Office real estate is still a tough sector, but not every office landlord is facing the same story. Older buildings in weaker locations remain under pressure, while newer, well-located and amenity-rich properties are getting a bigger share of tenant demand. Cousins Properties CUZ sits on the stronger side of that divide.

The company focuses on high-quality office assets in Sun Belt markets such as Atlanta, Austin, Charlotte, Nashville, TN, Dallas and Phoenix. These cities continue to attract businesses and workers, helped by job growth, population gains and a lower-cost operating environment compared with many coastal markets.

This makes CUZ an interesting stock for investors who believe the best office properties can keep recovering. Its latest results showed stronger leasing, rising rents and steady portfolio upgrades. The stock has gained 13.2% over the past three months, while the industry has slipped 0.7%.

Image Source: Zacks Investment Research

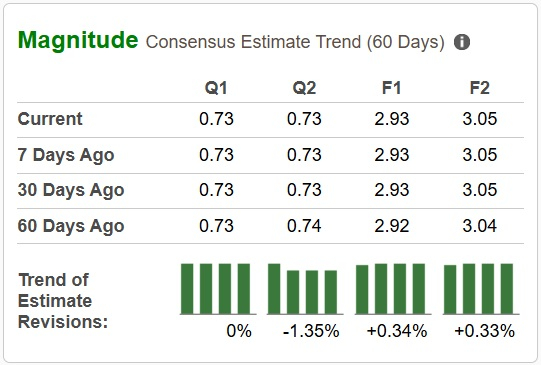

Analysts also seem optimistic about this Zacks Rank #2 (Buy) company, with the Zacks Consensus Estimate for both its 2026 and 2027 FFO per share being revised marginally upward over the past 60 days. The figures also suggest an increase of 3.17% and 4.03%, respectively, year over year.

Image Source: Zacks Investment Research

Here are five reasons to consider buying Cousins Properties stock.

Factors That Make CUZ Stock a Solid Pick

Leasing Momentum Is Strong: One of the foremost reasons to like Cousins is tenant demand. The company signed 932,000 square feet of office leases in the first quarter, one of its best leasing quarters in years. More than half of that activity came from new and expansion leases, which suggests demand is not just about holding on to existing tenants. Management also pointed to a healthy late-stage leasing pipeline, giving investors confidence that occupancy can keep moving higher.

Rents Are Moving in the Right Direction: Cousins is not filling buildings by cutting prices. Second-generation cash rents rose 15.2% in the quarter, extending a long streak of positive rent growth. This is important because it shows pricing power in a market where top-tier space is becoming harder to find. If supply stays tight, the company is expected to have room to keep pushing rents over time.

Sun Belt Strategy Holds Potential: Cousins owns Class A office properties in Sun Belt markets, which continue to benefit from population growth, job creation and corporate migration. Companies looking for talent, lower costs and better business climates are still expanding in these markets, and Cousins is positioned in the type of buildings those tenants want.

Balance Sheet Gives Management Flexibility: Cousins has an investment-grade profile, access to unsecured debt markets and a larger credit facility. The company has solid liquidity, helped by a new $1.2 billion unsecured credit facility and a $500 million bond issue that addresses its 2026 refinancing needs. Leverage was 5.66X in the first quarter, but management expects it to move back toward the low-5X range as planned asset sales are completed. This gives CUZ room to fund acquisitions, buy back shares and improve the portfolio without taking on too much financial risk.

Portfolio Upgrades Can Support Future Growth: The company is actively improving its asset mix. It bought 300 South Tryon in Charlotte, sold Harborview Plaza in Tampa and is under contract to sell One Eleven Congress in Austin. This steady recycling is expected to leave Cousins with a cleaner, higher-quality portfolio. For investors who believe the best office assets will keep separating from the rest, CUZ offers a focused way to play that trend.

Other Stocks to Consider

Some other top-ranked stocks from the broader REIT sector are Prologis, Inc. PLD and W. P. Carey Inc. WPC, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Prologis’ 2026 FFO per share suggests a 6.37% increase year over year.

The consensus mark for W. P. Carey’s 2026 FFO per share has been revised six cents upward to $5.26 over the past month.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Prologis, Inc. (PLD): Free Stock Analysis Report

Cousins Properties Incorporated (CUZ): Free Stock Analysis Report

W.P. Carey Inc. (WPC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).