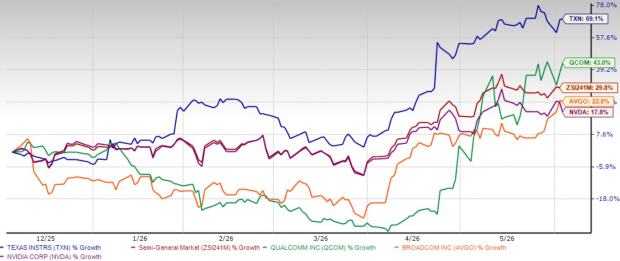

Texas Instruments Incorporated TXN has been one of the strongest performers in the semiconductor industry lately, supported by solid financial execution, growing demand for its analog and embedded chips and increasing exposure to artificial intelligence (AI)-related opportunities. Over the past six months, TXN shares have surged 69.1%, significantly outperforming the broader Zacks Semiconductor – General industry’s 29.8% gain. This impressive rally has established Texas Instruments as one of the standout names in the chip sector.

The stock has also delivered stronger returns than several major semiconductor peers, including QUALCOMM Incorporated QCOM, Broadcom Inc. AVGO and NVIDIA Corporation NVDA. Over the past six months, shares of QUALCOMM, Broadcom and NVIDIA have risen 43%, 22.8% and 17.8%, respectively.

Texas Instruments is benefiting from the ongoing AI boom, even though it does not manufacture high-end AI processors. Instead, the company provides analog and embedded chips that play a critical role in data centers, industrial equipment and automotive systems. As demand for AI infrastructure and high-performance computing continues to expand, Texas Instruments is well-positioned to capture a growing share of this market. This makes the stock increasingly attractive for long-term investors.

Texas Instruments Six-Month Price Return Performance

Image Source: Zacks Investment Research

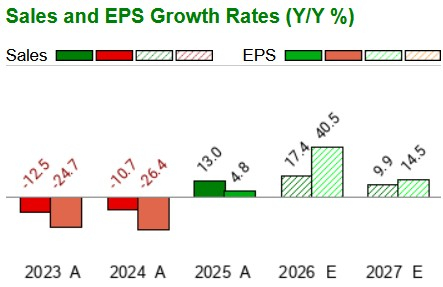

Texas Instruments’ Resilient Financial Performance

Despite macroeconomic uncertainty, geopolitical tensions and trade-related challenges, Texas Instruments continues to deliver impressive financial results. In the first quarter of 2026, revenues increased 18.6% year over year, while non-GAAP earnings per share jumped 31.3%.

Management’s outlook for the second quarter suggests that this momentum is far from over. Texas Instruments expects revenues between $5 billion and $5.4 billion, representing year-over-year growth of 12-21%. The projected earnings range of $1.77-$2.05 per share implies growth of 25-45%, reflecting continued strength across key markets, particularly those benefiting from AI-driven investments.

The Zacks Consensus Estimate for 2026 and 2027 also points to continued expansion in both revenue and earnings, reinforcing confidence in the company’s growth trajectory.

Image Source: Zacks Investment Research

Texas Instruments continues to generate substantial cash, which remains one of its biggest strengths. Over the past 12 months, operating cash flow totaled $7.8 billion, while free cash flow reached $4.35 billion. The company ended the first quarter of 2026 with $5.1 billion in cash and short-term investments, up from $4.88 billion at the end of 2025.

This financial strength gives Texas Instruments significant flexibility. The company can continue investing in research, expanding manufacturing capacity and rewarding shareholders simultaneously. During the first quarter alone, Texas Instruments repurchased $158 million worth of shares and distributed $1.29 billion in dividends. Over the past year, total shareholder returns through dividends and buybacks reached approximately $6 billion. These actions not only reward investors but also support long-term earnings growth.

Data Centers to Aid TXN’s Long-Term Prospects

The data center market is becoming an increasingly important growth engine for Texas Instruments. On the first-quarter earnings call, management highlighted industrial and data center demand as major contributors to growth. This trend is particularly encouraging because global data center investments continue to accelerate due to cloud computing, AI applications and growing enterprise workloads.

