Palantir Technologies (PLTR) fell out of favor with investors in 2026. Shares of the AI-focused software company are down 19.16% year-to-date (YTD), significantly underperforming the S&P 500 Index ($SPX), which has gained 10.54% during the same period. The stock also remains roughly 31.17% below its 52-week high of $207.52.

The pullback marks a notable shift in sentiment toward one of the market's most prominent AI stocks. While Palantir delivered strong gains in recent years as enthusiasm around AI accelerated, investors have become increasingly cautious amid concerns about valuation and intensifying competition.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Palantir continues to benefit from growing demand for its AI-powered software platforms across both government and commercial customers. However, its extremely high valuation weighed on its share price.

At the same time, the competitive landscape is evolving rapidly. Emerging AI leaders, including Anthropic and other rivals, are introducing increasingly sophisticated models and enterprise solutions. As competition expands, concerns arise about whether software providers can maintain their competitive advantages, pricing power, and growth rates over the long term.

With Palantir trading well below its recent highs, is the pullback an attractive entry point? Let's examine the factors that could determine whether Palantir is worth an investment.

www.barchart.com

www.barchart.com Palantir Maintains Its Explosive Growth Rate

Despite lagging the broader market in recent months, Palantir continues to deliver one of the fastest growth rates in the software industry. Thanks to the significant demand for its Artificial Intelligence Platform (AIP), the company just posted another solid quarterly performance.

Notably, Palantir’s revenue grew 85% year-over-year (YOY) and 16% sequentially, marking Palantir's eleventh consecutive quarter of accelerating growth. The performance was strong enough for management to significantly raise its full-year outlook, signaling confidence that customer demand remains robust.

The company's momentum is being driven primarily by the U.S., where adoption of its AI solutions continues to expand across both enterprises and government agencies. U.S. revenue surged 104% YOY and 19% from the prior quarter. Meanwhile, Palantir's customer base climbed 31% to 1,007 organizations, highlighting that growth is coming from both new clients and existing customers spending more.

Importantly, revenue generated from Palantir's top 20 customers rose 55% YOY to an average of $108 million per customer on a trailing twelve-month basis. This suggests that once organizations adopt Palantir's platform, they often expand their usage over time.

The commercial business remains a standout. U.S. commercial revenue jumped 133% YOY to $595 million, demonstrating strong enterprise demand for operational AI applications. Government customers continue to be a major growth driver, with U.S. government revenue climbing 84% to $687 million amid contract renewals and new program wins.

Additional indicators point to sustained momentum ahead. Net dollar retention reached 150%, meaning existing customers are increasing their spending. At the same time, total contract value bookings surged 135% YOY, providing greater visibility into future revenue growth.

Further, management's updated outlook suggests the acceleration is far from over. Palantir now expects approximately $7.66 billion in revenue for 2026, up from its previous forecast of $7.19 billion and implying roughly 71% annual growth. The company also raised its U.S. commercial revenue forecast to more than $3.22 billion, representing at least 120% growth.

Profitability is expanding alongside revenue. Palantir now projects adjusted operating income of $4.44 billion to $4.45 billion and adjusted free cash flow of $4.2 billion to $4.4 billion, indicating that its AI-driven growth is translating into substantial cash generation.

Should You Buy, Sell, or Hold Palantir Stock?

Palantir continues to deliver impressive growth, driven by strong demand for its AI platform, an expanding customer base, and increasing spending from existing clients. The company’s recent guidance upgrade further suggests its momentum remains intact, supporting its premium valuation.

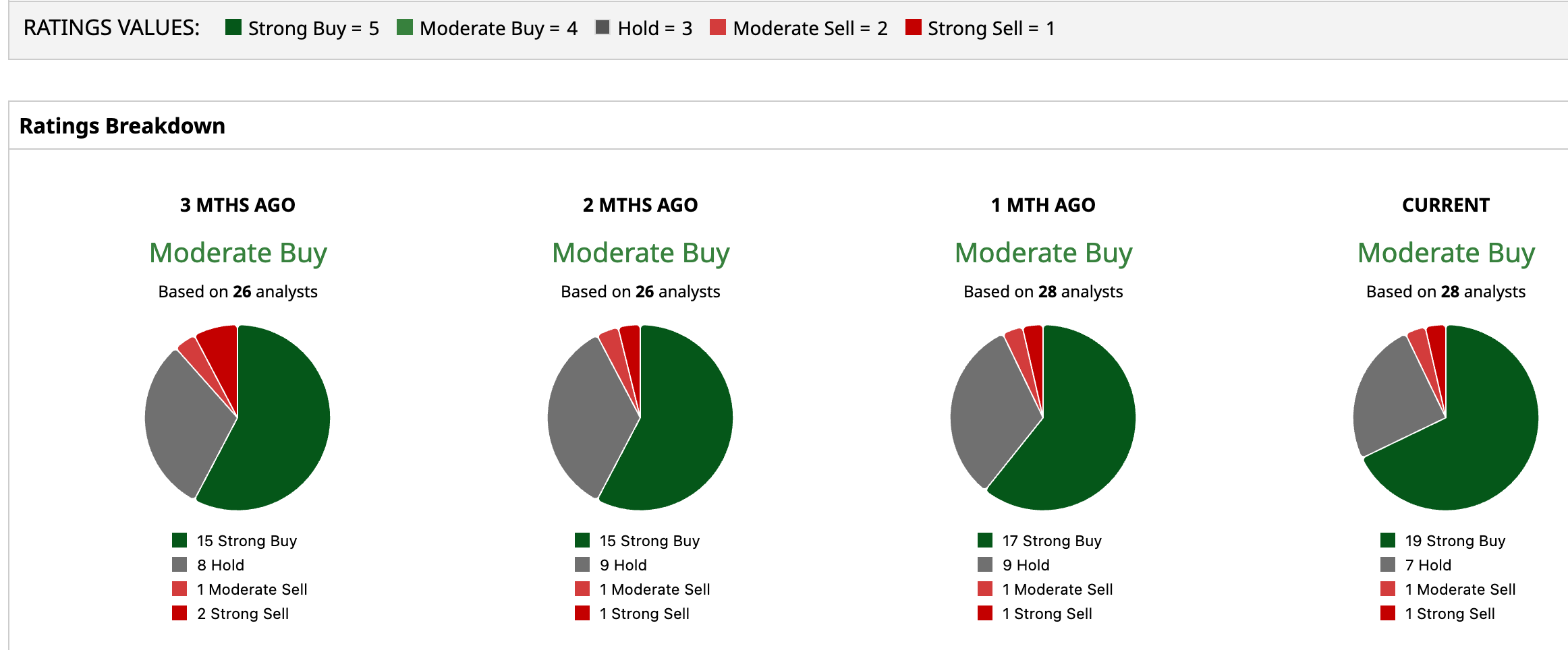

For long-term investors, the pullback in PLTR stock is a buying opportunity. At the same time, Wall Street analysts maintain a “Moderate Buy” consensus rating.

Regardless, investors should keep valuation concerns in mind. Palantir shares trade at elevated multiples compared to many peers, which could lead to heightened volatility in its stock price.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Is Cheering Broadcom Stock. It Wants to Supercharge the Smart Home Industry. Palantir Lags the S&P 500 in 2026. How to Play the Once-Leading AI Stock Now. Apple Was Warren Buffett’s Best Investment. GOOGL Stock Could Be Greg Abel’s Claim to Fame. ARM Stock Is Supercharging Its Path to $15 Billion in Chip Sales