

BlackBerry expects fiscal 2027 revenues to grow 6-11% to $584-$611 million, with adjusted EBITDA of $110-$130 million and non-GAAP EPS rising to 15-19 cents, excluding any potential share repurchases. Stronger cash conversion is expected to drive full-year operating cash flow to approximately $100 million, nearly doubling year over year.

It expects Secure Communications to return to full-year growth for the first time in six years, marking a crucial inflection point. Fiscal 2027 revenues are projected to grow 4-8% to $270-$280 million, with adjusted EBITDA forecasted at $57-$65 million.

BlackBerry’s licensing business remains a stable source of cash flow and profitability, with revenues of about $24 million.

For fiscal 2027, BlackBerry expects QNX revenues of $290-$307 million, with the higher end implying nearly 15% growth and serving as its target. However, due to macroeconomic uncertainty, it has included some downside risk to the lower end of the range.

Image Source: Zacks Investment Research

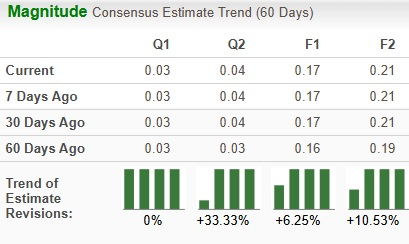

Analysts have revised their estimates up for both fiscal 2027 and 2028 over the past 60 days.

No Case Is Without Risks

While the long-term story is improving, the near-term setup is not without challenges. QNX backlog (about $950 million) looks impressive, but there’s a catch. Management noted that revenues from design wins typically materialize two to three years later, implying that while growth visibility is solid, near-term financial performance may not fully reflect that strength. This could potentially result in mismatches between expectations and reported results.

In addition, some of BlackBerry’s most exciting opportunities, such as physical AI, robotics and the Alloy Kore platform, remain in the early stages, introducing execution risk. Heavy reliance on the automotive industry is a concern. QNX platform remains heavily exposed to vehicle production cycles and OEM spending, which in turn are heavily dependent on macro conditions. BlackBerry faces increasing competitive pressures in both QNX and cybersecurity businesses.

Within QNX, it faces Wind River (VxWorks) and Alphabet’s GOOGL Android Automotive OS. The cybersecurity business is pitted against CrowdStrike CRWD, Palo Alto Networks PANW and a host of other cybersecurity companies.

What to Make of BB’s Premium Valuation?

In terms of the forward 12-month price/sales ratio, BB is trading at 9.9X, higher than the Internet-Software sector’s multiple of 4X.

Image Source: Zacks Investment Research

The premium appears justified given the company’s improving fundamentals and long-term growth prospects.

In comparison, GOOGL trades at a forward 12-month P/S multiple of 9.54, while CRWD and PANW are trading at multiples of 30.79 and 18.42, respectively.

Shares of GOOGL, CRWD and PANW have gained 14%, 49.9% and 51.9%, respectively, over the past six months.

Here’s Why BB Is Still a Buy

BB currently carries a Zacks Rank #2 (Buy).

Strong QNX momentum, emerging opportunities in the GEM space and a resurgent Secure Communications segment all point to meaningful long-term potential.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

BlackBerry Limited (BB): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).