Unlike companies that compete directly in AI accelerators, Texas Instruments focuses on the supporting infrastructure required to run these systems efficiently. Its analog and embedded chips help manage power distribution, cooling systems, battery backup solutions, motor controls, signal conversion and connectivity within data centers.

As data centers become larger and consume more power, the need for efficient power management solutions becomes increasingly critical. Texas Instruments is well-positioned to benefit from this trend.

The company's data center business reached an annual revenue run rate of roughly $1.2 billion in 2025, growing more than 50% year over year. In the first quarter of 2026, data center revenues jumped 90% from the prior-year period and increased 25% sequentially. These growth rates highlight the company’s growing importance in AI infrastructure and suggest that this market could remain a major contributor for years.

Internal Manufacturing Strategy Adds Long-Term Value for TXN

Texas Instruments serves a broad range of end markets, including personal electronics, industrial, communications, automotive and data centers. This diversification reduces reliance on any single market and helps stabilize results during economic cycles.

To strengthen its competitive position and capitalize on opportunities tied to AI, 5G and high-performance computing, Texas Instruments continues to invest heavily in internal manufacturing. Rather than depending on third-party foundries, the company plans to produce more than 95% of its wafers internally by 2030.

This strategy provides greater control over production, costs and supply-chain reliability. It can also improve profitability over the long run as manufacturing scale increases.

Texas Instruments is expected to receive up to $1.6 billion in CHIPS Act funding, with total lifetime benefits estimated between $7.5 billion and $9.5 billion. These incentives should help reduce expansion costs and support future margin improvement.

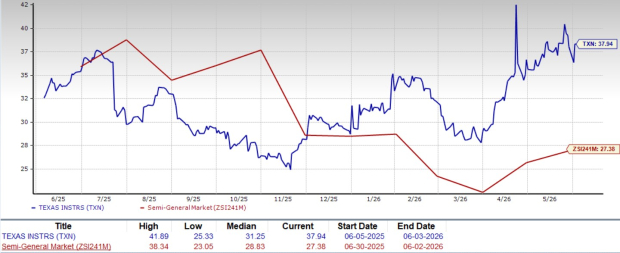

Steady Growth Outlook Justifies TXN’s Premium Valuation

From a valuation standpoint, Texas Instruments is not cheap. The company currently carries a Zacks Value Score of F, indicating that the stock trades at a premium relative to traditional valuation metrics.

TXN currently trades at a forward 12-month P/E ratio of 37.94, well above the industry average of 27.38X. However, premium valuations are often justified when companies combine durable growth, strong profitability and consistent cash generation.

Texas Instruments checks many of these boxes. The company continues to benefit from expanding AI-related demand, generates substantial free cash flow, maintains a strong balance sheet and consistently returns cash to shareholders through dividends and buybacks.

Texas Instruments Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

Compared with other semiconductor leaders, Texas Instruments also trades at a higher earnings multiple than NVIDIA, QUALCOMM and Broadcom. At present, NVIDIA, QUALCOMM and Broadcom are trading at P/E multiples of 22.87, 23.17 and 31.37, respectively. While this premium leaves less room for error, investors appear willing to pay up for the company’s stability, manufacturing advantages and long-term growth potential.

Final Thoughts: Buy Texas Instruments Stock Now

Texas Instruments has built a compelling investment case through its strong financial performance, growing exposure to AI-driven infrastructure spending, expanding data center business and disciplined capital allocation strategy. The company’s focus on internal manufacturing should further strengthen its competitive position and profitability over time.

Although the stock trades at a premium valuation, that premium appears justified, given its consistent earnings growth, robust cash flows and shareholder-friendly approach. With AI infrastructure spending still in the early stages of a multi-year expansion cycle, Texas Instruments looks well-positioned to deliver steady growth for years to come.

Currently, Texas Instruments sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

QUALCOMM Incorporated (QCOM): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).